Key takeaways:

- Lower interest rates and a stronger IPO market are creating more favourable conditions for private equity exits, encouraging long-awaited liquidity events.

- The US stock market responded positively to the recent election of Donald Trump for a second term. Further improvement in the IPO market could be ahead amid improving investor confidence and anticipation of potential deregulation.

- Macroeconomic and geopolitical uncertainties pose ongoing risks that could impact the pace and success of exits in 2025.

With deal markets showing signs of thawing, one question is on everybody’s lips: when will exit markets kick back into gear?

When the pace of asset sales slows, as observed since 2021, distributions back to Limited Partners (LP) also decline, which can limit their capacity to commit fresh capital.¹ ² ³ Hence exit markets are being watched intently.

Critical context

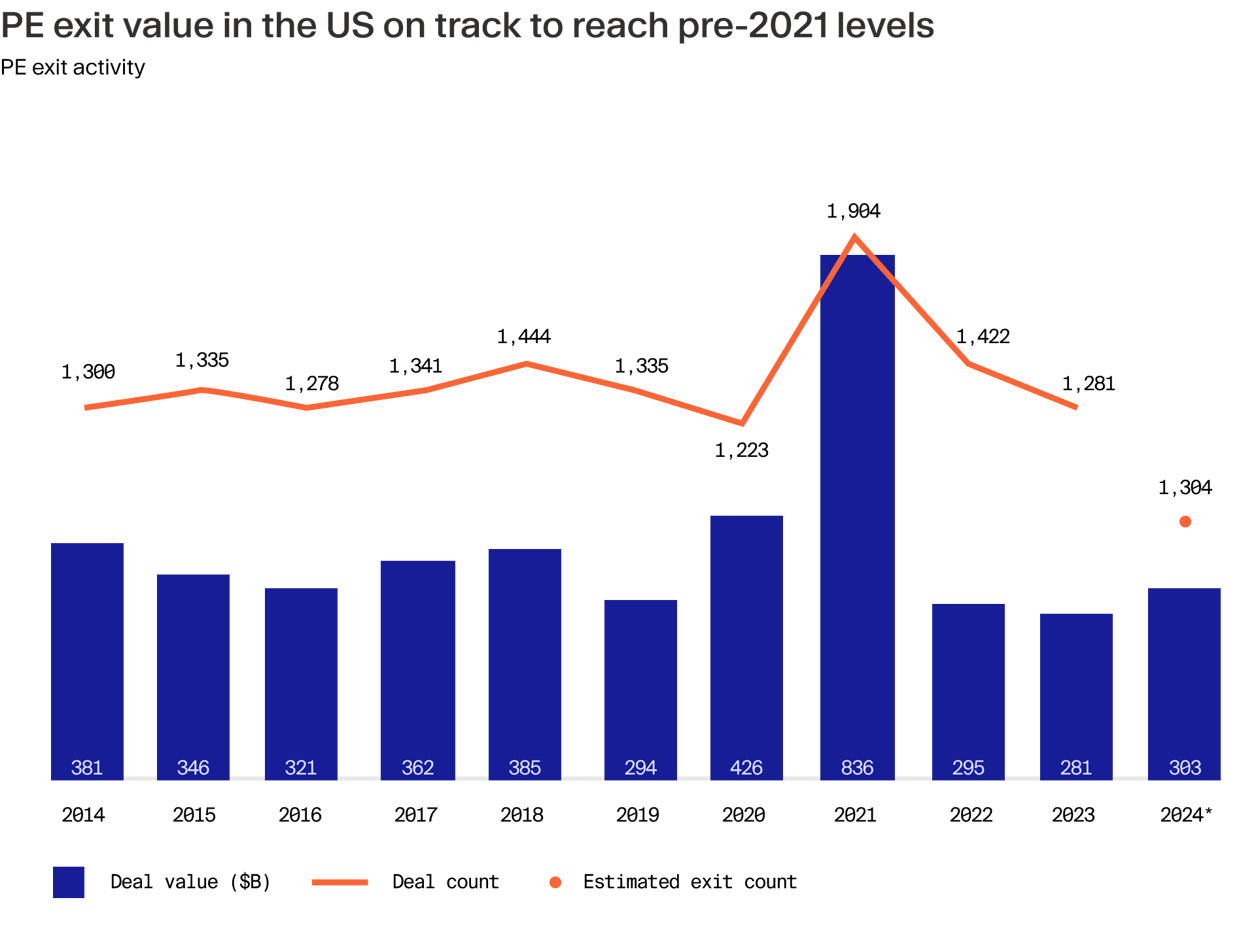

So far this year we’ve seen some encouraging signs. Private equity exit activity has shown improvement, especially in the US, where more favourable financing conditions and a somewhat more receptive IPO market are creating tailwinds. US private equity exits increased 51% in value in the first nine months of 2024 year-on-year,⁴ though Europe has been trailing.⁵

To understand the likely path ahead for exits, it’s important to consider underlying drivers. Lower debt costs generally stimulate deal markets, including exits. Indeed, as much as 40% of GPs have said the cost of financing is currently one of the top three challenges for exiting investments, according to a recent survey from Goldman Sachs Asset Management.⁶

In recent months, central banks across major economies have made multiple rate cuts, easing leveraged finance costs. In the US, the Federal Reserve reduced its target range by 50 basis points in September and further eased it by 25 basis points in November, setting the range at 4.5%-4.75%.⁷ The European Central Bank initiated 25 basis point cuts in both June and September, followed by an additional cut in October, bringing the main refinancing rate to 3.25%.⁸

These combined actions have contributed to lower costs for floating-rate leveraged finance instruments, which are the typical type of debt used in private equity buyouts. Issuance in US and European institutional loans and high-yield bonds surged 279% year-on-year in the first nine months of the year, to $1.4 trillion.⁹

This has primarily been concentrated around the refinancing and opportunistic repricing of higher-cost debt, indicating that PE firms are prioritising optimising existing portfolio company capital structures rather than aggressively pursuing new buyouts.

However, debt issuance to fund both M&A and LBOs has also picked up from 2023 lows.¹⁰ With expectations of further monetary easing and increased investor inflows into leveraged finance in search of yield as interest rates fall, firms may be positioning themselves for a more active acquisition and exit phase in the near future.

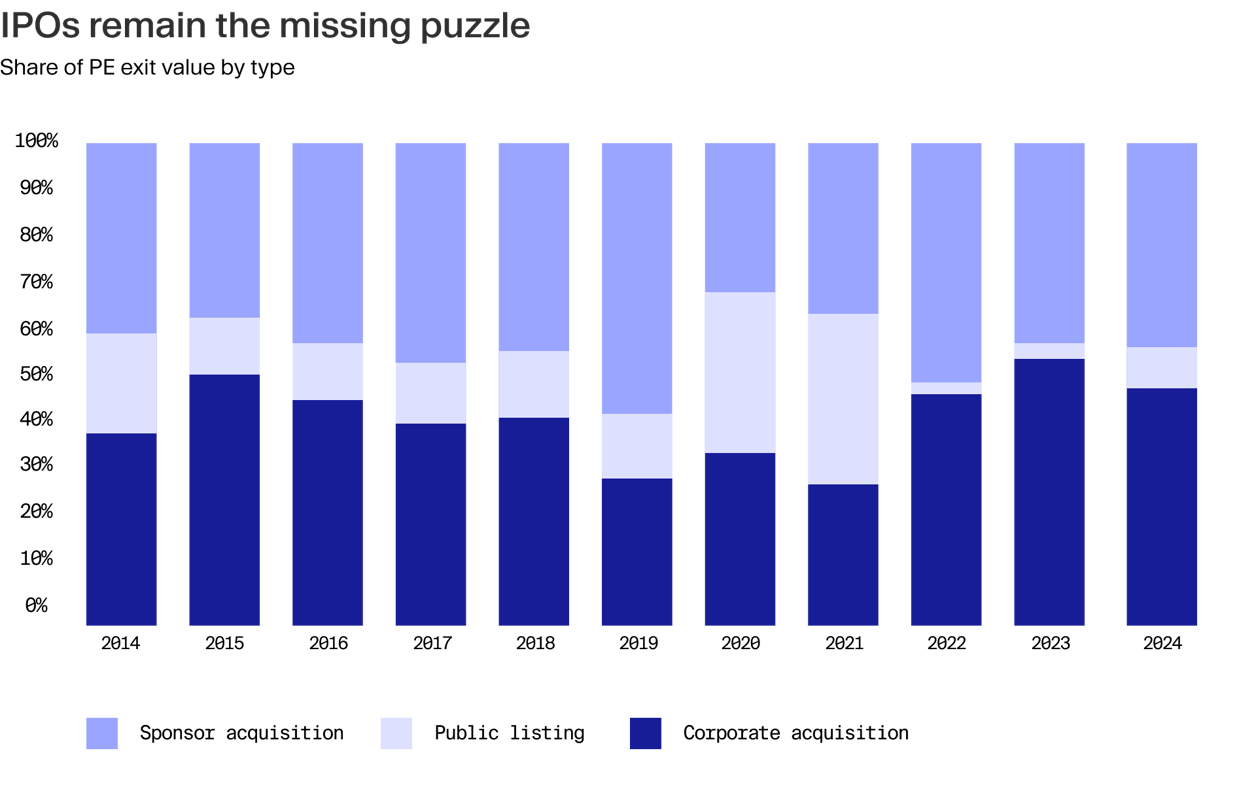

Brighter skies ahead for IPOs?

IPO markets have also been giving positive signals this year. In the Americas, proceeds in a period between January and September gained 37% over the same period last year, while in EMEA they were up by an even greater 45%.¹¹

Public listings by private equity sponsors have also improved notably in the US where they are on track for a 194% YoY growth,¹² while activity in Europe, on the other hand, has been more lacklustre.¹³

One successful example of a PE-backed public listings include Bay Grove Capital scoring a partial exit in July with the IPO of Lineage, the world's largest temperature-controlled warehouse real estate investment trust (REIT). The company raised $4.4 billion and secured a market cap of over $18 billion what was the biggest public offering since chipmaker Arm floated in September last year.¹⁴ In March, Reddit went public raising approximately $748 millionand valuing the company at around $6.4 billion. Notable venture capital backers of the popular social media platform include Andreessen Horowitz and Sequoia Capital.¹⁵

Meanwhile, many expect Donald Trump's victory in the US presidential election could support a wave of companies that had been hesitant to list publicly to go forward with IPOs in 2025.¹⁶ Indeed, PitchBook anticipates a significant uptick in activity, identifying at least 19 companies that could enter public markets within the year.¹⁷

Investors have also been encouraged by the stock market's ebullient response to the election outcome and the president-elect's commitment to deregulation. The Volatility Index, which measures market expectations of near-term volatility and is often referred to as Wall Street’s “fear gauge”, plummeted to its lowest level since September following Trump’s election.¹⁸ This is a short-term signal, but a positive one nonetheless.

GPs under pressure

Another reason to expect more exits in 2025 is the heavy pressure that GPs are under to return cash to LPs due to ageing portfolios. It is estimated that 46% of unsold PE-owned assets have been held for four years or longer, the highest proportion since 2012.¹⁹

In H1 2024, the median holding period of all PE assets sold was 5.8 years. This was a notable improvement on 2023, though the 7-year median at that time was an all-time record, illustrating that LPs have had to exercise patience in seeing realised returns.²⁰ This explains why investors have become focused on Distributed to Paid-In Capital (DPI), in addition to other return metrics that include unrealised gains.²¹ LPs are scrutinising how much cash their PE managers have managed to distribute before committing to new funds.²² This has also led GPs to explore other avenues to liquidity.

Sustained secondaries

With an estimated $3.2 trillion tied up in unrealised PE portfolios,²³ GP-led continuation funds and other secondary liquidity solutions have become increasingly popular and there’s little reason to expect this to change. In the first nine months of 2024, PE secondaries fundraising set pace, reaching $76.6 billion, slightly surpassing the $76.3 billion raised in the same period in 2023. This impressive total was driven largely by a standout Q3, in which secondaries funds secured $38.8 billion — almost matching the entire amount raised in the first half of the year.²⁴ After a slower start, Q3's surge reversed the earlier trend of year-on-year declines and marked the strongest Q1-Q3 period for secondaries fundraising in the past five years.²⁵

Secondaries have served as an important source of liquidity in the tougher exit environment of the past three years, as LPs clamour for cash.²⁶ With dry powder continuing to pour into this segment of the PE market, buy-side demand for assets should keep secondary dealmaking momentum high regardless of whether traditional exit routes open up more fully in the coming months.

Lingering risks

It seems as though conditions are ripe for an exit revival, but that’s not a guaranteed outcome. Lower debt costs are no panacea, with 58% of GPs in Goldman Sachs’ survey citing macroeconomic uncertainty and 53% citing valuations as significant challenges for exits.²⁷ Inflation, though tempered, remains a potential threat as interest rates fall. This is even more true for the fact that the US president-elect has once again made trade tariffs central to his manifesto.²⁸ These import restrictions would raise the price of goods, potentially leading businesses to pass these costs on to consumers, which in turn could refuel inflation pressures.

Geopolitical uncertainty is also unavoidable and adds yet another layer of risk. Ongoing conflict in Europe and the Middle East, trade disputes and fever pitch China-Taiwan tensions could throw a spanner in the works of exits. It’s hard to say with any confidence how these situations will develop over the next month, let alone the next year.

Next year outlook

With all that said, the outlook for exits is the best it has looked in a long time. As interest rates are moving down and IPO markets are gaining traction, private equity stands to benefit from more accommodating conditions for portfolio sales. If global deal markets continue to ease, GPs and LPs are poised for a more active year ahead.

Record high levels of secondary fundraising and improving liquidity options show that PE managers are ready to support exits by any means possible to unlock value for their investors. Thestage is set for a significant upswing in exit activity, offering private equity firms a chance to finally turn potential into concrete performance.

¹ https://citywire.com/wealth-manager/news/private-equity-fund-distributions-at-lowest-level-in-15-years/a2436016 ² https://files.pitchbook.com/website/files/pdf/Q3_2024_US_PE_Breakdown.pdf ³ https://files.pitchbook.com/website/files/pdf/Q3_2024_European_PE_Breakdown.pdf ⁴ https://files.pitchbook.com/website/files/pdf/Q3_2024_US_PE_Breakdown.pdf ⁵ https://files.pitchbook.com/website/files/pdf/Q3_2024_European_PE_Breakdown.pdf ⁶ https://am.gs.com/en-gb/institutions/insights/report-survey/private-markets-survey#header-gated-download-cta ⁷ https://www.forbes.com/sites/jasonschenker/2024/11/07/the-fed-just-cut-interest-rates-and-more-rate-cuts-are-coming/ ⁸ https://www.cnbc.com/2024/10/17/european-central-bank-october-meeting.html ⁹ https://ionanalytics.com/insights/debtwire/levfin-highlights-9m24/ ¹⁰ https://files.pitchbook.com/website/files/pdf/Q3_2024_US_PE_Breakdown.pdf ¹¹ https://www.ey.com/content/dam/ey-unified-site/ey-com/en-gl/insights/ipo/documents/ey-gl-ipo-trends-q3-v1-09-2024.pdf ¹² https://files.pitchbook.com/website/files/pdf/Q4_2024_PitchBook_Analyst_Note_Top_US_PE-Backed_IPO_Candidates_and_Outlook.pdf ¹³ https://files.pitchbook.com/website/files/pdf/Q3_2024_European_PE_Breakdown.pdf ¹⁴ https://www.rothschildandco.com/en/newsroom/insights/2024/09/ga_growth_equity_update_edition_30/ ¹⁵ https://www.reuters.com/markets/deals/reddit-set-hotly-anticipated-debut-after-pricing-ipo-top-range-2024-03-21/ ¹⁶ https://www.bloomberg.com/news/articles/2024-11-06/ipo-market-holdouts-look-to-2025-as-trump-retakes-white-house ¹⁷ https://files.pitchbook.com/website/files/pdf/Q4_2024_PitchBook_Analyst_Note_Top_US_PE-Backed_IPO_Candidates_and_Outlook.pdf ¹⁸ https://www.wsj.com/livecoverage/stock-market-today-fed-meeting-dow-nasdaq-sp500-live-11-06-2024/card/vix-fear-gauge-drops-after-clear-trump-victory-STqrret14S2URVmn5sPx ¹⁹ https://www.bain.com/insights/year-cash-became-king-again-global-private-equity-report-2024/ ²⁰ https://pitchbook.com/news/articles/pe-hold-periods-decline-signaling-improved-exit-activity ²¹ https://www.bain.com/insights/private-equity-midyear-report-2024/ ²² https://am.gs.com/en-ae/institutions/insights/article/2024/the-quest-for-liquidity-in-private-markets ²³ https://www.bain.com/insights/topics/global-private-equity-report/ ²⁴ https://www.secondariesinvestor.com/download-behind-q3s-massive-secondaries-fundraising-spike/ ²⁵ https://www.secondariesinvestor.com/download-behind-q3s-massive-secondaries-fundraising-spike/ ²⁶ https://www.commonfund.org/cf-private-equity/cash-is-queen-a-secondaries-article ²⁷ https://am.gs.com/en-gb/institutions/insights/report-survey/private-markets-survey#header-gated-download-cta ²⁸ https://foreignpolicy.com/2024/11/18/trump-tariffs-china-trade-economics/