Moonfare earliest underlying funds date back to 2018, which means that many of them have started to return capital to our community. As of April 2023, at least half of dozen have already generated distributions. These funds span from large-cap buyouts to growth equity and secondaries strategies.

Distributions typically slow down when markets suffer

As the market conditions deteriorated over the past 12 months, however, investors may have been asking themselves what does the new reality mean for the pace of distributions they receive from private market investments.

Indeed, the pace of distributions can depend a lot on the macroeconomic environment. During times of uncertainty, when selling an asset may not result in an optimal valuation, fund managers may opt to delay realisations.

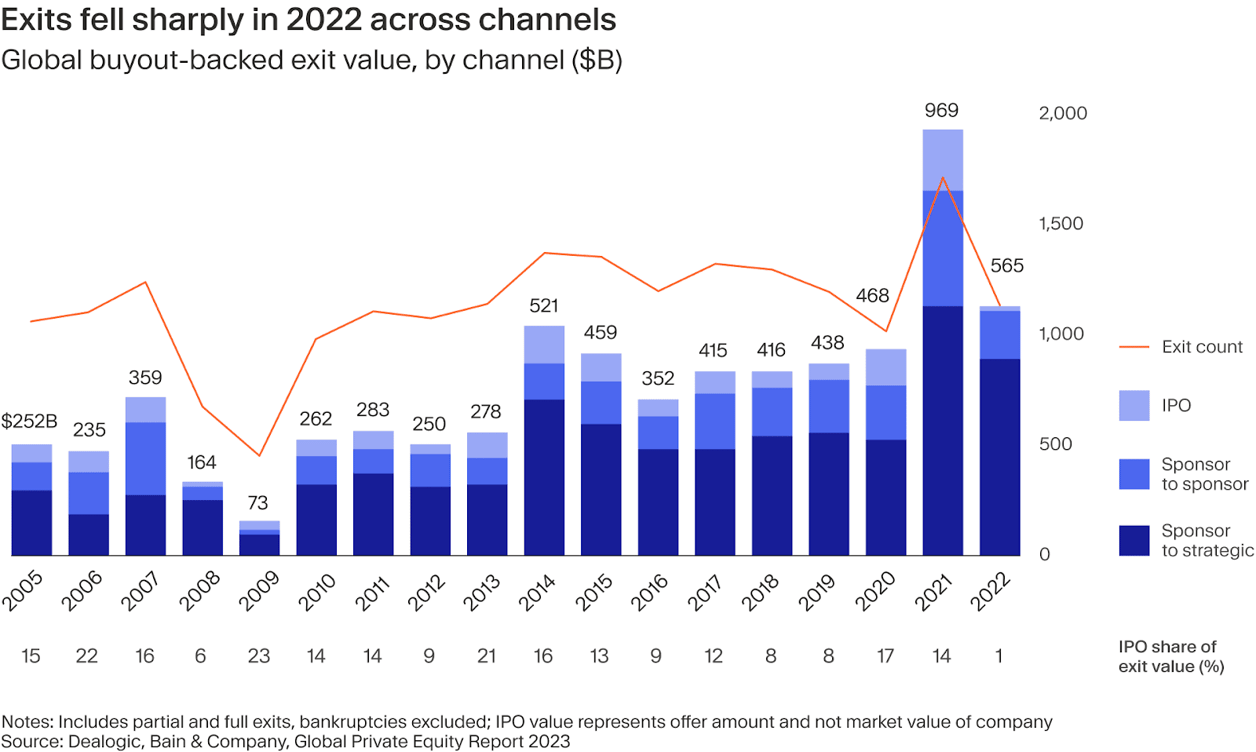

Following the public markets volatility of 2022 and with inflation creating a challenging economic environment, for example, exits slowed sharply across all channels, most markedly in the IPO markets (historically, though, the values remained above average, as demonstrated by the graph below).¹ A potentially more subdued activity in 2023 could continue delaying distributions to investors.

GP-led deals step in

However, the range of realisation routes allows private equity fund managers some latitude. The GP-led deals, for example, are gaining traction and could make distribution profiles less volatile during this cycle. The value of these deals almost tripled from 2019 to 2021 to $68 billion and even stood at $52 billion in a more difficult 2022.²

GP-led transactions see fund managers retain what are usually high quality portfolio companies, most frequently by placing them into a new fund, known as a continuation vehicle. Existing investors are offered the option of rolling over their stake or selling it to gain liquidity. This gives GPs additional time to create value in the company or companies while also offering their investors a choice of distributions or a chance to gain from future upside.

Past recessionary vintages with strongest returns

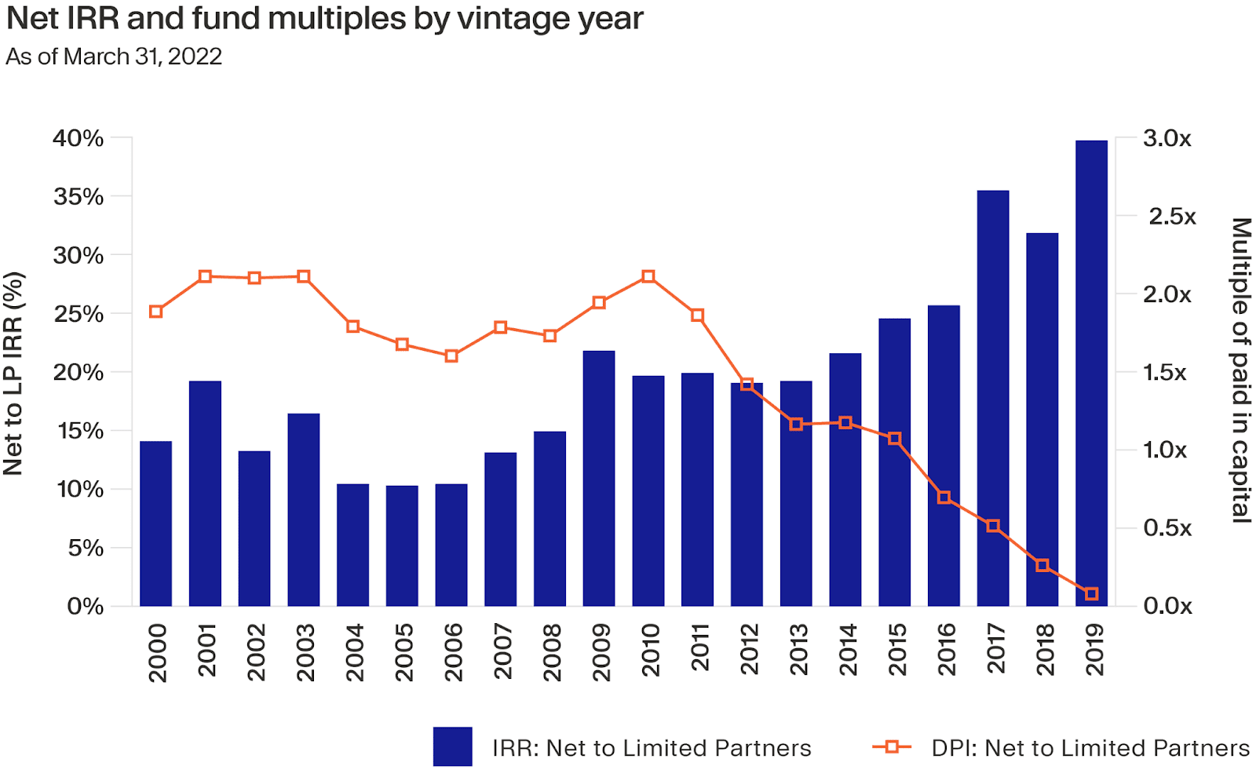

Private equity has a long history of outperforming public markets investments.³ This holds true through economic cycles, as private equity funds focus on creating value in portfolio companies in good times as well as bad; they have the flexibility on exit timing, which means they can sell at attractive valuations.

Indeed, some of private equity’s best returns have been a product of recessionary environments. US buyout and growth funds that started investing in the 2001-2003 and 2009-2011 downturns, for example, generated net distributions paid in capital of 2x - investors received back twice the value of their initial investment - according to Cambridge Associates.⁴

Distribution profiles across strategies

While the exit environment slowed down, it’s still important to note that different strategies have different distribution profiles. More defensive strategies such as some private credit funds will continue making distributions as loans are repaid or reach maturity regardless of where we are in the cycle.

Infrastructure funds can also be more resilient in downturns because of the essential nature of the services provided by their assets and because they may receive inflation-linked income from assets, which they then distribute to investors.

Let’s look more closely at how distribution profiles vary across private market strategies.

Private credit funds tend to return capital more quickly than other private markets strategies. They receive income from loan repayments and often have fixed maturity dates on their loans—as opposed to having to sell investments to realise a return. This means that distributions from private credit funds are typically more predictable and stable. Private credit fund life cycles are also often shorter than the typical 10-year life cycles seen in buyout funds.

Venture capital investments, by contrast, usually take longer to reach maturity since early-stage companies take time to grow and reach a point where they can either be sold or listed via an IPO. Distributions, therefore, tend to take longer to be received—peaking between year 10 and 12.⁵ In addition, the distribution profile tends to be less predictable with other private markets strategies since VC funds have higher loss rates but also higher potential upside. Real asset funds, such as those focusing on infrastructure, tend to have extended life cycles of up to 20 years or more because of the long-term nature of the assets and the contracts involved. Their distributions therefore tend to start coming through from year four onwards. Learn more about the characteristics and benefits of private infrastructure funds.

Distributions in funds of funds and secondaries

Other types of vehicles, such as funds of funds and secondaries funds also have different distribution profiles even though they invest in private equity funds themselves.

In funds of funds, distributions flow from the underlying funds to the fund of funds vehicle and then to its investors. Since the initial investments are made over a longer period of time compared to investments made by a single fund, distributions may take longer. Yet the diversification across funds makes distributions more regular and less volatile than those from direct fund investing.

Conversely, secondaries funds tend to make distributions earlier in their lives because they buy up positions in funds or investments that are already part-way through their investment period. Some distributions can come through within the first year, with the majority of funds returning investors’ initial capital by around year eight.⁶

As we’ve also observed in our 2023 Moonfare Pulse report, secondaries have become increasingly more popular over the past 12 to 18 months. According to our data, 12% of all allocation value in 2022 was targeting secondary opportunities, compared to only 6% a year prior. Given the current climate, the growing interest in secondaries is also not surprising: these investments give investors a recourse to liquidate assets before the end of the fund lifecycle and can function as a lever for more sophisticated cash-flow management.

¹ https://www.bain.com/globalassets/noindex/2023/bain_report_global-private-equity-report-2023.pdf ² https://www.jefferies.com/CMSFiles/Jefferies.com/files/IBBlast/Jefferies-Global_Secondary_Market_Review-January_2023.pdf ³ https://caia.org/blog/2022/07/20/long-term-private-equity-performance-2000-2021 ⁴ www.cambridgeassociates.com/en-eu/insight/us-private-equity-looking-back-looking-forward-ten-years-of-ca-operating-metrics/ ⁵ https://files.pitchbook.com/website/files/pdf/PitchBook_Basics_of_Cash_Flow_Management.pdf ⁶ https://pitchbook.com/news/reports/2020-basics-of-cash-flow-management#downloadReport