Key takeaways

- Private equity dealmaking activity picked up last year, driven by stabilising interest rates, greater credit availability and narrowing valuation gaps.

- While exit activity also rose, the gap between US and European company sales was significant.

- Global fundraising declined, with capital continuing to flow into the hands of established managers with multi-strategy platforms.

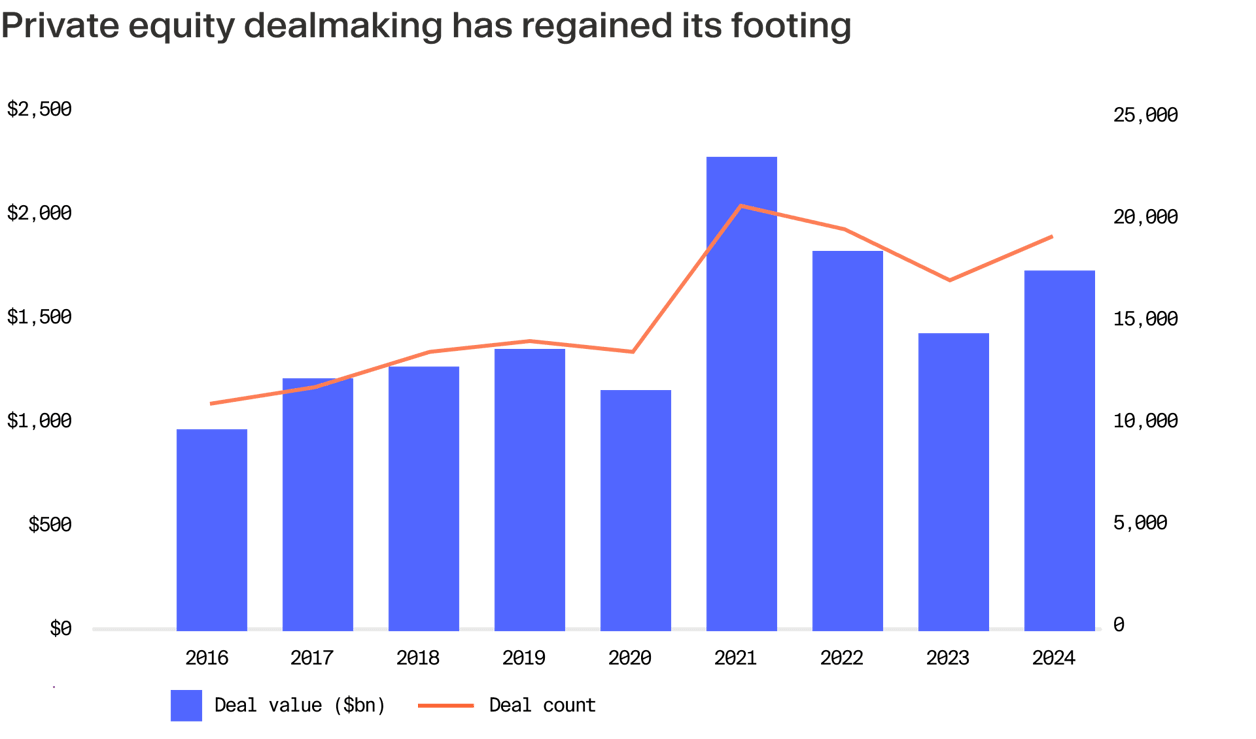

After two sluggish years, private equity dealmaking staged a confident comeback in 2024, as stabilising interest rates, improved credit availability and narrowing valuation gaps unlocked pent-up demand.¹

Transaction volumes and deal values climbed across key markets, with Europe seeing particularly strong growth — deal value surged by 35.4% and transaction count was up 18.2%, according to Pitchbook.²

While public market strength pushed asset prices higher, take-privates were a key driver of capital deployment, underscoring PE’s time-tested ability to capitalize on valuation dislocations. US bidders showed a keen interest in European buyouts, accounting for a fifth of all value in the region.³

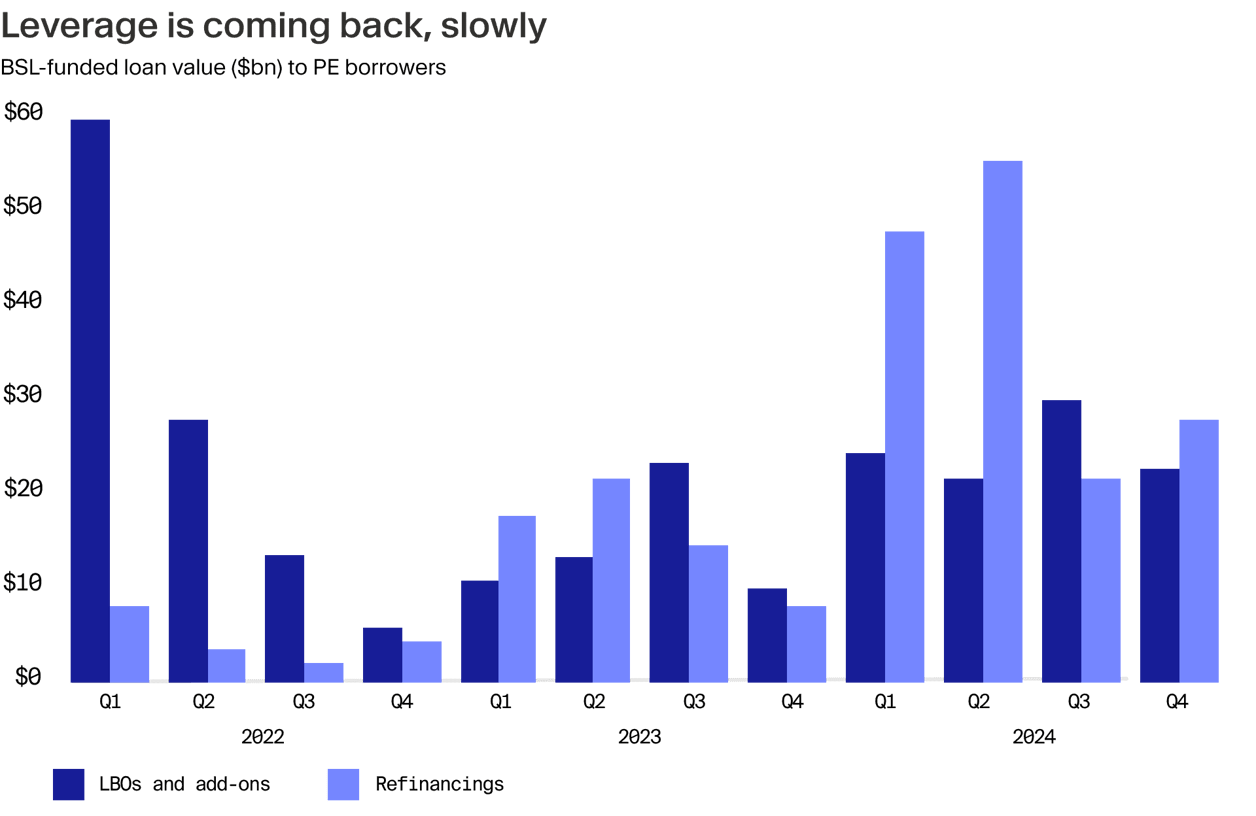

Leverage is creeping back, though refinancing dominates

The broadly syndicated loan (BSL) market regained momentum in 2024, fuelled by banks’ renewed appetite for leveraged buyout financing and a historic wave of refinancing that shattered previous records. LBO loan volumes doubled to $60.3 billion, though remained well below pre-pandemic levels and 59% less than the 2021 peak, according to Pitchbook.⁴

While banks competed with private credit lenders for deals, issuance was largely driven by refinancing, which nearly doubled for the second consecutive year, reaching $259 billion. This surge pushed BSL volumes past their previous 2013 record of $213 billion. Refinancings now make up almost two-thirds of BSL issuance.⁵ With fewer PE-backed companies changing hands, sponsors turned to refinancing as a stopgap measure, extending debt maturities rather than exiting at below-target valuations.

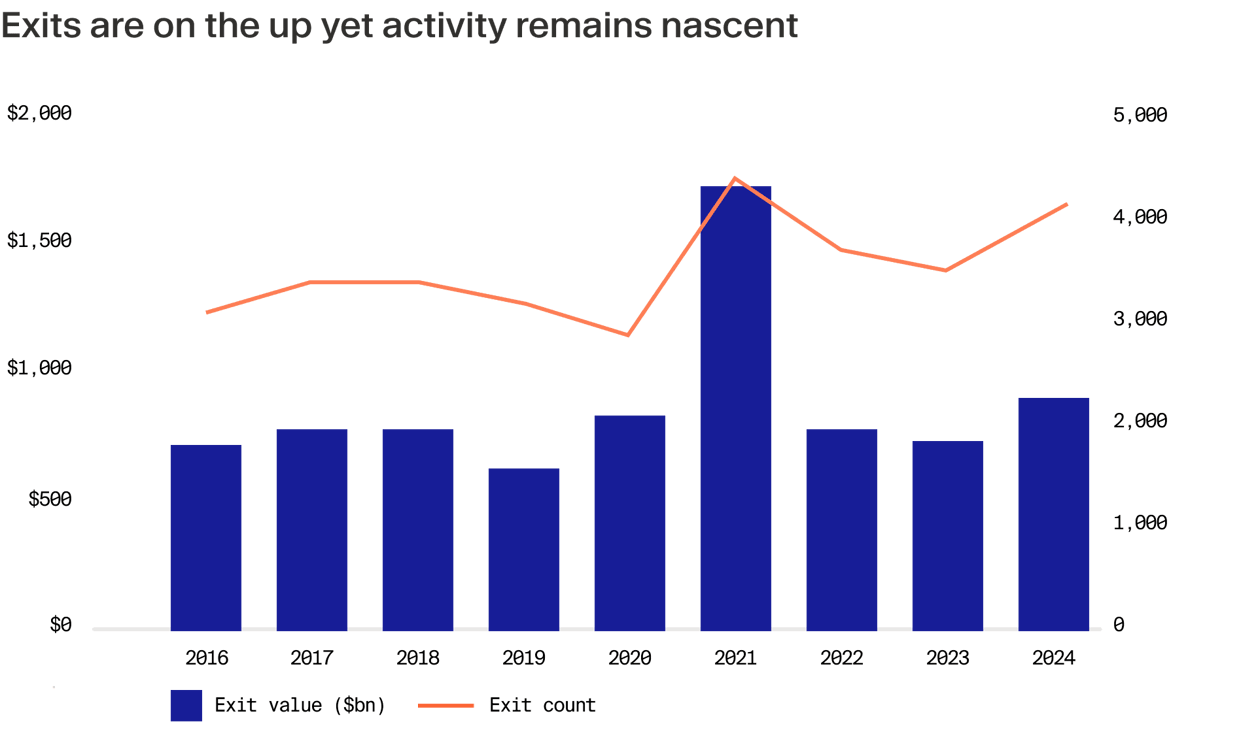

Exits recover, but the gap between the US and Europe is wide

Following a lacklustre period, exit markets began to show some buoyancy in 2024, especially in the US. Global exit value rose 19.6% on the previous year to $902 billion and deal count was up by 9.3% to 3,796 company sales.⁶ The contrast between the US and Europe was stark, however, the former’s aggregate exit value surging by 49% versus just 5% in Europe.⁷ ⁸

Although both markets posted similar relative gains in volume, the US saw far higher aggregate exit value. This reflects a heavier weighting toward large-ticket disposals due to strong corporate M&A appetite and a nearly fivefold increase in IPOs of PE-backed companies.⁹ It is not by chance that this coincides with US equities outperforming the global average, with the S&P 500 gaining around 25% in 2024¹⁰ compared to MSCI All Country World Index’s 18.6%.¹¹

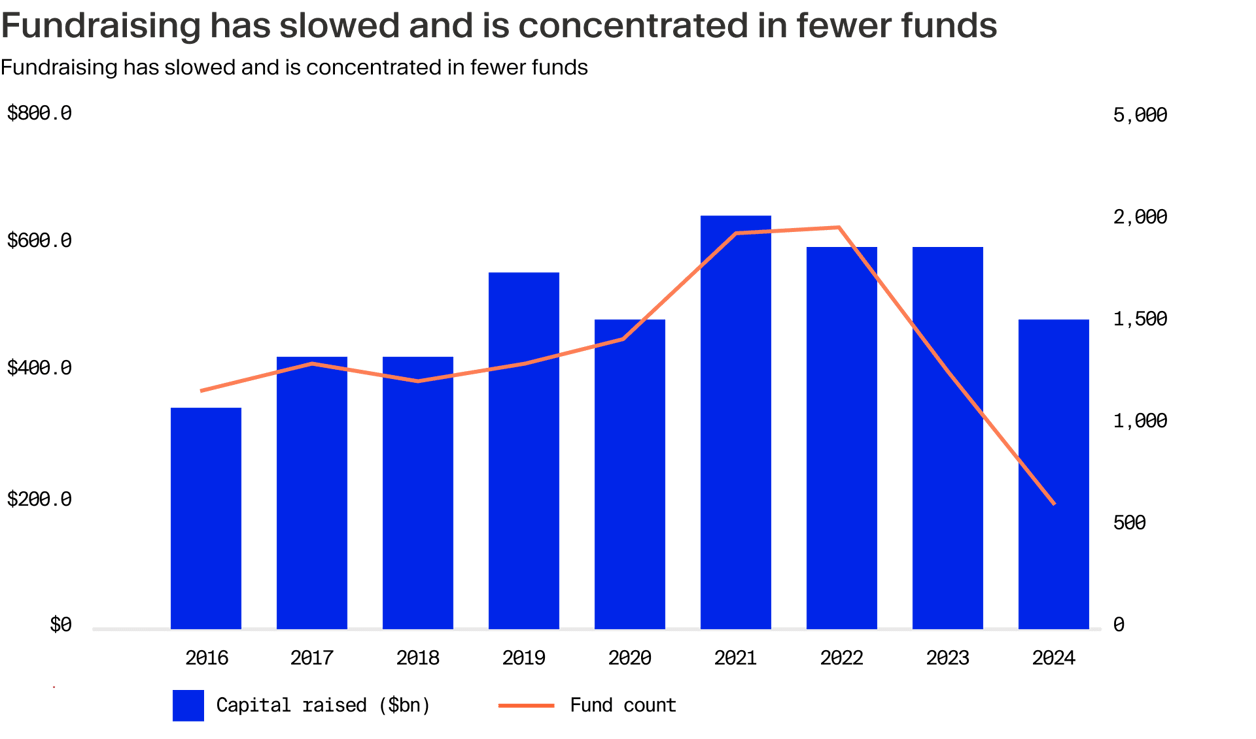

Fundraising falls as LPs double down on megafunds

PE fundraising declined in 2024 as global capital amassed fell 20% year-on-year to $476 billion.¹² The number of funds closed also plummeted by more than 48% to 531, the lowest reading since at least 2008, highlighting the increasing difficulty GPs are having in securing new money.¹³ This is not an industry-wide capital drought. Rather, a handful of megafunds continued to capture the bulk of capital commitments. Mid-market firms have struggled, as LPs continued to demonstrate a preference for established managers with multi-strategy platforms and unassailable track records.¹⁴ Notably, it was the US that led last year’s contraction. Fundraising value in the country regressed by 28% due to LP fatigue and distribution shortfalls.¹⁵ In contrast, fundraising in Europe was flat on the previous year¹⁶ thanks to bumper hauls from the likes of EQT Partners (EQT X, €22 billion)¹⁷ and Cinven (Eighth Cinven Fund, €13.2 billion)¹⁸. A meaningful exit market recovery can help to free up liquidity and deliver a more even distribution of commitments across the industry.

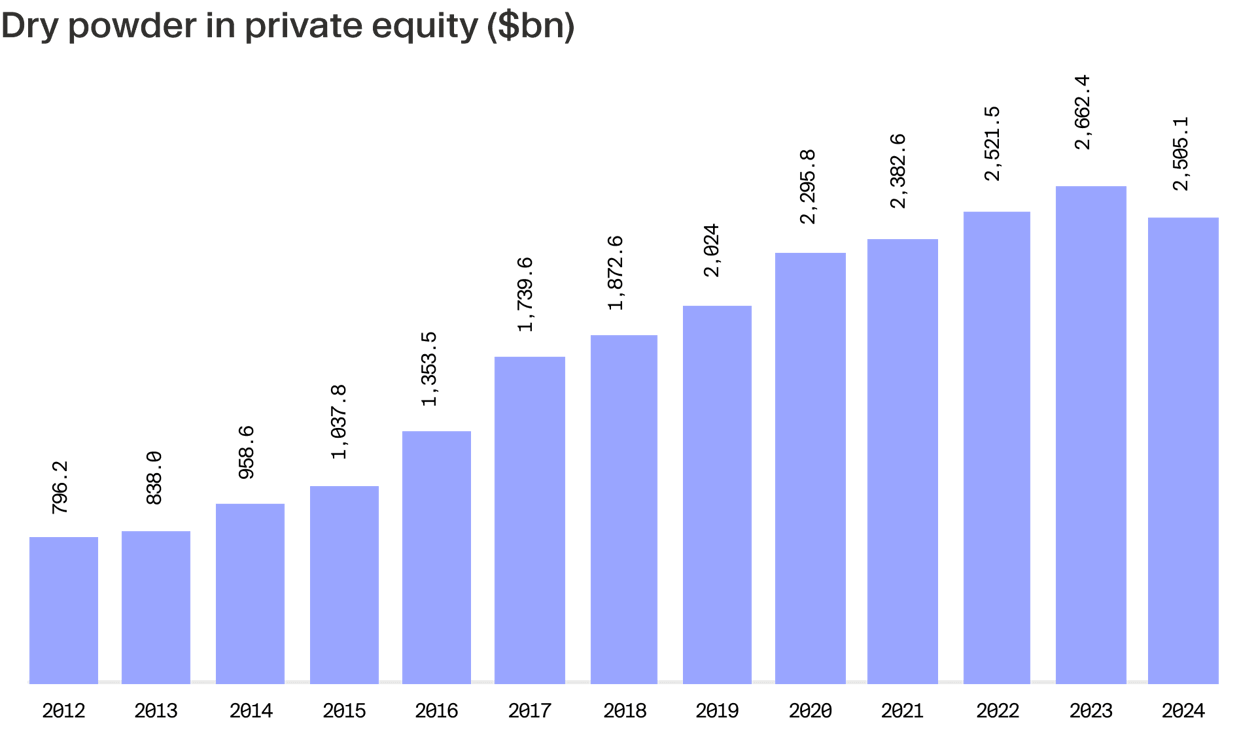

Dry powder dips for the first time in over a decade

For the first time in well over a decade, the industry’s collective stores of dry powder rolled over. Capital raised but not yet invested declined by approximately 6% to $2.51 trillion, reflecting the slower fundraising environment in the US, according to S&P Global.¹⁹

However, fundraising is an inherently lagging indicator²⁰ and last year’s slowdown in commitments was largely a reaction to 2022–2023’s weaker exit markets and attendant LP liquidity constraints.²¹ Provided exits accelerate and distributions improve, the fact that GPs are now more actively deploying capital could reignite fundraising momentum in 2025-2026. This could soon bring dry powder back in line.

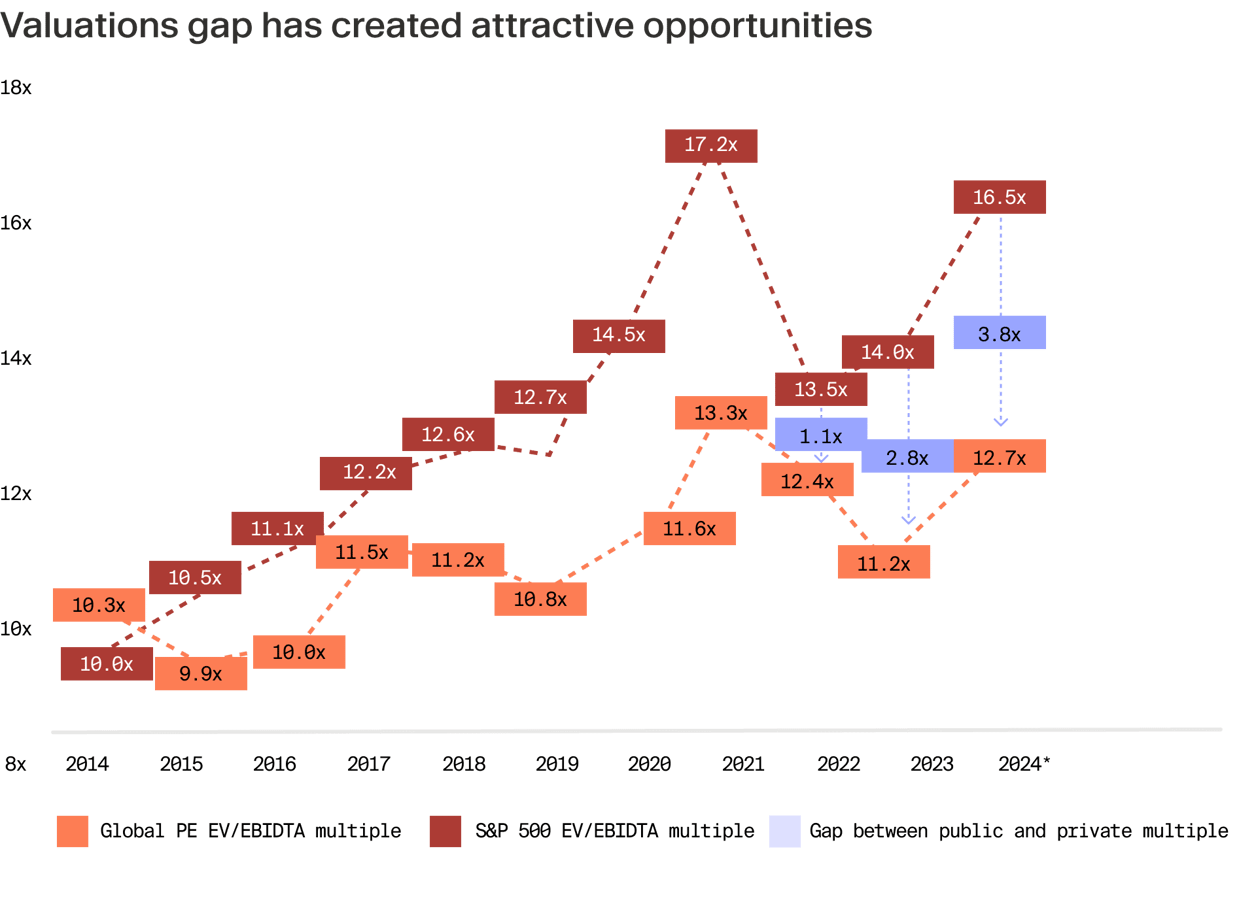

Valuations gap presents prime opportunity for PE

While private market multiples ticked up from their 2023 lows, the gap between public and private equity valuations extended to near-record highs last year, presenting a compelling investment opportunity. Public equities rebounded sharply, with S&P 500 EV/EBITDA multiples surging to 16.5x in 2024. Private equity has been slower to adjust, sitting at 12.7x, as highlighted in Blackrock’s graph below.²²

This 3.8x spread is the widest since 2021, when the market was distorted by excess liquidity. The gap reflects slower deal activity and continued caution in private markets, as buyers and sellers negotiate around shifting rate expectations. If credit conditions continue to improve and competition for assets rises, this spread is likely to compress — potentially driving stronger PE returns.

Europe’s take-private market is thriving

Private equity firms continued to act on valuation dislocations in public markets, making 2024 one of the strongest years for take-privates in Europe. A total of 52 such deals generated €58 billion in value, accounting for around a tenth of total PE deal value, according to Pitchbook.²³ The UK stood out, attracting nearly a third of the region’s take-private value, driven by structural issues with the London Stock Exchange (LSE).²⁴ A record 88 companies delisted or moved their primary listing away from the LSE, the largest net outflow since 2009, while only 18 new listings took place.²⁵ Across Europe, listed firms continue to trade at a discount to US peers, sustaining strong PE interest. As of late 2024, the UK equity market was trading at a discount of nearly 50% to the US benchmark, and the MSCI Europe ex-UK index at a discount of over 35%.²⁶ With ample dry powder and a persistent valuation gap to capitalise on, we believe this trend will continue in 2025.

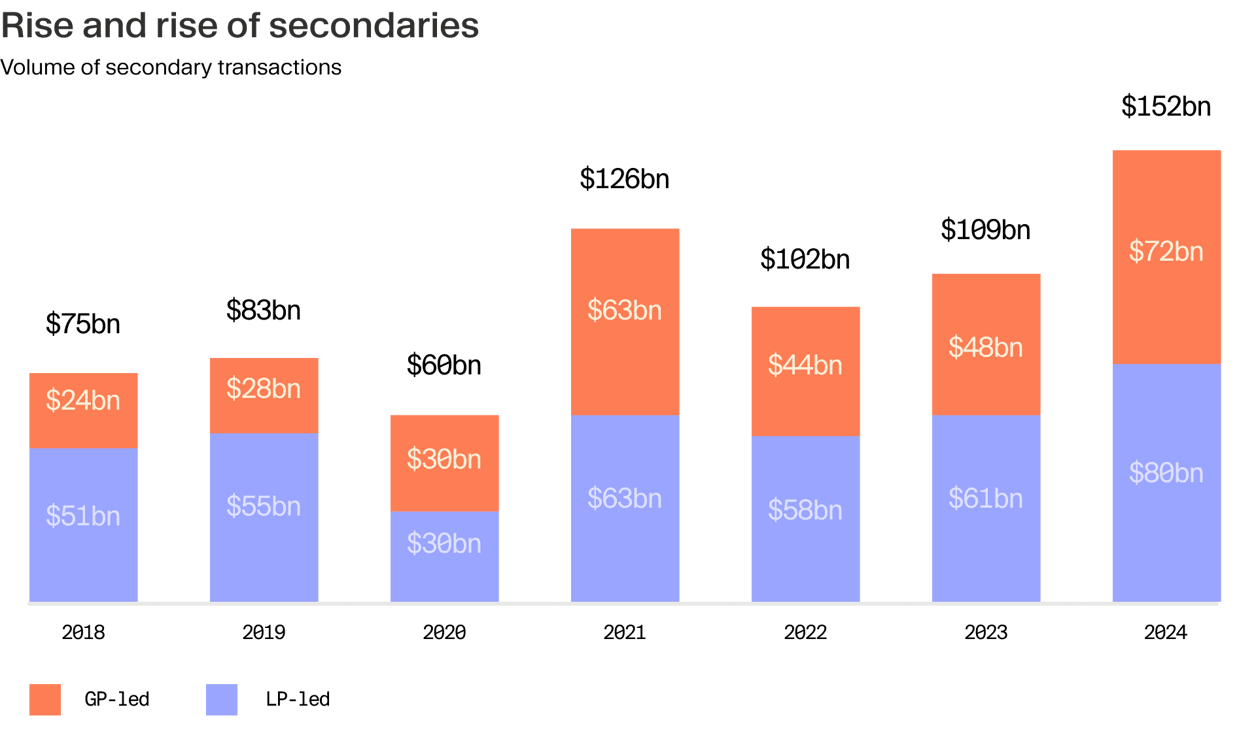

Secondaries hit record highs amid liquidity pressures

The secondary market soared to a record $152bn in 2024 — a 39% year-on-year surge that eclipsed 2021’s peak — as GPs and LPs sought liquidity amid constrained M&A and IPO channels.²⁷

GP-led deals dominated, with single-asset continuation funds surging, as sponsors held onto trophy assets rather than selling at depressed valuations. LP-led activity also grew sharply, driven by stagnant distributions and ongoing capital calls, prompting LPs to rebalance their fund portfolios via secondaries, according to a recent report from Lazard.²⁸

Bid-ask spreads narrowed as improved pricing visibility and increasing competition from buyers boosted transaction volumes. New capital from insurers and sovereign wealth funds further accelerated deal flow, which is providing liquidity for sellers and stabilising valuations.²⁹

Pricing trends reflect this dynamic, with buyout and growth capital assets seeing average gains of 2.6% and 5%, respectively.³⁰ Armed with $173 billion in dedicated dry powder at the end of 2024,³¹ the secondaries market will likely remain a critical pressure valve in 2025 even as traditional exits open up more fully. To learn more what the near future could have in store for secondaries, read our interview with Philip Meschke, Moonfare's Head of Investments.

Venture-backed startups are postponing IPOs

Many large tech firms continue to shun public listings,³² with some waiting for greater macroeconomic stability, while others prefer to prioritise revenue growth over the financial scrutiny of public markets.³³

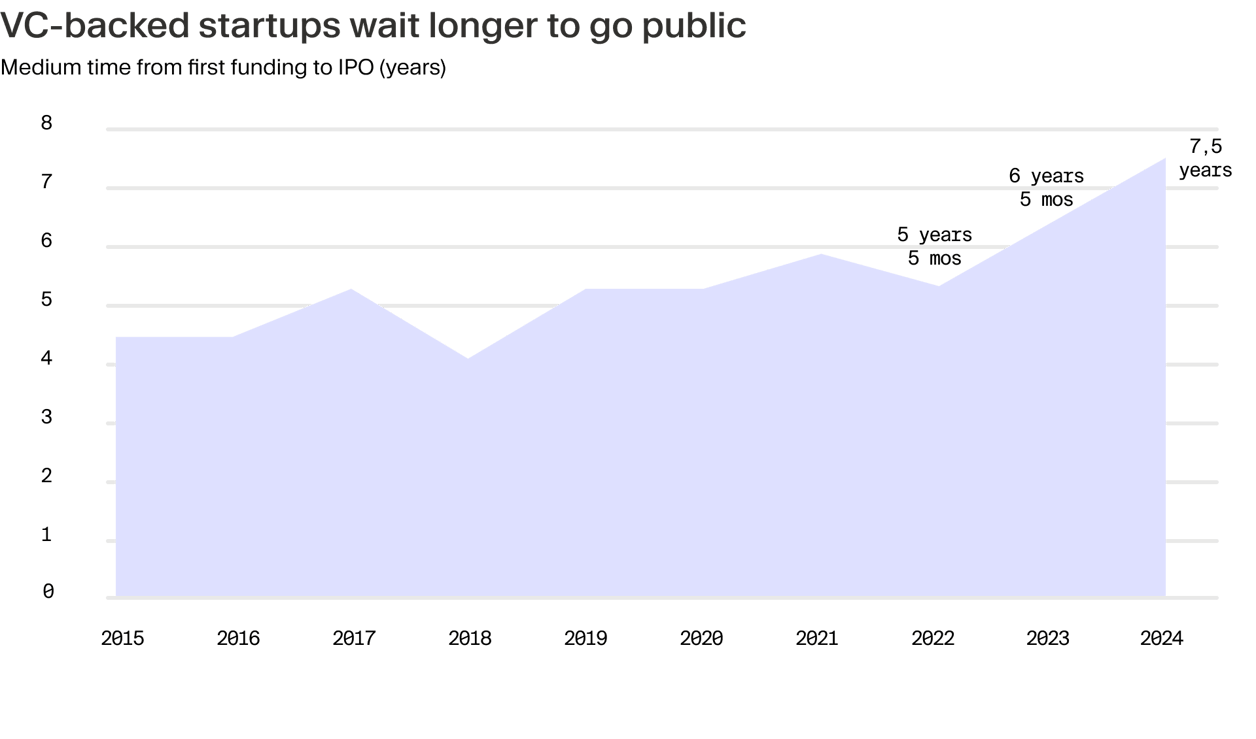

This trend has pushed IPO timelines to new highs. In 2024, the median time from first funding to IPO reached 7.5 years, up two years from 2022, according to CB Insights. While 2024 saw an uptick in IPO activity, volumes remain well below historical averages.³⁴

With startups sharply focused on scaling and strengthening market position, shareholders are turning to the direct secondary market. Instead of going public, some founders are selling equity stakes to institutional buyers while securing private capital to extend their cash runways and fund expansion.³⁵ Investors are responding to this demand — StepStone Group last year raised $3.3 billion for its dedicated venture secondaries fund, an industry first.³⁶ As companies stay private longer, private equity investors are finding more opportunities to back high-growth firms before they enter the public arena.

¹ https://pitchbook.com/news/reports/2024-annual-global-pe-first-look ² https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ³ https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ⁴ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ⁵ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ⁶ https://pitchbook.com/news/reports/2024-annual-global-pe-first-look ⁷ https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ⁸ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ⁹ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ¹⁰ https://www.spglobal.com/spdji/en/indices/equity/sp-500/#overview ¹¹ https://www.msci.com/documents/10199/a71b65b5-d0ea-4b5c-a709-24b1213bc3c5 ¹² https://pitchbook.com/news/reports/2024-annual-global-pe-first-look ¹³ https://pitchbook.com/news/reports/2024-annual-global-pe-first-look ¹⁴ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ¹⁵ https://files.pitchbook.com/website/files/pdf/2024_Annual_US_PE_Breakdown.pdf ¹⁶ https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ¹⁷ https://eqtgroup.com/news/eqt-x-hits-the-hard-cap-raising-eur-22-billion-usd-24-billion-in-total-commitments-2024-02-27 ¹⁸ https://pe-insights.com/cinven-raises-14-5bn-eighth-flagship-fund/ ¹⁹ https://www.spglobal.com/market-intelligence/en/news-insights/articles/2025/1/private-equity-backed-megadeals-jumped-higher-in-2024-87094719 ²⁰ https://www.bain.com/insights/stuck-in-place-private-equity-midyear-report-2023/ ²¹ https://pitchbook.com/news/reports/2024-annual-global-pe-first-look ²² https://www.blackrock.com/institutions/en-us/literature/whitepaper/2025-private-markets-outlook-stamped.pdf ²³ https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ²⁴ https://files.pitchbook.com/website/files/pdf/2024_Annual_European_PE_Breakdown.pdf ²⁵ https://www.rte.ie/news/business/2025/0106/1489304-london-stock-exchange-companies-exit/ ²⁶ https://am.jpmorgan.com/lu/en/asset-management/per/insights/market-insights/investment-outlook/equity-outlook ²⁷ https://www.lazard.com/research-insights/lazard-2024-secondary-market-report/ ²⁸ https://www.lazard.com/research-insights/lazard-2024-secondary-market-report/ ²⁹ https://www.lazard.com/research-insights/lazard-2024-secondary-market-report/ ³⁰ https://www.lazard.com/research-insights/lazard-2024-secondary-market-report/ ³¹ https://www.preqin.com/news/secondaries-in-2025-the-outlook-for-fundraising-deals-and-performance ³² https://www.ft.com/content/b9d7b633-c611-4c09-b02e-5855dfaa0dfb ³³ https://techcrunch.com/2024/12/17/its-dumb-to-ipo-this-year-databricks-ceo-explains-why-hes-waiting-to-go-public/ ³⁴ https://www.cbinsights.com/research/report/venture-trends-2024/ ³⁵ https://www.svb.com/business-growth/access-to-capital/venture-debt-reaches-record-high/ ³⁶ https://www.stepstonegroup.com/news-insights/stepstone-closes-largest-ever-venture-capital-secondaries-fund/