Liquidity is often top of mind for investors in times of economic turbulence. The uncertainty that this environment brings, stoked by falling activity and asset price volatility, drives demand for access to cash at hand.

This is particularly acute for individuals, who are likely to be more susceptible to an unexpected change in circumstances than large institutional investors.

As a consequence, barriers to private markets can appear taller in these times, given the closed-end nature of many funds in the asset class. For example, illiquidity was the most-common issue cited by our investor community in our 2022 Investor Survey. Around three-quarters of family offices, meanwhile, highlighted liquidity issues as a significant barrier to private market investing.

Why private markets can tune your portfolio for long-term success

Favouring more liquid investments — including public stocks, bonds and hard cash — is certainly understandable in uncertain times, given the value investors place on being able to realise positions quickly.

Yet while having a portfolio concentrated with highly liquid assets may be appealing, shunning private market investments during downturns could have unintended consequences on your long-term return potential. So, what benefits can private market allocations bring to your portfolio?

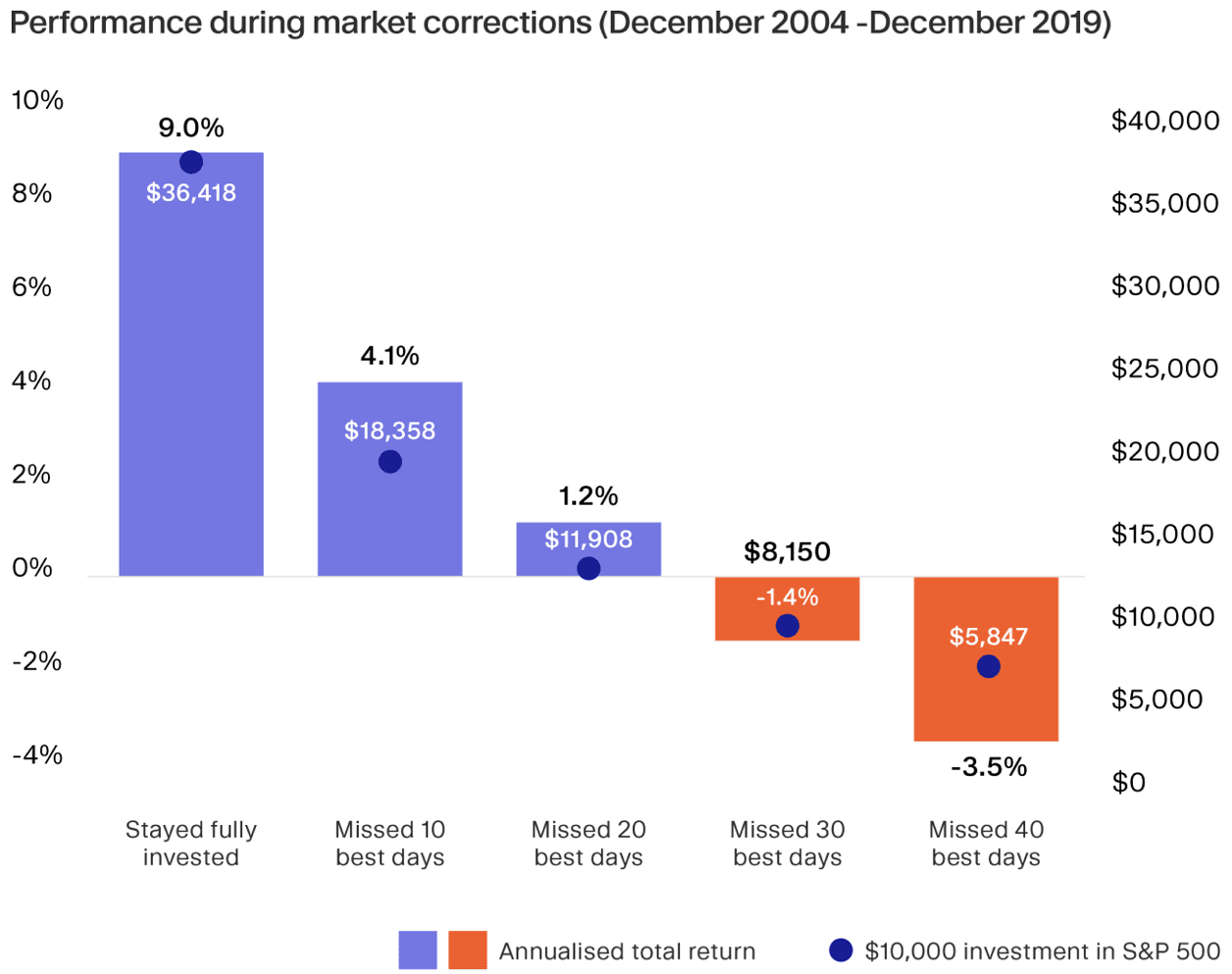

Long-term focus. Following the crowd as the market moves may make sense in the short term. However, for investors focused on the longer term, realising liquidity early could do more harm than good.

Equity market research from Putnam Investments highlighted by Ninepoint Partners, for example, suggests that investors who stayed fully invested during volatile periods gained the most in terms of risk-adjusted returns. Having some measure of private market assets, given their long-term nature, can help shield portfolios to a degree during these corrections.

Adding upside. Strategies like private equity tend to offer a higher return than other, more liquid assets — including public stocks and fixed income — precisely because they require investors to tie up their capital for longer than they may otherwise prefer.

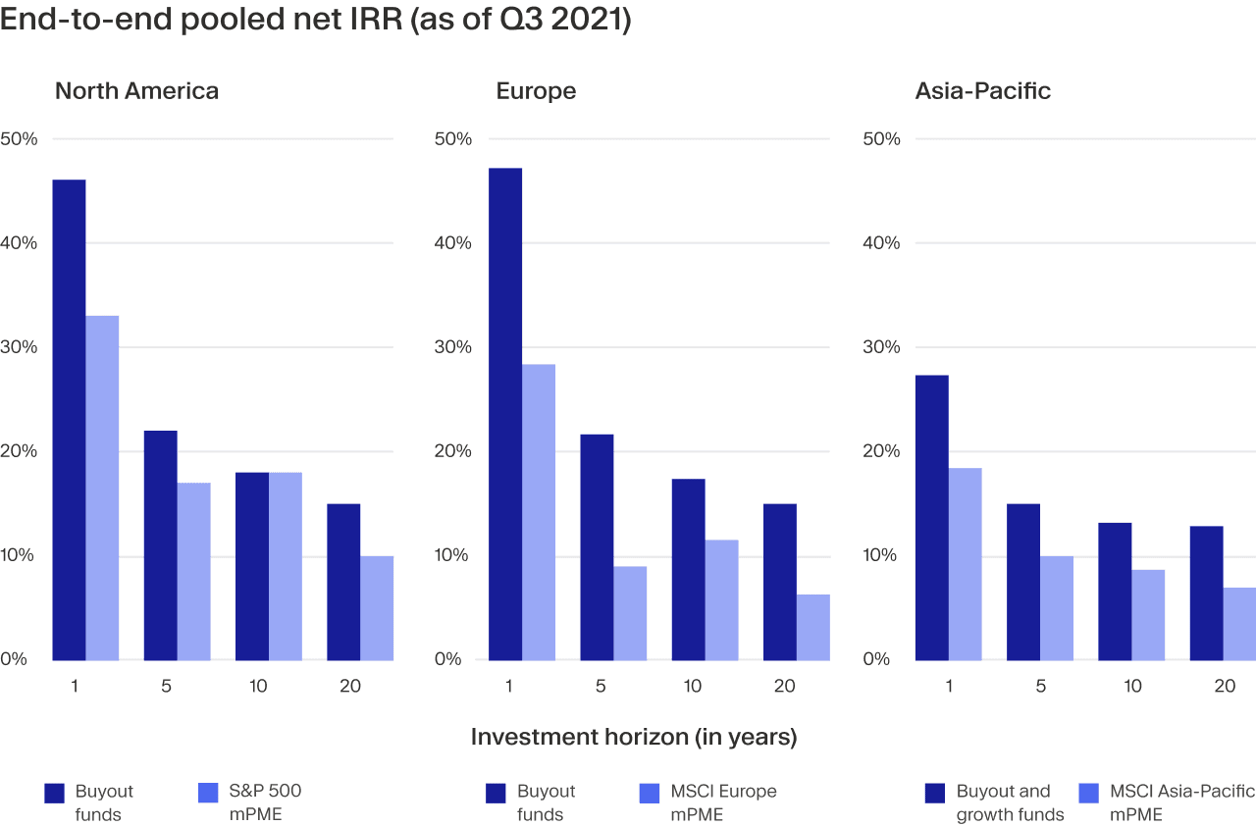

Bain Capital research highlights this ‘illiquidity premium’, showing that buyout funds in the US, Europe and Asia-Pacific are generating a stronger net pooled IRR than their public market equivalents across time periods.

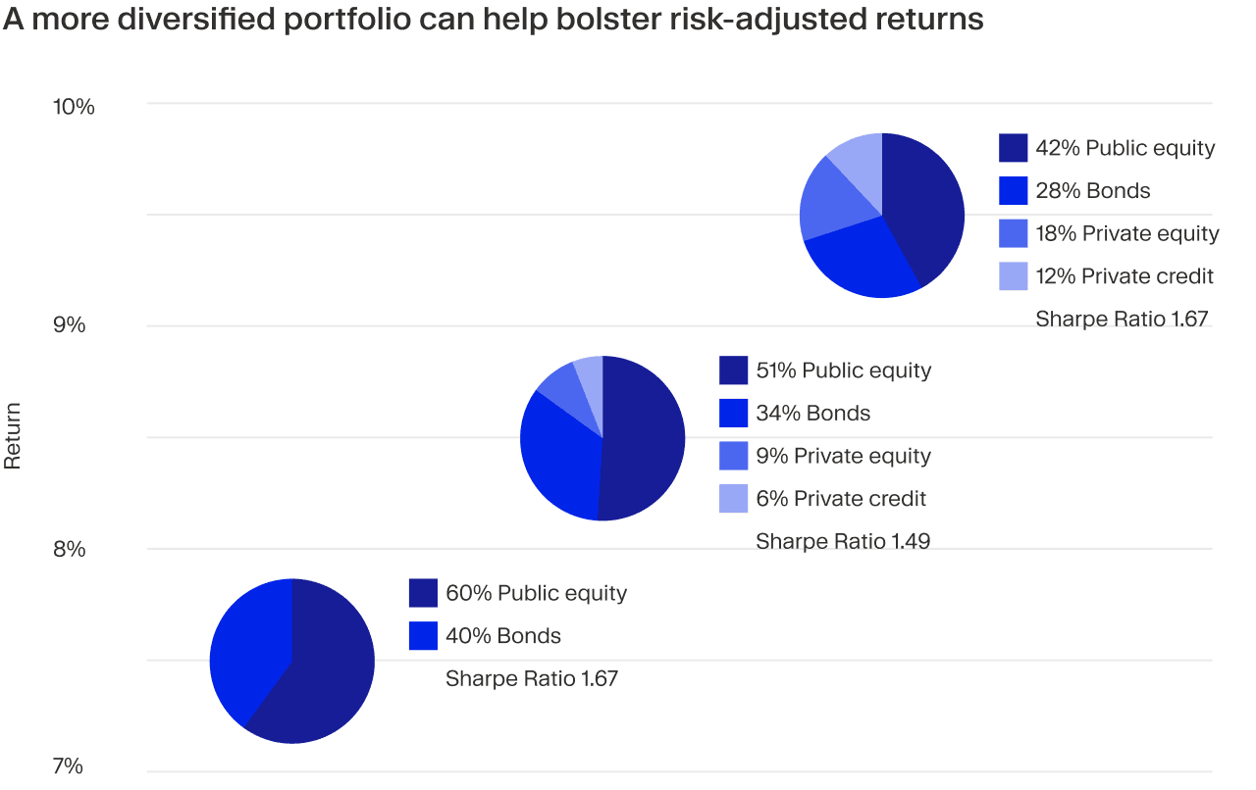

Diversification 2.0. Traditional methods of diversification by allocating across stocks and bonds no longer work in the current environment, as public equity and fixed income now track each other. Bolstering these portfolios with an allocation to private markets can provide a form of hedge against public market volatility, as well as boost risk-adjusted returns.

Learning to think long term

Even with these advantages in mind, locking your investable capital into a closed-end fund for a decade can be a difficult pill to swallow. However, private markets do have liquidity avenues that can help mitigate some of these concerns and provide peace of mind to some investors.

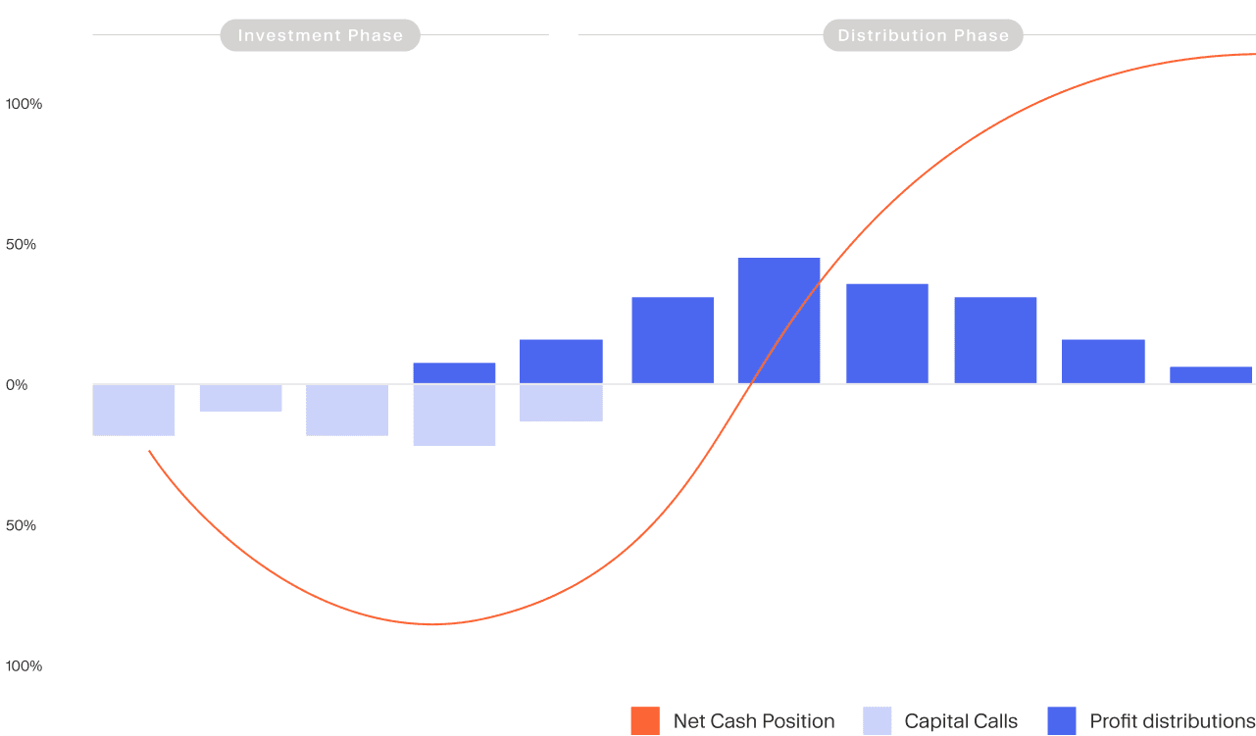

Commitments are spread out. The headline figure of a minimum private equity allocation, no matter how big or small, can be daunting for anyone approaching the asset class from traditional investable markets. However, it’s important to remember that this is the total, not what is due up front.

Instead, private equity draws down commitments gradually via capital calls, usually over a period of between two to six years. For investors, this has a number of benefits. Firstly, it significantly reduces the amount of their capital that is locked up at any set time, giving them more control over how to manage their cash flow — including deploying uncalled capital elsewhere if desired. Additionally, the multi-year staging of commitment and deployment reduces the impact of market fluctuations by investing throughout the economic cycle.

PE portfolios can become self funding. Fulfilling commitments in installments over several years doesn’t just mitigate an investor’s initial capital outlay. Over time, as the PE fund begins distributing, these early returns maybe used to pay for capital calls later in the cycle.

This profile of a PE fund, known as the ‘J-curve’, means that this portion of a portfolio can effectively become self-funding. Take a deeper dive into how this works in our white paper.

Secondary markets act as a release valve. The lack of price discovery in private markets does make exiting investments trickier for those who may need to realise liquidity earlier than originally intended. This is exacerbated in the current economic climate, with tighter exit windows making GPs hold onto companies longer than they would like, reducing their ability to create added value. Demand for earlier access to liquidity is therefore coming from GPs and LPs alike.

This has led to a recent boom in secondary market funds, specialist investors looking to buy stakes in either private companies or multiple fund interests from those with a need to sell. For GPs and LPs, this provides an avenue to realise liquidity for rebalancing portfolios, meeting distribution payments or, for individuals at least, helping to fund something that life has thrown their way.

For the secondary fund meanwhile, the agreement can give them access to quality private companies or funds at a discount. Investors in secondary funds themselves also benefit by gaining access to a portfolio of more mature private assets, mitigating the initial negative phase of the J-curve cycle.