Key takeaways:

- Private market liquidity will remain high with private investors who have been sitting on capital during COVID making efforts to put their unspent capital to work.

- Asset price inflation will continue to make it harder for Private Equity investors to identify bargains, however, the impact of inflation on the performance of target companies can create opportunities.

- Broadening the composition of your portfolio will be more important than ever in the current inflationary environment, with secondaries offering consistency and diversification in and out of cycles as part of a balanced investment strategy.

- In choosing which general partners (GPs) to work with, investors should seek those with previous experience of investing and managing across cycles and through crises.

Where does Private Equity find itself at the end of 2021?

The pandemic has affected all areas of finance and Private Equity is no exception. While we can’t be sure that we have seen the full effects of the health crisis yet, what we can be certain about is that the past year has been a better one for private investors than 2020. Nevertheless, it hasn’t all been plain sailing.

As Winson Ng, Moonfare’s Chief Investment Officer, observes: ‘We made the best of it. While certain sectors continued to be badly hit, such as the travel and consumer industries, careful management and diversification across vintages meant disasters were avoided. Fund managers were even able to take advantage of the thriving sectors, such as tech, where fundraising activities and some returns have been the best ever.’

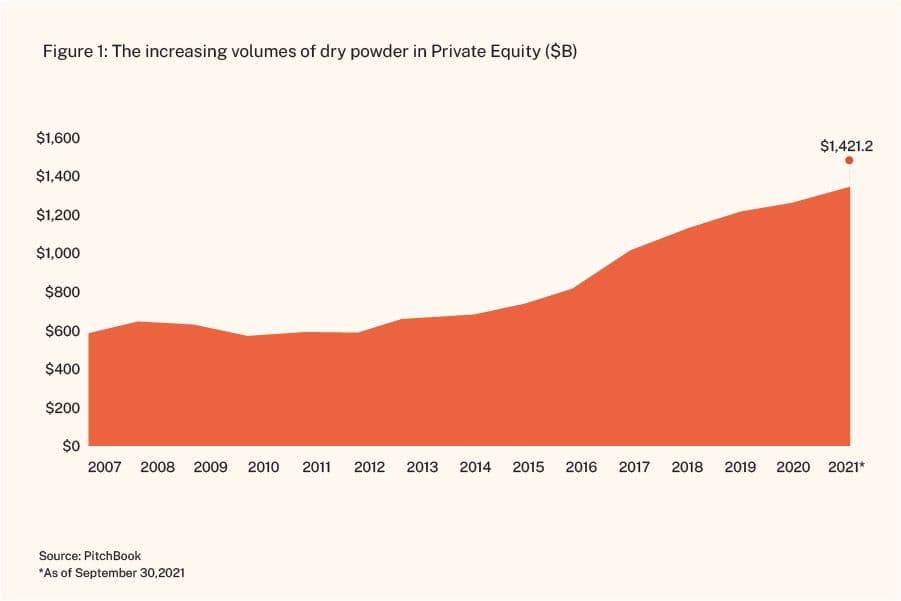

The pandemic was not a financially-driven correction which meant that private investors were able to continue building up record levels of dry powder. Consequently, the second half of 2021 saw a great deal of excess liquidity entering the market. ‘We can expect this excess liquidity to flow through the market for some time meaning we are unlikely to see any further correction in the near term,’ observes Ng.

Increased liquidity has also been exacerbated by the arrival of high-net-worth individuals (HNWIs) into private markets. Whereas Private Equity was once dominated by institutional clients, now private markets are much more established among HNWIs, and a lot of new money is being raised from this segment.

So where does this leave us as we enter 2022? Heightened market liquidity has driven up entry multiples, making it harder to identify bargains and ultimately achieve yield. At the same time, central banks continue to stimulate their economies, albeit less aggressively than at the height of the health crisis. We had become accustomed to low inflation but now face the prospect of ongoing substantial cost increases for some time.

Can inflation be a good thing?

In many respects, inflation is not all bad news for private markets. Given the deal structures that characterise Private Equity strategies, they are generally less impacted by rising costs – and in fact history tells us that private markets often flourish in inflationary environments. You could go as far as to say that Private Equity can offer one of the best hedges against inflation.

At the same time, fund managers have the ability to mitigate negative inflationary effects by actively managing portfolio companies, be this by extracting value, through better management; entering into mergers and acquisitions, or other expansion opportunities; altering portfolio companies’ business models to pass higher costs through to customers; or adjusting the timing of exits. Ultimately the management of inflationary pressures comes down to the conservatism and discipline of the responsible fund manager, and their ability to keep on the right side of conservatism around debt structure and levels, and cash conversion.

In this environment, investors who have been solely focused on achieving the highest risk-adjusted returns might do well to consider adjusting their strategy. Diversification is crucial for a balanced portfolio and investing in growth to the exclusion of all else can be risky. It is advisable to consider assets that are less impacted by the inflation hikes.

The advice from Ng is clear: ‘I suggest that investors don’t solely pursue alpha and growth, but also diversify cash return profiles, for example by adding credit and secondaries into their portfolios. These strategies have the benefit of making earlier returns and so diversify the cash return back to the investor over a number of years.

Infrastructure has also provided a backstop for investors. While Private Equity funds dedicated to infrastructure typically have a longer duration – lasting for as much as a decade and a half – they offer the benefits of greater stability, steady cash flows and limited downside.

The opportunity presented by secondaries

Even before COVID, the popularity of secondaries amongst private investors was increasing, and we can expect further significant growth in this market as we come out of the health crisis. Ng explains: ‘Secondaries have come a long way since the late 1990s and have not only evolved into an established strategy on their own, but also into sub-segments, such as general partner (GP)-led deals or structured deals.’ Secondaries are now widely accepted as portfolio management tools to allocate or rebalance private capital investments.

Whereas the secondaries market was traditionally dominated by buyouts, there are now a variety of available funds with strategies focused on everything from private credit to real estate, from infrastructure to natural resources.

This maturation of the market and rapid diversification of asset bases is enabling a broader range of investors to access these investment opportunities. This is also translating into a number of large platforms and asset managers making a series of acquisitions of secondary funds, further reinforcing their importance in a balanced investment strategy thanks to the consistency and diversification in and out of cycles that they can offer. Read our white paper to learn more about secondaries in Private Equity.

The importance of the right investment partners

While this year will prove challenging when it comes to identifying deals with the potential to offer real value, this shouldn’t prevent you from seizing on opportunities to utilise your unspent capital. When you do so though, it will be vital to choose the right GPs for your investments – ideally those who have been around for some time and gained experience of investing and managing across cycles and through crises.

Ng explains how we do this at Moonfare: ‘Our rigorous due diligence process enables us to identify GP partners who can provide strong returns but are also cycle-tested and navigate high entry valuations. In this way, we only work with GPs who are seasoned investors and know when and where they can add value to portfolio companies.’ Irrespective of what 2022 holds, as an investor your main objective should be to tap into the experience of expert cycle-tested GPs who can drive balanced and sustainable growth in your portfolio – both in down and up-cycles going forward.

If you are interested in the exciting world of private markets, create your Moonfare account in a few minutes.