Key takeaways:

- For PE and VC, 2021 was a record breaking year, driven by a pandemic-accelerated technology boom that led to record buyouts and valuations.

- As it becomes increasingly clear that managers need a high-level of understanding to thrive in tech-investment, they are looking to specialize in the hunt for niche investment opportunities.

- The post-pandemic trend towards specialization may see other complex sectors and sub-sectors like healthtech and cyber security perform well. However, it’s unlikely that 2021 levels of investment will be repeated. While the situation in Ukraine will likely have an impact too.

- New investors should think carefully about relying on specialization too heavily as it’s a strategy more suited to the more experienced. If choosing the specialization route, investors should enlist the services of a reputable manager.

Pandemic saw surge in innovation and PE investment

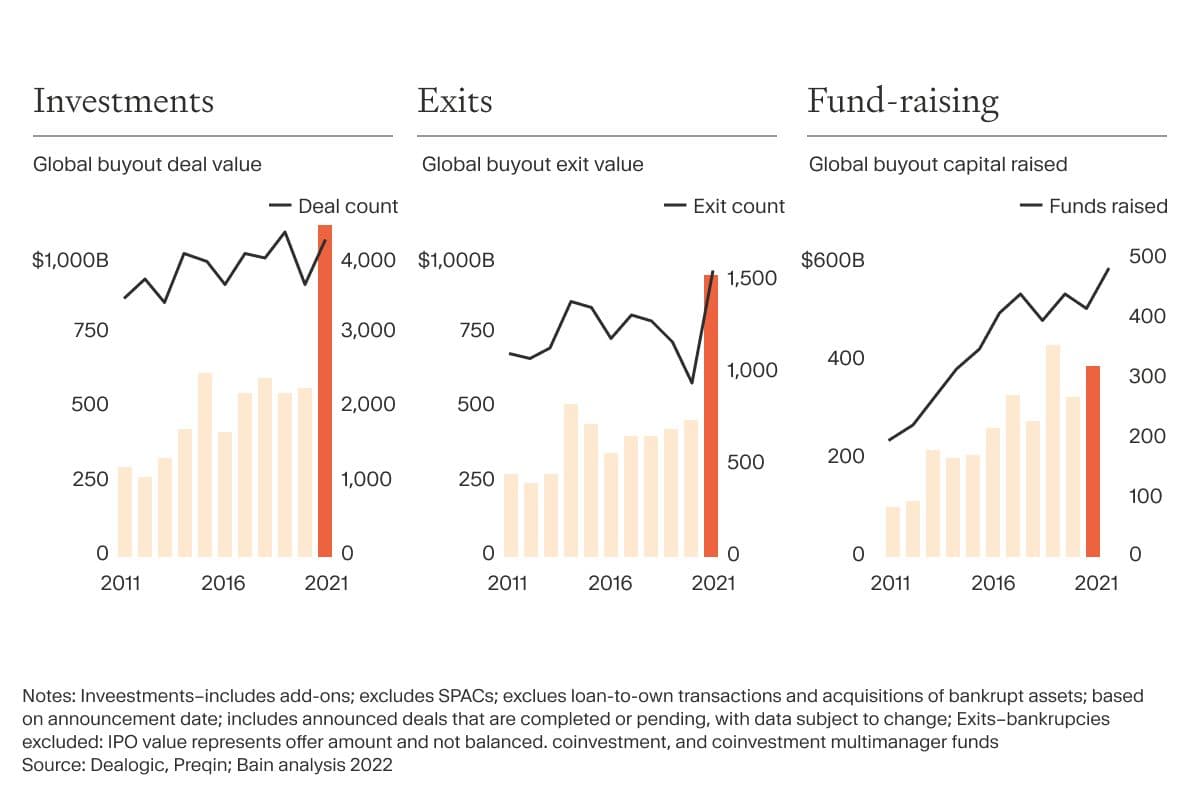

2021 capped a five-year run that saw $1.8 trillion netted in new buyout capital. That makes it the second best year in the industry’s entire history. To put it bluntly, the pandemic was good for Private Equity.

There were a number of macro reasons for this level of growth. Increased liquidity worldwide, boosted by trillions of central bank stimuli pumped into the economy as an antidote to global lockdowns, benefited public and private investors immensely. As we touched upon in our guide to Private Equity in 2022, this liquidity has been bolstered, too, by the arrival of high-net-worth individuals (HNWIs) into private markets, while a quiet start to 2021 left private investors with record levels of dry powder to invest over the second half of the year.

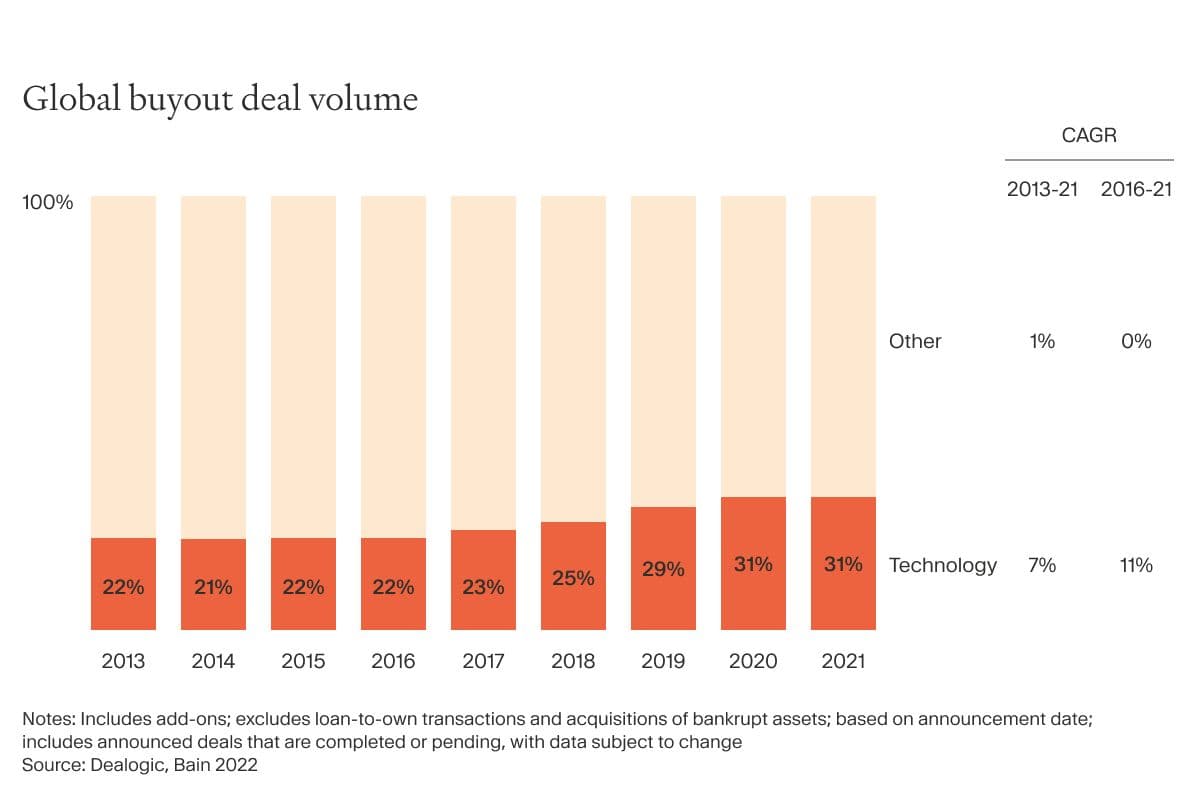

However, the main driver was seemingly the pandemic-accelerated adoption of new technology, and the waves of growth and innovation this triggered. There were $284 billion worth of Private Equity tech deals closed in 2021. That’s 25% of the total buyout value and 31% of the deal count, by far the largest share for any sector.

Driven by this innovation, deal valuations have risen too. The number of deals greater than $1 billion roughly doubled in 2021. All of this has combined to incentivise GPs to specialize and look for niche investment opportunities to generate value and drive returns.

Digital transformation has seen PE specialization surge

It’s becoming increasingly clear to managers that to truly thrive in a deeply competitive space like tech-investment, a genuine high-level of understanding is vital. As tech transforms every industry, investors are now frantically looking for insurgents to fund and established players to bolster. Those who have a deep knowledge, not just of the tech but of the sub-sectors and how they grow, are able to gain the ability to “move quickly and decisively in a hypercompetitive market.”

This isn’t anything new, says Pavel Ermoline, Investment Manager at Moonfare. Over the last decade, there has been a significant rise in specialization as GPs try to stand out from their competitors. But the pandemic has accelerated it greatly, shifting the focus further towards “hands-on value creation”.

Now, Ermoline notes, “Private Equity managers have specialized their skillset and value proposition to portfolio companies and management teams. Some managers specialize in growing regional leaders, others will help companies in their international expansion. Buy-and-build, corporate carve-outs, take-privates are examples of sub-strategies and specializations Private Equity managers can pursue in a very deep market.”

Equally buoyed by tech, VCs are looking to specialize too

We’re seeing something similar play out in Venture Capital (VC), where the digital transformation boom saw VCs perform incredibly well too. According to the Preqin Global Venture Capital Report 2022, “Through three quarters of 2021, venture firms completed $211 billion worth of deals with information technology start-ups; annualized, that figure is double the 2020 figure of $122.3 billion.”

Naturally, industry focus has also begun to specialize. The shift towards value creation is making a generalist approach on accessing attractively priced targets unfit for purpose. On this, Ermoline suggests, “Nowadays, smaller managers usually focus on a select few industries and larger firms, having the luxury of setting up sector-focused teams, can target a broader array of industries within one vehicle.”

Strategy is being specialized here too. Especially as VC backed companies continue to stay private far longer than they previously have. Due to this, the industry has expanded from seed investments to late stage and growth equity strategies. Each of these stages requires its own specialized skill set.

Which other sectors should we monitor post-pandemic?

This post-pandemic trend towards specialization may see especially complex sectors and sub-sectors continue to perform well. And if investors keep up the search for new innovators, tech could easily see another boom. However, it’s unlikely this level of investment will continue - not just in tech but across the entire Private Equity industry. In December 2021, PitchBook suggested: "If the current pace of dealmaking over the last six months continued for a full year, the aggregate deal value would be greater than the current dry powder of all funds."

While rising inflation rates, global supply chain chaos and labor shortages could also have a negative impact.

Despite this, there are still a number of sectors worth keeping an eye on - all of which will require a degree of specialization. For obvious reasons, healthtech is doing incredibly well. According to Preqin’s 2022 report, by Q3 2021, healthcare venture capital deals for the first three quarters reached $79 billion, already surpassing 2020’s record total of $69 billion.

Cyber security is also worth monitoring. The same Preqin report noted that the aggregate deal value in the cybersecurity sector surged from $5.9 billion in 2016 to almost $13bn in the first three quarters of 2021. The horrific situation in Ukraine is likely to benefit this sub-sector too.

However, how the conflict will impact defense investment remains to be seen. As we mentioned in our recent article on the Russian invasion and Private Equity, “In one week, Germany undid decades of its foreign and defense policy. It vowed to initiate massive investments in its defense and security.” It’s yet to be seen how this will fully unfold, but other countries like Sweden are also changing tact on defense investment.

What should new PE investors look to specialize?

Despite a trend in specialization, for newer investors, looking at a range of sectors remains advisable. Ermoline is clear on this: “ Look for specializations that can complement a diverse, global portfolio. An investment focusing on one or a limited set of sectors would usually be advised only for more seasoned investors.”

Of course, only the investor knows how equipped they are. Your level of experience and the scale of your existing portfolio should dictate whether you invest with a manager and a highly focused mandate, or via larger firms with the resources to navigate various sectors at once.

However experienced you are, if you’re set on reaping the rewards specialization can bring, Ermoline advises acquiring “the help of managers who truly understand the sector.”

But that suggestion comes with a clear warning: “Do your research here, there are a lot of managers around, not all of them are up to the task.”