Key takeaways

- The stability of traditional 60/40 portfolios has come under question recently, as high inflation and economic uncertainty reduce their diversification benefits.

- In turn, institutional investors have increasingly been turning toward alternative assets, adding larger allocations to the likes of private equity as a source of higher risk-adjusted returns and diversification.

- Given the economic shift, more investors may wish to consider adding alternative assets in order to rebalance their portfolios.

For more than half a century, many investors have constructed their portfolios according to the 60/40 principle. This entails reserving 60 percent of your portfolio for public equities, and the remaining 40 percent for bonds. The overall aim of this set up is to achieve more consistent long-term returns while lowering levels of volatility.

Until recently, this largely worked. Measured against pure stock and bond portfolios from 1988 to 2018, the 60/40 strategy provided a buffer against volatility and a better long-term return.

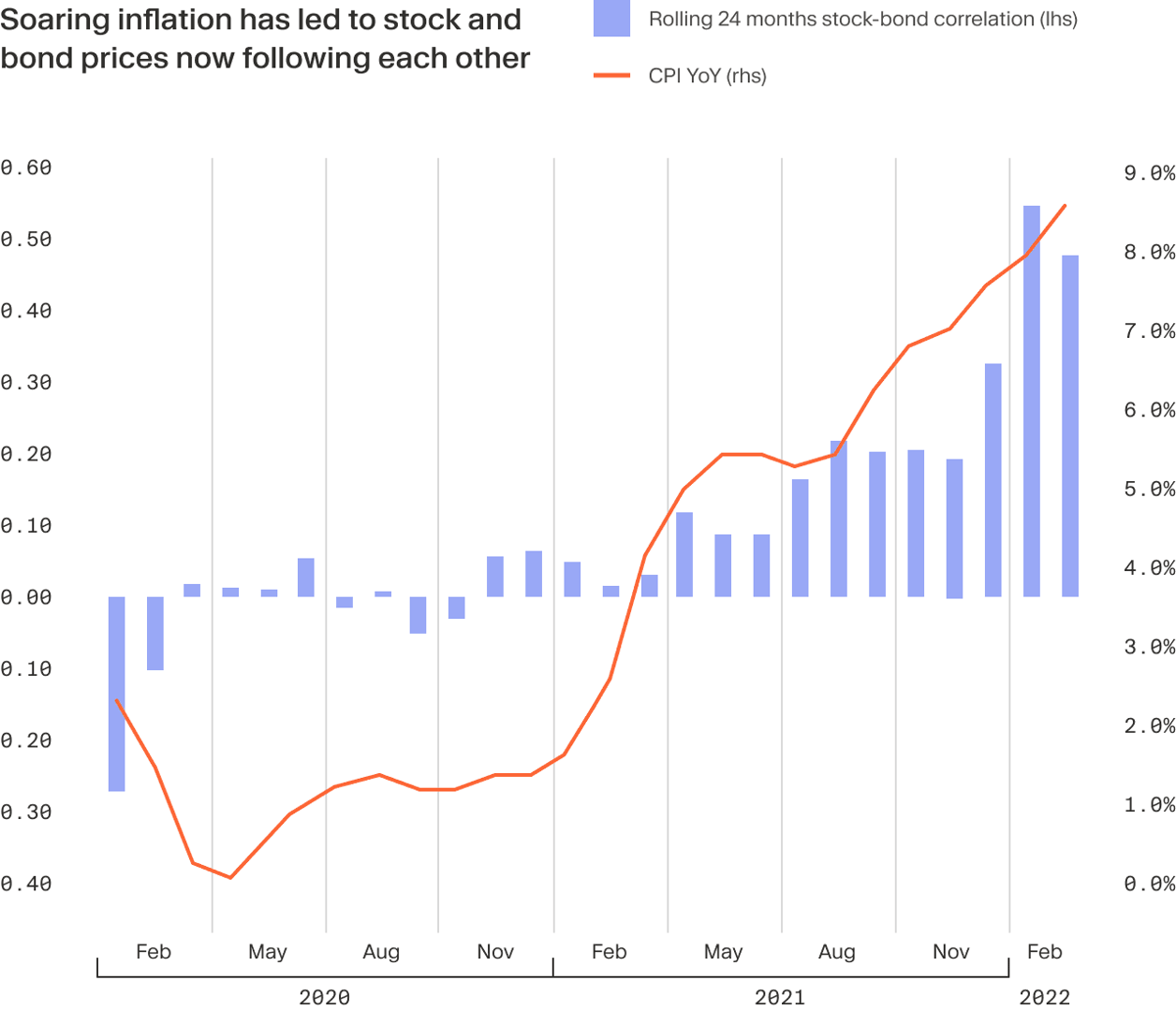

However, its recent success came in part from the fact that, for the last 20 years or so, bond and equity prices were negatively correlated – that is, when one asset class would decrease in value, the other would increase. This would help keep the portfolio diversified, given its ability to perform well in different market environments.

Increasingly, however, this is no longer the case.

‘High inflation, increasing interest rates and high uncertainty are destabilising the relationship between bonds and equities,’ says Pavel Ermoline, Investment Manager at Moonfare. ‘This is weakening the impact of the 60-40 model.'

Given this shift, many institutional investors have been moving away from such models for decades, adding allocations to alternative asset classes such as private equity alongside existing stocks and bonds. This has helped reinstall diversification benefits, as well as add another source of returns.

The wider investor community, however, is lagging behind. This, explains Ermoline, means many could be missing out. ‘Investors should think about diversifying their exposure away from only traditional asset classes,’ he says. ‘And in the context of relatively low interest rates, private markets have a key role to play.’

A brief history of 60/40 portfolios

The 60/40 model first emerged in the 1950s as a by-product of modern portfolio theory. However, it did not come to the fore until the 1970s, when investment giant John Bogle made it a cornerstone of index investment at his newly founded Vanguard Group.

The logic behind this mix is that the equity allocation would outperform in better times, while the bonds would provide a level of downside protection and resilience in the worse conditions. In essence, the latter’s relatively lower volatility would act to counterbalance uncertain equity markets, providing investors with the chance of better risk-adjusted returns. Indeed, according to Schroders, an investment of $1,000 in 1989 and measured through 2019 would have an annual return of 7.5 percent, outperforming pure stock or bond portfolios over that timeframe.

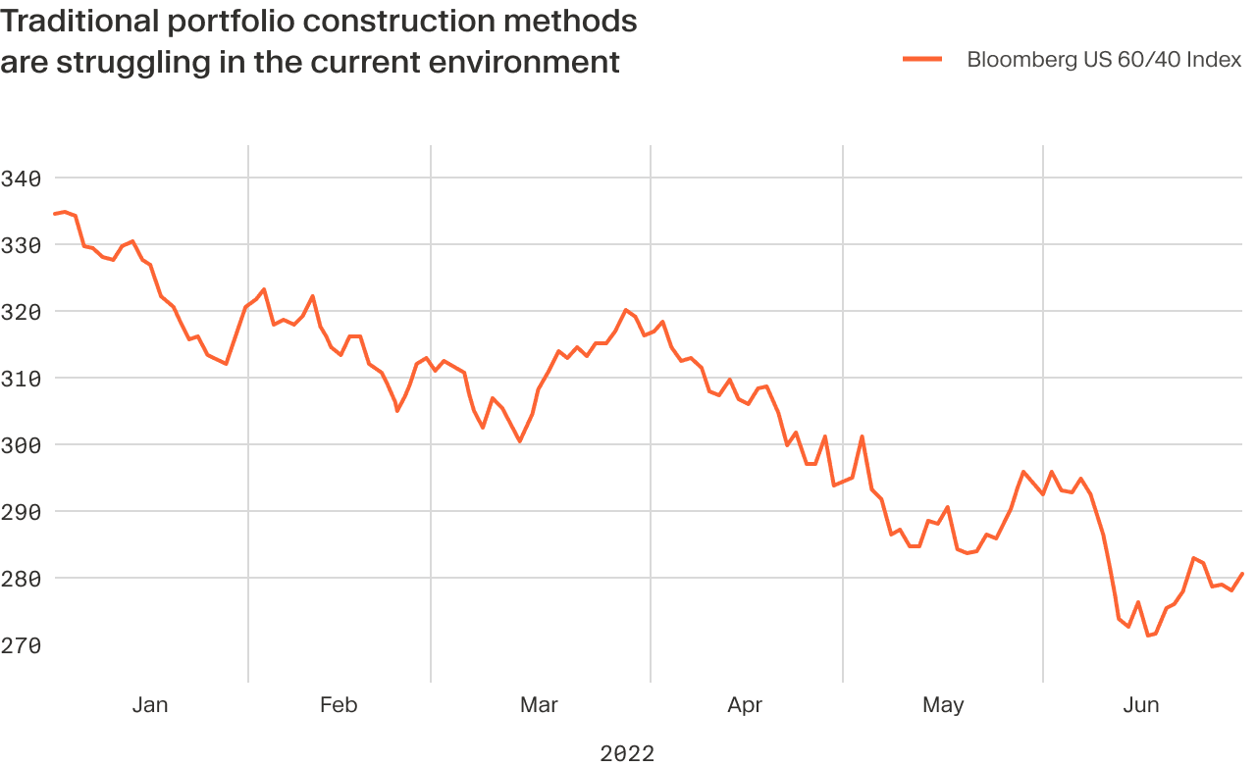

The model served investors well for years, and no more so than during the last decade. Between 2011 and 2021, the 60/40 portfolio generated an 11.1 percent annual return. This year, however, has been a different story. In the first six months of 2022, the Bloomberg US 60/40 Index – a tracker of that type of portfolio’s performance – was down around 17 percent.

New economic reality is transforming portfolio construction

There are a few reasons for this. At a fundamental level, stocks and bonds were already at historically high valuations. In 2021, for example, the S&P 500 notched 70 all-time highs through the year and gained 26.9 percent overall. With bonds, meanwhile, relatively low yields also offer a poor starting point for future returns, with even negative yields on offer in some core sovereign markets. Yet this ignores the clear change in relationship between the asset classes that is undermining their diversification.

In recent history, bonds have been a relatively reliable buffer when economic growth is slowing, as investors usually flock to safe-haven assets, such as sovereign debt, in uncertain times. However, increasing inflation can negate this, as rising prices reduce the real return on bonds, given they are mainly assets with a fixed rate. For stocks, meanwhile, rising rates and prices put pressure on companies' bottom lines, dragging down equity markets as well.

'In a high inflation environment with central banks raising interest rates as a first response, equity markets tend to move in the same direction as bonds, weakened by higher input costs and increased discount premiums,' explains Ermoline.

In the first half of the year, the S&P 500 index dropped more than 20 percent, its worst first half performance in more than half a century. Bonds also came under pressure from rocketing inflation and rising interest rates. For example, in the same period, US Treasuries had delivered total year-to-date losses of 11 percent.

If these high levels of uncertainty are maintained, equity and bond markets could continue to mirror rather than counterbalance each other.

‘This blunts the effectiveness of 60/40 as a diversifier,’ says Ermonline.

Remodelling portfolios with private equity

In light of this, institutional investors have already been diversifying away from stocks and bonds and towards alternative asset classes, such as private equity. Today, market allocations for big institutions – including pension funds, endowments and foundations – generally range from 10 percent to 25 percent.

'Institutions have been known to proactively shift their asset allocation through time, including a larger and significant allocation to private equity,' explains Ermoline. 'They have recognised that exposure to this asset class has become a vital driver of returns.'

For less sophisticated investors, following this lead is inherently more tricky. 'The penetration to the broader investor market has taken more time,' Ermoline says. 'Challenges such as illiquidity, access and an education gap mean some are not yet in position to extract the full potential of a PE allocation.'

However, while there are challenges, it’s important to weigh up the benefits of allocating to private equity and other alternative assets during portfolio construction.

Potential for higher risk-adjusted returns

Although past performance is not necessarily indicative of future returns, private equity’s track record of a long-term return profile could prove highly beneficial in an environment of lower returns from bonds and stocks. Between 2001 and 2021, private equity and private credit outperformed global public equity and credit markets in 19 of the 20 years.

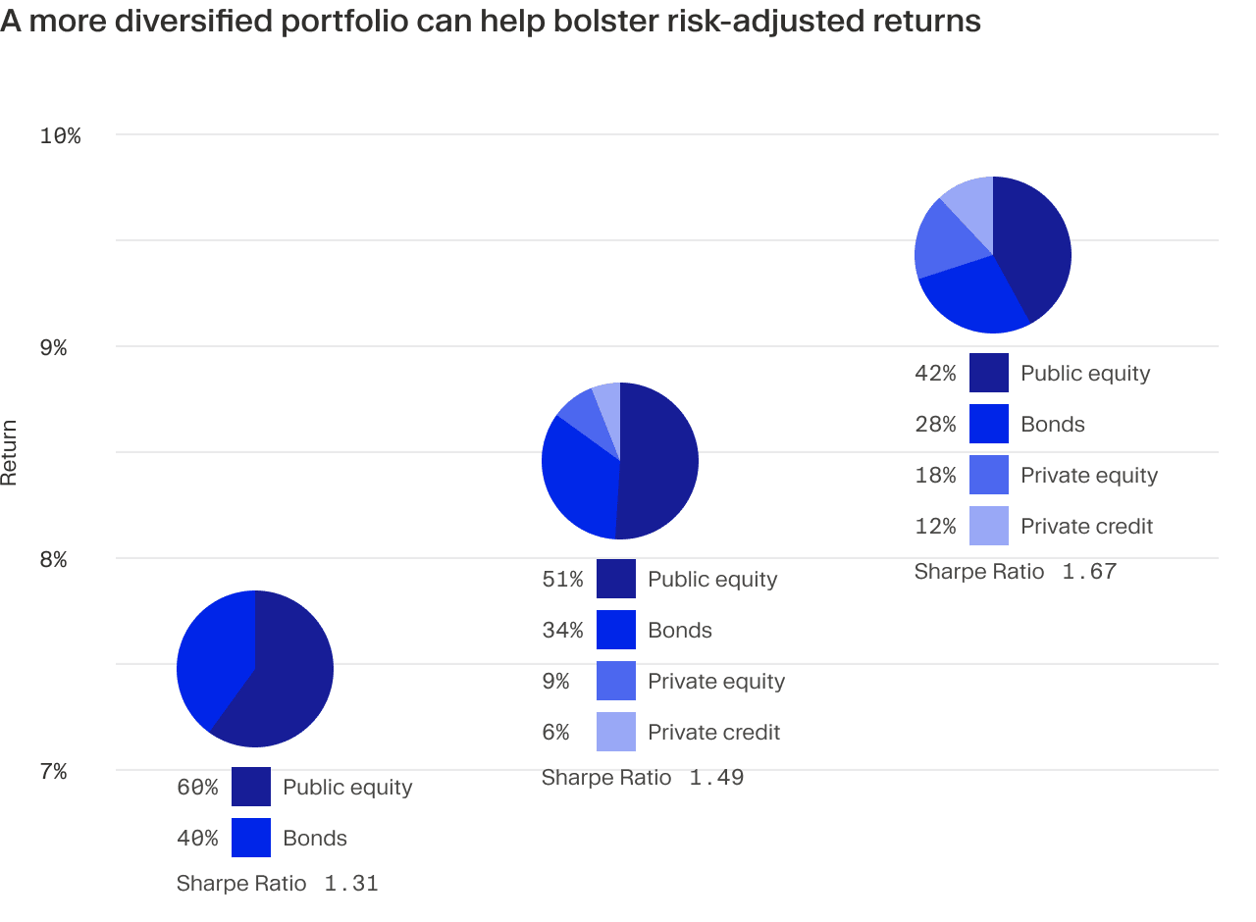

Adding this to a traditional portfolio can help bolster performance. Research by Hamilton Lane shows that between 2000 and 2020, a rigid 60/40 portfolio offered annual returns of around 7.5 percent. However, a portfolio with a larger allocation to private equity and real estate (42 percent public equity, 28 percent bonds, 18 percent private equity, 12 percent private credit) offered annual returns of 9.40 percent.

Greater diversification

On top of the return potential, adding private markets can also help investors broaden their base, and diversify away from an ever-shrinking set of companies listed on stock exchanges. In the UK, for example, the number of companies listed on the country’s stock exchanges has fallen by 12.5% in three years.

Adding a private market allocation to a portfolio means owning a wider and more diverse section of the investment landscape. It also provides access to companies and industries that are rarely on or too early for public markets, such as Silicon Valley startups. This, in turn, diversfies and spreads risk at a lower level through the portfolio, rather than concentrating it in one area. Indeed, according to Hamilton Lane research, the overall risk profile of a portfolio fell as select amounts of private credit and equity were added.

How should private market assets be added to a portfolio?

Like all investment decisions, allocating private equity into a portfolio comes with a degree of risk and needs careful consideration and due diligence. At a macro level, this can be boiled down to three key points investors should consider:

Take a top-down perspective. Before you allocate, it is important to understand how private equity or other alternative assets would work alongside your existing investments. Being able to assess how a PE allocation would affect overall portfolio volatility and performance is the first step to take.

This entails taking a bird’s-eye view of the portfolio and determining how much you want to allocate across different assets. ‘Private equity, like private real estate and credit, all have publicly listed counterparts in the form of stock, REITs, and bonds,’ says Ermoline. ‘The first step should be to start from a top-down analysis and determine how much to allocate between equities, real estate and credit.’

Broaden your horizons. Keeping focus on one alternative asset class could hamper your potential for greater risk-adjusted returns, while also inherently reducing the diversification benefits of spreading different instruments across the portfolio. ‘Private equity, real estate and credit should all be considered in the underlying asset allocation, based on factors including investment horizon and target return,’ Ermoline explains. ‘Each of these sub-asset classes has its own merits and will help investors to achieve higher returns while adding to diversification.’

Learn from the best. Each investor will have their own preference for how much of their portfolio they will want to allocate to private markets. However, there is nothing wrong with taking inspiration from more experienced practitioners. ‘The optimal allocation depends on a lot of different factors, and will ultimately vary from one individual to another,’ says Ermoline. ‘But looking at what experienced investors are allocating, and using this as a benchmark, is a good starting point.’

For decades, 60/40 has been a cornerstone of investment strategies across retail and institutions. However, as circumstances change, questions need to be asked about whether existing models of investing can stand the test of time.

At present, the worsening economic landscape is seeing many investors adjust their asset allocation to include more private equity, not just as a source of returns, but to take advantage of active management strategies. As pressure on returns increases, it could be a decision that yields real benefits.

“The private equity model makes a lot of sense in a downturn, where operational support is key to weather the storm,” says Ermoline. “Many investors have already shifted their asset allocation towards including more private equity, and have demonstrated how this decision can lead to robust performance generation through multiple cycles.”