Key takeaways:

- Global private equity exit values and volumes reduced sharply in H1 2022 versus 2021 activity trends, led by a significant slowdown in IPOs following market corrections in early 2022. However, 2021 exit totals were abnormally high and activity in the first half of this year was still strong relative to pre-pandemic levels.

- Private equity fund managers have several exit routes they can pursue – including trade sales, secondary buyouts and, increasingly, GP-led secondary deals – to distribute returns to investors.

- Exits in 2022 and through 2023 may continue to be subdued relative to a record-breaking 2021, but are likely to pick up beyond this should conditions improve, valuations start picking up and as delayed exits start coming through.

- Investors should therefore expect a slower pace of returns distributions over the short to medium term, followed by an acceleration once the macroeconomic picture brightens.

Private equity’s long-term investment horizons make the asset class well placed to weather the kinds of choppy conditions we are currently experiencing, driven by rising inflation, stock market volatility and the prospect of recession in many developed economies. Yet it is not entirely immune to market shocks or challenging economic environments over the short term.

Exits are down, but not out

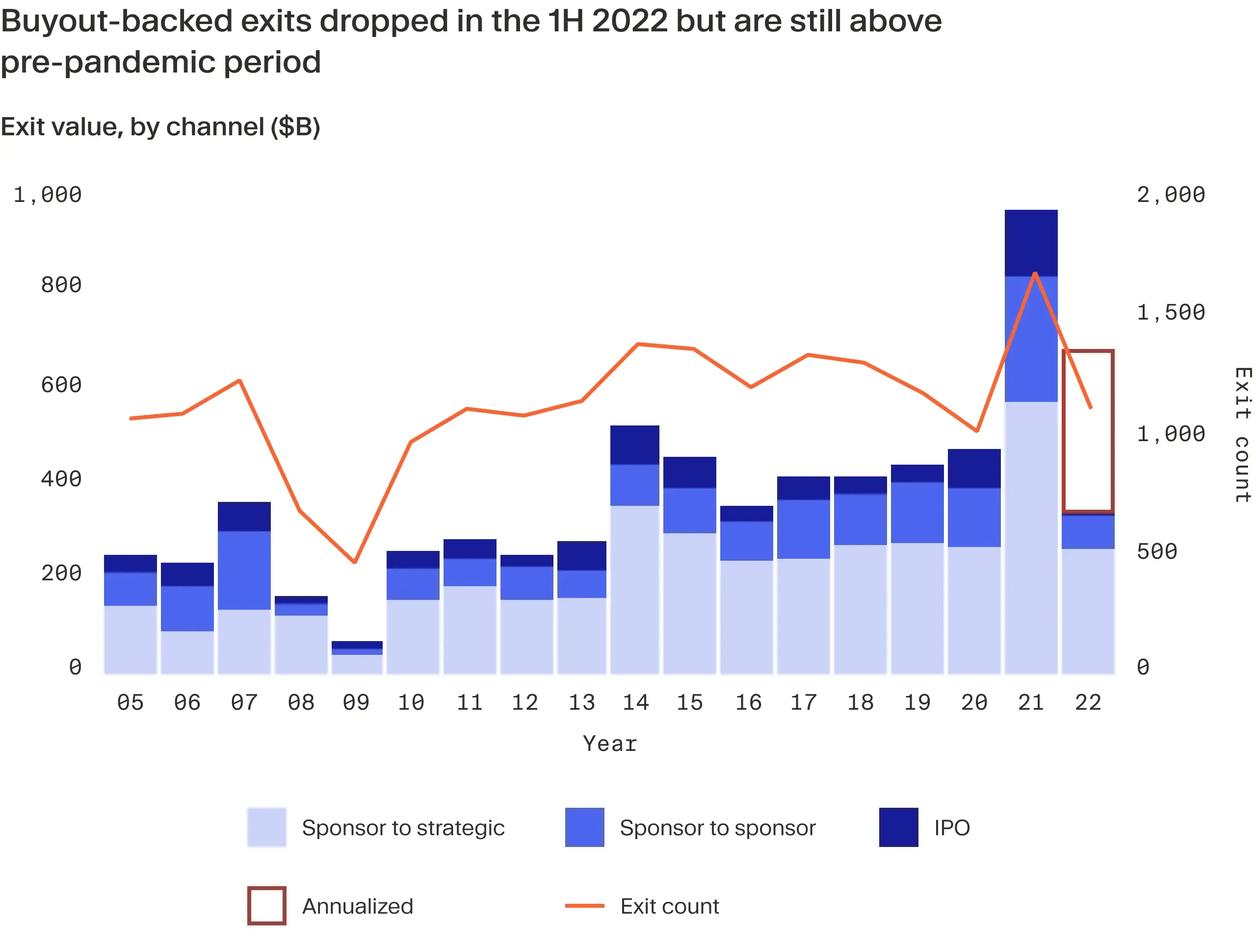

This is clear from the sharp falls in global exit values and volumes for the first half of 2022, relative to 2021 trends. Global buyout-backed exit value fell 37% in H1 2022 versus the same period in 2021, recording a total US$338 billion, according to Dealogic figures.¹ This decline was steepest in the US, where H1 2022 exits totalled just US$190.4 billion, less than a quarter by value of the US$886.8 billion seen in full year 2021, according to Pitchbook data.² Europe, meanwhile, saw a more modest decline by value, of 25.3%, for H1 2022 (€157.8 billion) from the first half of 2021, Pitchbook data shows.³

Yet compared with pre-pandemic totals, H1 2022 looks active. Last year was an outlier – it broke exit total records by some margin, driven by high levels of liquidity, stemming from central banks’ quantitative easing efforts in response to the pandemic and by the pent-up demand for assets following the pause in investment activity when COVID-19 initially struck. In the years running up to the pandemic – 2017 to 2019 – global buyout-backed exit values hovered just above the US$400 billion mark, reaching US$439 billion in 2019, according to Dealogic and Bain & Co.⁴

Behind the 2021 record-breaking figures was a sharp increase in buyout-backed IPOs that started at the tail-end of 2020 and ramped up during the following 12 months. IPOs and exits to special purpose acquisition companies (SPACs – an alternative form of IPO) in 2021 accounted for 23% and 28% of buyout-backed exit values in 2020 and 2021, respectively, per Dealogic and Bain & Co, far higher than the 11-12% seen pre-pandemic.⁵ Yet this year, private equity-backed IPO exits have dropped markedly – by 93%, EY figures suggest - as public markets investors have shied away from new issues and company valuations have fallen following the market correction in early 2022.⁶ Top public technology stocks lost US$3 trillion of market cap during H1 2022, according to S&P Global, for example.⁷

Private equity firms make hay while the sun shines…

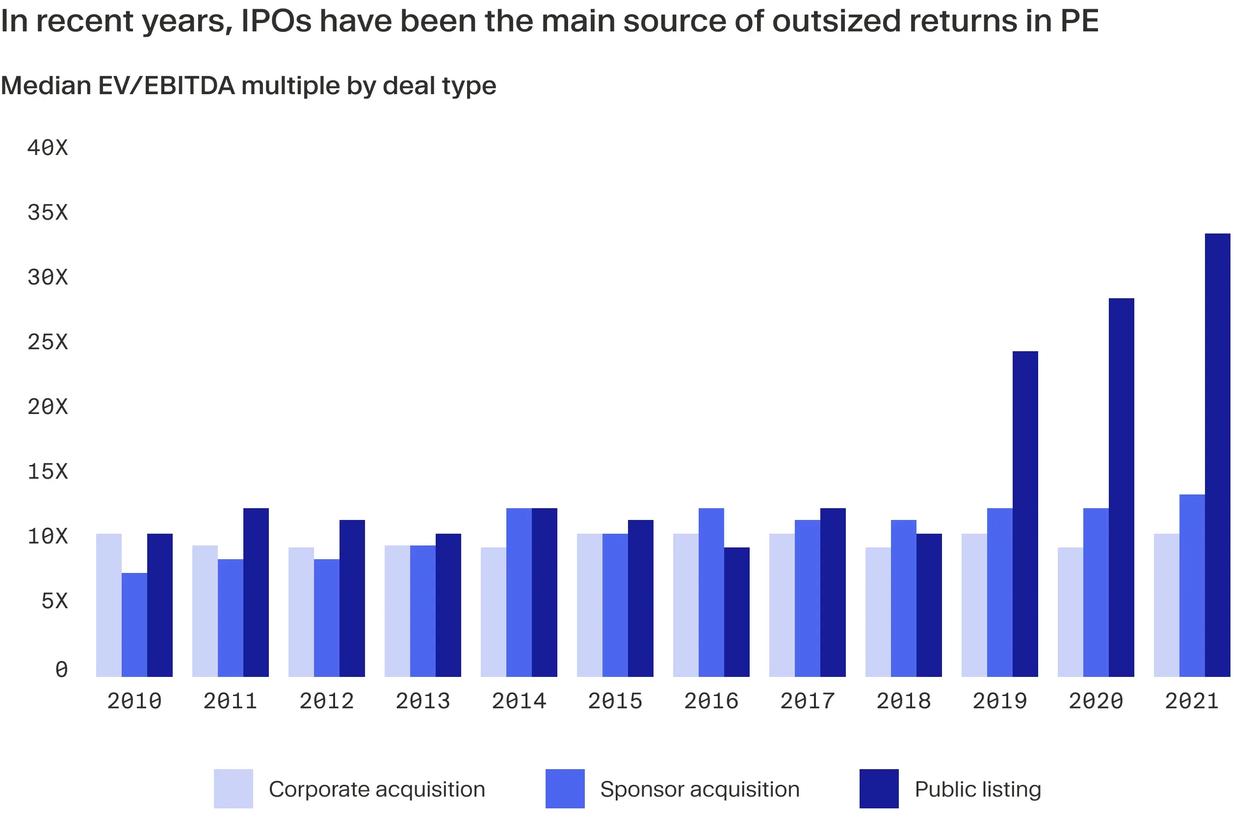

The rush to IPO demonstrates one of private equity’s advantages – that firms have the flexibility to sell at optimum times via optimum routes. During the 2019-2021 period, IPOs offered a significant premium to selling via other routes, as the chart from Pitchbook below illustrates.⁸

Private equity’s other exit routes, by contrast, tend to be less cyclical – and these have so far remained more resilient. The value of sales to strategic, corporate buyers (trade sales) and sales to other private equity buyers (secondary buyouts) has remained broadly in line with pre-pandemic levels.⁹

Examples in H1 2022 include the sale of Dutch fleet management business LeasePlan by a consortium of investors including TDR Capital to trade buyer ALD for a reported €4.9 billion.¹⁰ ¹¹ Among secondary buyouts, CVC Capital Partners sold women’s health company Theramex to PAI Partners and Carlyle for a reported €1.28 billion.¹² ¹³

As Antonia Remmerbach, Investment Manager at Moonfare notes: “The value of trade sales and secondary buyouts remain robust, as private equity managers generally consider several exit routes even if they are aiming to prepare a company for IPO.”

…But exit pace will slow

Yet as we move through 2022, these exit routes may also become more subdued. Firms such as Apollo Global Management, Partners Group and TPG have reportedly signalled as much,¹⁴ while a recent Private Equity Wire survey found that over half of fund managers had delayed, or were considering delaying, an exit because of economic conditions.¹⁵

This proportion is likely to increase further as public market valuations filter through to private markets portfolios (there is always a lag), inflation rises and recessionary forces loom. “The companies nearing the end of their holding period will have been acquired during the 2017-2019 period – when prices were higher and there was macroeconomic stability,” says Remmerbach. “Firms will not be willing to sell on unfavourable terms just because they have reached the end of the average three to five-year holding period.” Further, she adds: “The pressure to sell has been mitigated by the record-breaking exit year in 2021.”

This will inevitably lead to lower and slower distributions of returns to investors than in recent years. For investors, this may well mean more muted returns when measured by IRR (which is time-sensitive) for 2017-2019 vintages. Money multiple returns, however, should hold steady as fund managers can continue to work with portfolio companies to add value and position them for an exit at optimal value.

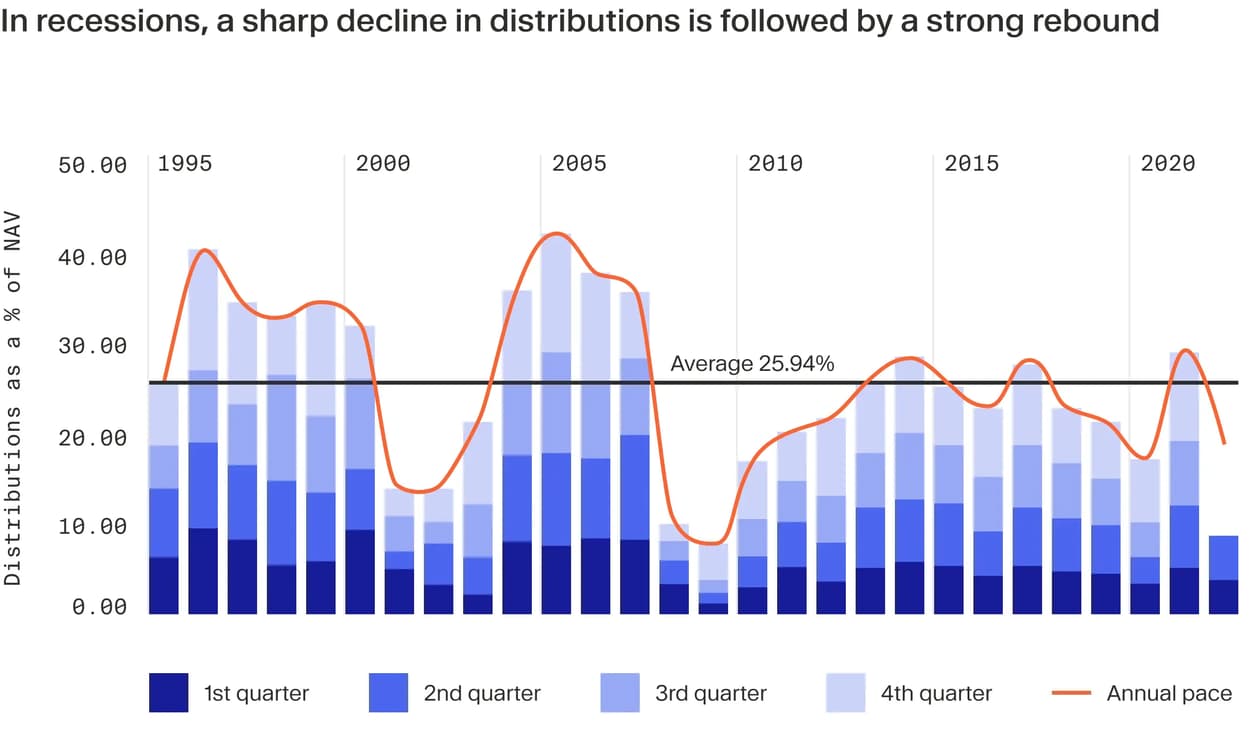

Distribution patterns may not be quite as volatile this time

As the distribution pace chart demonstrates, lower distributions during recessionary periods have historically lasted for between two and three quarters, followed by a sharp rise as conditions improve.

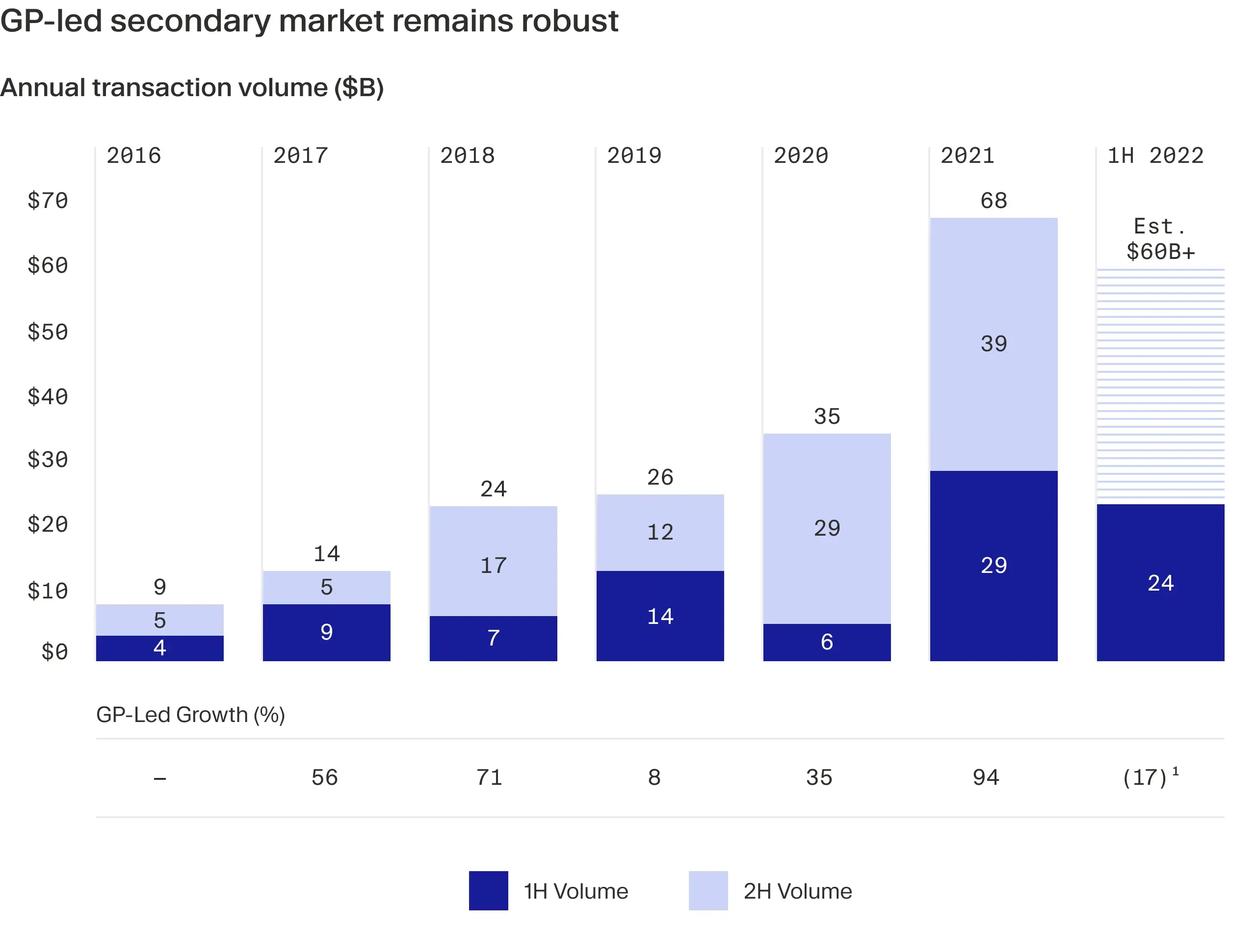

However, there is a mitigating factor this time around: the GP-led secondary market’s rapid development - a phenomenon that has gained traction only in the past few years and that could make distribution profiles slightly less volatile during this cycle.

GP-led deals see fund managers retain what are usually high quality portfolio companies, most frequently by placing them into a new fund, known as a continuation vehicle. Existing investors are offered the option of rolling over their stake or selling it to gain liquidity. This gives General Partners (GPs) additional time to create value in the company or companies while also offering their investors a choice of distributions or a chance to gain from future upside.

“GP-led deals have become an attractive alternative exit route to the traditional secondary buyout, trade sale or IPO,” says Remmerbach. “We expect their growth to continue, especially in the current environment of high inflation, volatility and decreasing valuations, which are leading to longer holding periods.” Indeed, we witnessed this during a recent period of dislocation: the second half of 2020 – as the pandemic struck and exits became more challenging, fund managers deployed GP-led deals in a bid to realise returns (see chart below).¹⁶

Outlook for the rest of 2022 and beyond

Private equity fund managers will exploit the flexibility implicit in the industry’s model – they can time exits to ensure they achieve maximum value for portfolio companies. Most GPs will have realised strong returns over the past year. They will therefore feel less pressured to exit in a less favourable environment and can continue to work with portfolio companies to add value.

The industry is sitting on large amounts of dry powder – US$1.8 trillion as of H1 2022 - and firms will need to deploy this capital within a typical four to five-year investment period.¹⁷ The current trend is to acquire add-ons for portfolio companies. As a recent report from Datasite says: “We expect add-ons to remain a popular theme going forward, especially considering how many current portfolio companies were acquired at ambitious multiples over the past few years.”¹⁸

Yet some of this dry powder will inevitably be deployed in secondary buyouts where firms believe they can add further value and this will underpin part of the exit market in the near term. Trade buyers will also continue to look to private equity portfolios for assets that meet their strategic objectives. IPOs, meanwhile, look set to be more challenging for some time to come. “Overall, we expect trade sales and secondary buyouts to take the lead over IPOs in H2 2022 and into 2023, although exit value will be considerably lower than the record numbers in 2021,” says Remmerbach. “In particular, we expect a flight to quality in global M&A in favour of recession-resilient businesses.”

Sources

¹ https://www.bain.com/insights/shifting-gears-private-equity-report-midyear-2022/ ² https://pitchbook.com/news/reports/q2-2022-us-pe-breakdown (see chart on p21) ³ https://pitchbook.com/news/reports/q2-2022-european-pe-breakdown (see chart on p11) ⁴ https://www.bain.com/insights/private-equity-market-in-2021-global-private-equity-report-2022/ ⁵ https://www.bain.com/insights/private-equity-market-in-2021-global-private-equity-report-2022/ (see Figure 18) ⁶ https://www.ey.com/en_br/private-equity/pulse ⁷ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/top-tech -stocks-have-lost-3-trillion-in-market-cap-in-2022-70807173 ⁸ https://pitchbook.com/news/articles/2021-pe-exits-record-ipo-value ⁹ https://www.bain.com/insights/shifting-gears-private-equity-report-midyear-2022/ (see Figure 4a) ¹⁰ https://www.tdrcapital.com/agreement-leading-to-potential-sale-of-leaseplan-to-ald/ ¹¹ https://www.datasite.com//us/en/resources/insights/reports/deal-drivers-emea-hy-2022.html ¹² https://www.theramex.com/news/a-consortium-of-carlyle-and-pai-partners-to-acquire-theramex-from-cvc-funds/ ¹³ https://www.datasite.com//us/en/resources/insights/reports/deal-drivers-emea-hy-2022.html ¹⁴ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/ipos-vanish-in-h1-but-private-equity-firms-find-other-exit-routes-71571046 ¹⁵ https://www.privateequitywire.co.uk/2022/08/30/317082/exits-being-delayed-ipo-window-narrows ¹⁶ https://www.jefferies.com/CMSFiles/Jefferies.com/Files/IBBlast/1H2022-Jefferies-Global-Secondary -Market-Review.pdf ¹⁷ https://barwon.net.au/wp-content/uploads/2022/07/2022-06-30-BGLPEF-AF-Monthly-Report.pdf ¹⁸ https://www.datasite.com/us/en/resources/insights/reports/as-the-tide-turns-h2-2022-market-outlook.html