Key takeaways

- Sliding debt issuance and rising financing costs are weighing on deal valuations.

- In this environment, private equity firms turn focus to operational improvement to create value as tightening liquidity constrains multiple expansion.

- Secondary funds and direct lenders are providing flexible sources of capital for general partners (GPs) in volatile markets.

After delivering record high levels of deal activity in 2021, the private equity industry has had to reset expectations in 2022, as rising inflation and interest rates push up costs for deal financing.

Private equity is still well-positioned to navigate the impact of tightening debt markets on deal flow, with large sums of dry powder available to managers, as well as access to alternative sources of liquidity from direct lenders and secondary markets.

But even though private equity is well placed, rising financing costs are making dealmaking more challenging. Global private equity investment activity proved relatively resilient over the first half of 2022, with deal value of US$640 billion in line with the US$670 billion generated over the first six months of 2021. As macro-economic headwinds have intensified, managers have tapped the brakes on activity, with deployment down 28 percent quarter-on-quarter and 31 percent down year-on-year. Muted activity is anticipated through the rest of 2022 and into 2023.¹

Key sources of deal debt slow down, while financing costs rise

A major contributing factor to constrained deal financing has been a slowdown in debt issuance in leveraged loan and high yield bond markets. The volume of syndicated institutional loans and high yield bonds across the US and Europe have cratered by 72 percent to US$367 billion over the first nine months of 2022.² These type of loans have been an important source of debt financing for private equity deals during the last decade.

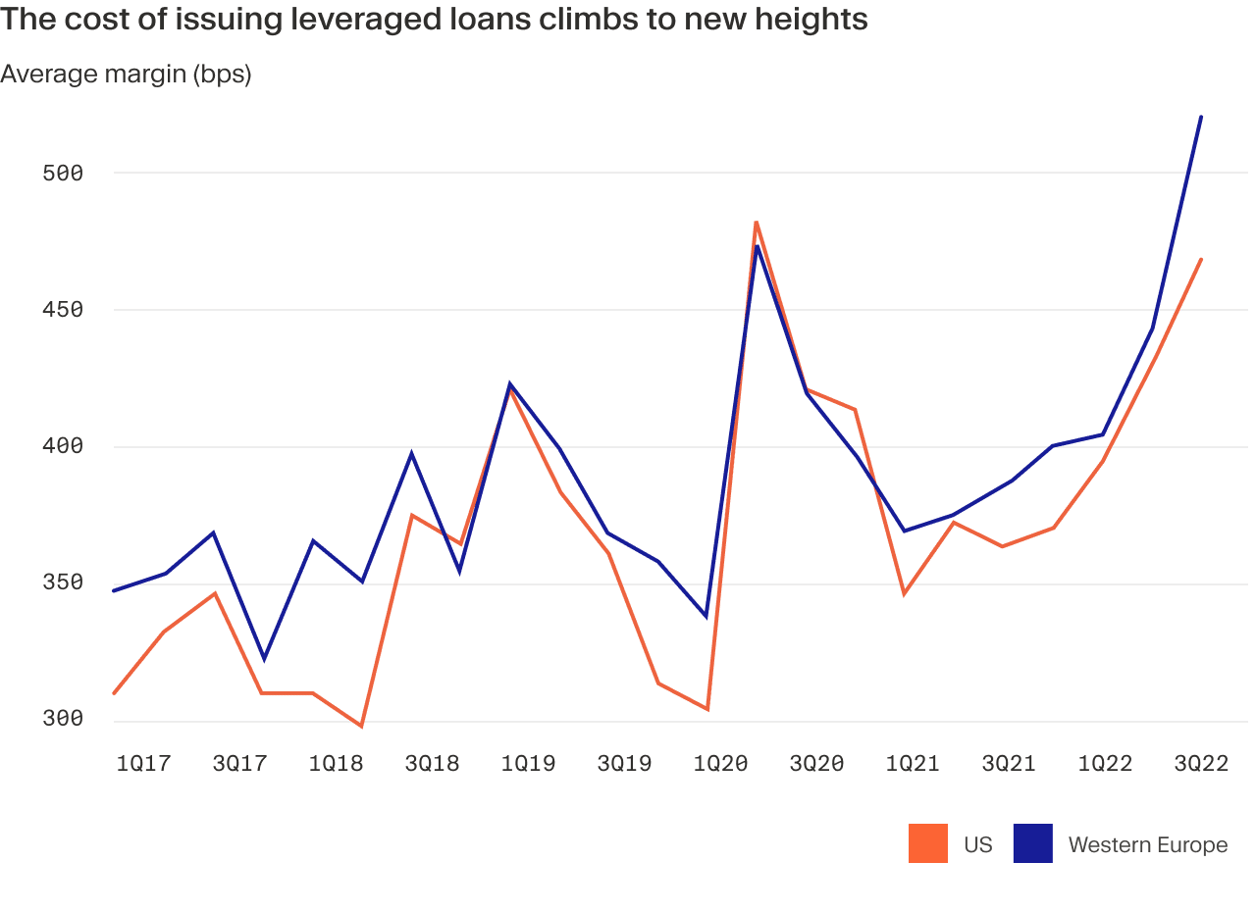

Pricing, meanwhile, has moved in the opposite direction. The average margin on US and Western European institutional loan issuance in Q3 2022 came in at 4.75 percent and 5.29 percent, up from 3.98 percent and 4.08 percent respectively over the first three months of the year. High yield bond yields have experienced similar spikes, with lenders demanding high interest rate coupons in an uncertain, inflationary market.³

This falling supply and simultaneous increased cost of leverage is having a significant impact on private equity valuations and deal structures – capital structures were more conservative in H1 2022 than at any point in the last decade, according to the Centre for Private Equity and MBO Research (CMBOR).⁴

With less debt available for transactions, the prices private equity firms can pay for assets have contracted. Although the shift in debt markets is still to filter down into deal valuations fully, there are already signs of downward pressure on deal multiples. According to the Argos Index, which tracks the M&A pricing for European Mid-Market companies, the average earnings multiples paid for companies have dropped by 14 percent year-on-year to 10x Ebitda in Q2 2022.⁵

In addition to M&A values easing, stock markets have also fallen, obliging private equity managers to reassess and reset the valuations of assets in existing portfolios to reflect the downward shift in stock markets.

This will require managers to adjust exit plans and timelines for some assets, as buyer pricing expectations are recalibrated.

New levers

In a challenging landscape, however, the private equity ownership model does have advantages.

A correction in deal valuations because of more expensive, harder-to-source debt could help to improve the risk-return profile of investments. Deals structured with less leverage may carry lower risk and may also oblige the industry to lean on operational improvement as the primary lever of private equity value creation rather than multiple expansion and financial engineering.

Over the last decade, cheap debt has allowed managers to bank on multiples rising through hold periods. Between 2016 and 2021 firms relied on multiple expansion to deliver more than half of their value creation, according to an analysis from CEPRES Market Intelligence.⁶

Current headwinds will drive a delineation in the market, with GPs that have previously relied on leverage to boost IRRs at risk of seeing returns fall if they’re not able to adapt.

For GPs that can sustainably deliver operational improvement and have a track record of growing portfolio company earnings and margins, however, higher borrowing costs will not necessarily mean lower returns. This will be the case for new deals as well as in portfolios, where firms will be putting long-term strategies in place to help management teams respond to rising prices and interest rates.

Dry powder support

Private markets dry powder, meanwhile, totalled a record US$3.6 trillion at the end of H1 2022⁷ and with valuations tracking lower, managers can deploy their war chests at much more attractive entry multiples. In addition, target companies are having to accept lower prices in negotiations as inflationary pressures and the possibility of a recession slow earnings. There are already cases emerging of buyout firms being able to settle on discounted valuations with deal targets. Thoma Bravo, for example, negotiated a three percent discount on the valuation of software company Anaplan, agreeing on a US$10.4 billion price.⁸

Dry powder can enable managers to shepherd portfolio companies through market turmoil too, either through the provision of additional capital support, or by backing “buy-and-build” acquisition strategies that expand earnings, geographical reach and market positioning.

Direct lenders step up to the plate

In addition to their own dry powder stocks, managers will also be able to continue accessing financing from alternative sources to bank-arranged syndicated loans and bonds. Private debt and direct lenders, for example, have taken advantage of shuttered loan and bond markets to win market share and secure deals that would otherwise have been out of reach.

With more than US$1 trillion of capital at their disposal⁹, private debt managers have remained open for business.

Direct lenders have stepped in to refinance bridge loans for deals, as observed when Ares Management led a club of lenders laying on US$2.15 billion of debt to replace a bridge facility that financed Nielsen’s acquisition by Brookfield and Elliot.¹⁰

Direct lenders are also funding jumbo deals like the US$9.5 billion buyout of software company Zendesk, which was financed by a consortium of direct lenders led by Blackstone.¹¹

Secondaries liquidity

The evolution of the secondaries market has also provided GPs with flexibility and new pathways for driving returns. GP-led secondaries, where portfolio companies are typically transferred into continuation funds and limited partners (LPs) can either cash out or roll their stakes, have made it possible for GPs to extend hold periods rather than facing a weakening M&A exit market, or recapitalize prized assets at the same time as offering investors an opportunity to take liquidity.

GP-led secondaries deal value totalled US$24 billion in H1 2022 and accounted for 42 percent of overall secondaries value, which come in at a record high of US$57 billion as GPs look to alternative sources of liquidity for managing their portfolios, according to Jefferies.¹² Ongoing uncertainty suggests that firms are likely to increase their use of secondaries markets for recaps, of companies as well as partial sales. This bodes well for secondaries activity in the months ahead.

Adapting to change

This year has been one of adjustment for the private equity industry after an outlier year in 2021 when abundant liquidity supported unprecedented levels of buyout activity.

As the deal activity reverts back to pre-pandemic levels, managers are responding to the impact of rising interest rate costs on deal financing structures and asset valuations by focusing on value creation and tapping into alternative sources of liquidity.

Dealmaking has become more challenging, but flexible private equity managers continue finding ways to keep investing.

¹ S&P Global Market Intelligence ² https://community.ionanalytics.com/levfin-highlights-3q22 ³ https://community.ionanalytics.com/levfin-highlights-3q22 ⁴ https://www.privateequitywire.co.uk/2022/08/31/317102/dealmaking-drops-h1-shows-resilience ⁵ https://argos.wityu.fund/argos-index-2nd-quarter-2022/ ⁶ https://www.bain.com/insights/inflation-global-private-equity-report-2022/ ⁷ https://www.bain.com/insights/shifting-gears-private-equity-report-midyear-2022/ ⁸ https://www.ft.com/content/117ebfdd-5d94-4cd0-9dc3-01de3c5c14c1 ⁹ https://www.ft.com/content/824a7fc3-a8a3-4a78-a565-bd663ba71520 ¹⁰ https://www.bloomberg.com/news/articles/2022-05-03/ares-led-group-snaps-up-2-billion-chunk-of-nielsen-buyout-debt ¹¹ https://www.bloomberg.com/news/articles/2022-06-24/blackstone-led-group-provides-5-billion-of-debt-for-zendesk ¹² https://www.jefferies.com/CMSFiles/Jefferies.com/Files/IBBlast/1H2022-Jefferies-Global-Secondary-Market-Review.pdf