Key takeaways

- Macro-economic headwinds and rising interest have put the brakes on private equity exit activity.

- Trade sales have emerged as the most reliable and active channel, as cash-rich corporates continue to make big ticket transactions, but other exit routes have been becalmed.

- After a challenging year, recovery signs are emerging as interest rates top out, equity and debt markets reopen and buyer and seller pricing expectations converge.

The past 12 months haven't been particularly favorable for private equity exits.

Buyout-backed exit value cratered to $131 billion over the first half of 2023, a 65% year-on-year decline, according to Bain & Company analysis. On an annualized basis exit value and exit volume are expected to fall by 54% and 30% compared to 2022 levels.¹

A combination of rising interest rates around the globe, macro-economic uncertainty and a widening gap between buyer and seller pricing expectations have all contributed to the slide in sales opportunities. Buyers have found it difficult to price risk and value assets when future earnings are unpredictable, while sponsors have been unwilling to offload assets at discounted valuations in the trough of the market.²

Despite these challenges, however, there are growing signs that suggest a potential reversal of the downward trend is on the horizon.

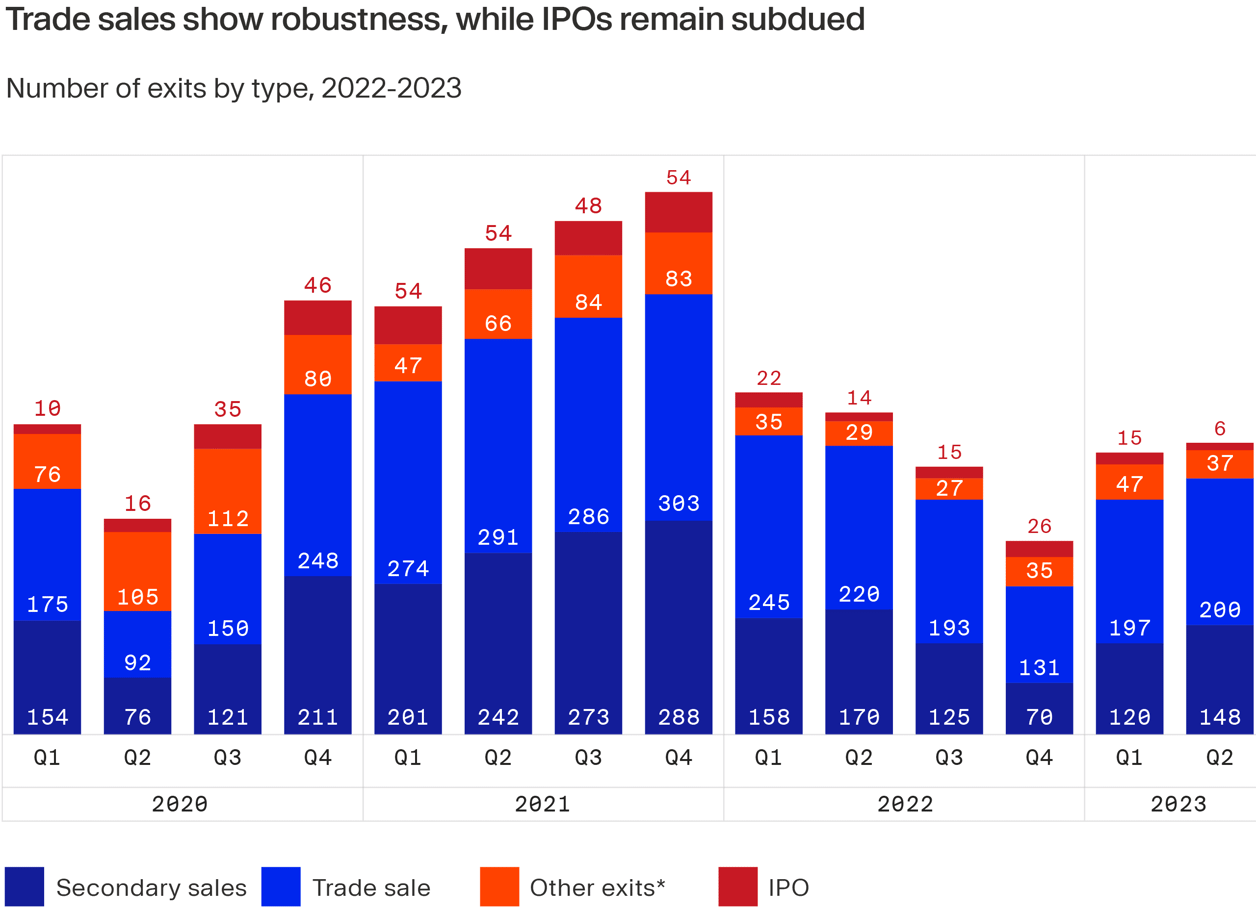

Exit breakdown by channel: trade sales at the fore, IPOs subdued

Activity across all the main exit channels has been impacted by market dislocation, with sales via secondary buyouts to other private equity firms, sales to strategics and exits via IPO all down year-on-year, according to Preqin figures.³

Trade sales accounted for more than half of all exits in H1 2023, with secondary buyouts delivering just over a third of exits and the IPOs less than 3%. The weak showing of IPOs as an exit reflects the impact of volatile markets on investor risk appetites, with equities investors reluctant to back new public offerings in an uncertain environment.⁴

Trade buyers, however, have been able to take a longer-term strategic view on acquisitions and have thus been more shielded from the medium-term market volatility that has weighed on IPOs and secondary buyouts reliant on financing sourced from public debt markets.

Corporates also accumulated large cash balances through the bull markets of 2021. According to a report in Investor’s Business Daily a cluster of just 13 S&P 500 companies are sitting on cash and investments of more than $1 trillion,⁵ making trade sales the most active exit route for private equity vendors.

Fewer exits… but bigger

The dominant role of trade buyers as the most reliable exit channel has led to an increase in the size of exits even though exit volumes have dropped.

Corporates with conviction on the long-term structural shifts that will drive earnings in their respective market have continued to take opportunities to make big ticket acquisitions that fulfill their strategic objectives. CVS Health, for example, acquired primary care group Oak Street Health in a US$10.6 billion deal that provided an exit for private equity backers Newlight Partners and General Atlantic.⁶

Backlog of unrealised assets

But even though corporates remain open to investing in big deals that deliver strategic objectives, this has not been enough to counterbalance the softness in other channels.

The wider exit slowdown has left buyout managers with a record $2.8 trillion of unsold assets in their portfolios, a fourfold increase on the backlog of unexited companies during the global financial crisis.⁷

The tough environment for sponsors has meant that some fund managers have had to sit on assets for longer, restricting the amount of capital investors can plough into the next vintage of funds.⁸ Reigniting exit activity will be therefore crucial for reenergizing the fundraising market.

Better times ahead?

The challenging backdrop for exits remains a concern, but after a difficult period there are recovery signs emerging that point to an improving exit outlook.

The Argos Index, which tracks the EBITDA multiples for European mid-market M&A deals, found that in the second quarter of 2023 valuations improved on first quarter 2023 totals, stabilizing at just under 10x EBITDA after falling away from the peak observed at the end of 2021.⁹

Signs of stabilizing valuations come as visibility on interest rates improves, with confidence building that interest rates are topping out in key markets as inflation cools.¹⁰ This has given buyers and sellers a clearer view on valuations and helped to bring the two sides closer together on pricing.

Settled interest rates should also help to reopen debt markets, with lenders more comfortable when it comes to pricing debt and assessing downside risk. Reopening debt markets could be a significant boost for secondary buyouts deal flow.

IPO window slowly opening up

There are also signs that IPO markets are coming back to life after the private equity firms Sequoia and Softbank managed to float online grocery app Instacart¹¹ and SoftBank listed chipmaker ARM.¹² Stock markets are still choppy, so IPOs remain challenging, but the IPO window has at least opened a crack after being entirely shut earlier in the year.¹³

Corporates, meanwhile, remain firmly in the mix and ready to make big ticket megadeals, as seen recently as tech giant Cisco announced a $28 billion deal to acquire cybersecurity group Splunk.¹⁴

After a turbulent period deal figures also suggest that the exit environment is improving, with PitchBook figures showing a 67% jump in US exit value quarter over quarter, to reach $87.3 billion in second quarter of 2023, while European exit value also picked up slightly in the same period, up 28% quarter-on-quarter. This has put exit value on course to reach between €240 billion and €250 billion for the year, which would be in line with annual exit value prior to the peak of the market in 2021.¹⁵

After a difficult start to 2023 and “soft-landing” for exit activity is now on the table as a possibility. As valuation expectations converge and capital markets come out of hibernation, private equity managers will be hoping that the worst is now behind them.

¹ https://www.bain.com/insights/stuck-in-place-private-equity-midyear-report-2023 ² https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/global-private-equity-exit-activity-slumps-in-q2-2023-76535745 ³ https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/global-private-equity-exit-activity-slumps-in-q2-2023-76535745 ⁴ https://www.weforum.org/agenda/2022/12/ipo-plummet-company-finance/ ⁵ https://www.investors.com/etfs-and-funds/sectors/sp500-companies-stockpile-1-trillion-cash-investors-want-it/ ⁶ https://www.forbes.com/sites/brucejapsen/2023/05/02/cvs-bolsters-primary-care-with-completion-of-106-billion-oak-street-health-deal/?sh=72eae60e20af ⁷ https://www.bain.com/insights/stuck-in-place-private-equity-midyear-report-2023 ⁸ https://www.bain.com/insights/stuck-in-place-private-equity-midyear-report-2023 ⁹ http://www.epsilon-research.com/Market/Argos ¹⁰ https://www.reuters.com/markets/us/investors-keep-bets-us-rates-soon-topping-out-despite-powells-hawkishness-2023-06-22/ ¹¹ https://pitchbook.com/news/articles/instacart-ipo-offering-price-ecommerce-exits ¹² https://www.reuters.com/markets/deals/softbank-backed-arms-long-march-545-bln-us-listing-2023-09-14/ ¹³ https://www.ft.com/content/2b8f723d-52b0-4ea5-9703-7c65e3c6bd35 ¹⁴ https://www.reuters.com/markets/deals/cisco-acquire-splunk-28-billion-2023-09-21/ ¹⁵ https://files.pitchbook.com/website/files/pdf/Q2_2023_European_PE_Breakdown.pdf