Key takeaways:

- Sustained high interest rates have raised the cost of capital, slowing down the private market's natural lifecycle.

- Stubborn inflation in the US contrasts with Europe's declining inflation, potentially putting the two markets on divergent paths.

- However, global M&A shows signs of recovery, suggesting cautious optimism for private market activity.

Ever since the monetary tightening cycle kicked off in 2022, private markets have been constrained, with a couple of exceptions such as private credit and secondaries. In the buyouts space, generationally high interest rates have pinched dealmaking due to the higher cost of capital. This slowed the industry’s natural lifecycle.

Lower exit volumes mean less capital returned to investors, which in turn impacts upon raising fresh dry powder and deployment. However, there are signs that the cycle could begin to gain momentum once again.

Stubborn inflation and interest rate uncertainties

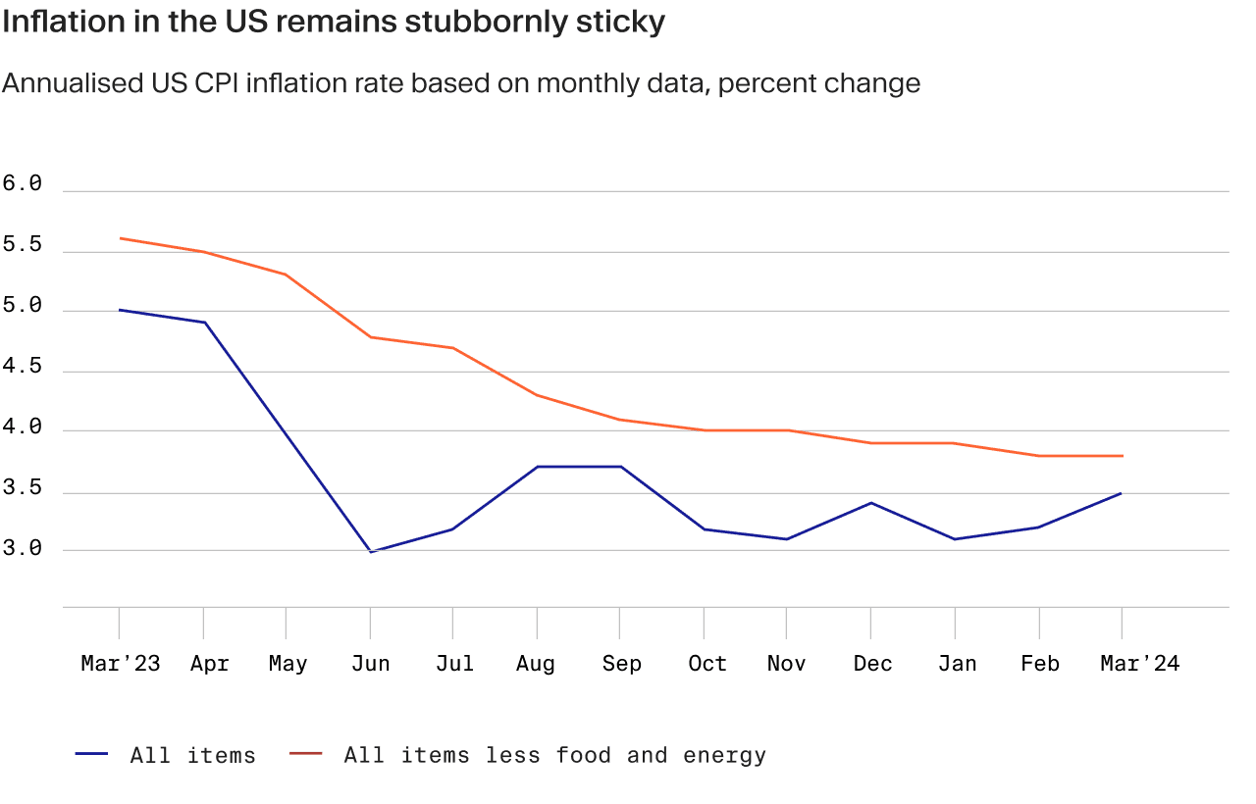

Interest rates remain a primary focal point for private market investors. The Federal Reserve, the most closely watched central bank in the world, maintained the federal funds rate at the range of 5.25% to 5.50% at its most recent meeting in the beginning of May.¹ Many were expecting a cut this quarter, with the June meeting seen as the point at which a Fed pivot would finally come. However, inflation remains stubbornly high. The US Consumer Price Index (CPI) advanced 3.5% annualised in March from 3.2% in February, the biggest gain in six months and the third consecutive reading above expectations.² This has called into question the assumption that inflation is steadily moving down, and is likely to postpone interest rate cuts in the US. Importantly, however, latest comments from the Fed don’t seem to suggest a rate hike either.³

In Europe, the odds of a June cut are higher than in the US. Eurozone inflation fell to 2.4% in March from 2.6% in February. With lower inflation and lower GDP growth, there is less impetus for the European Central Bank (ECB) to maintain its policy position. Therefore a 25 bps cut is still a realistic option for this quarter.⁴

A soft landing in sight?

Not long ago, many believed that high interest rates would likely lead to a so-called hard landing — a sharp downturn or recession. These sombre projections are increasingly looking over-baked. One of the more optimistic forecasters has been Goldman Sachs. The investment bank projects US GDP growth to tap a respectable 2.3% in 2024, above consensus, while unemployment will maintain below 4% and core inflation excluding food and energy falling to just above the Fed’s target of 2%. As a result, Goldman believes there’s only a small, 15% probability of recession in the US.⁵ Even more positively, the International Monetary Fund (IMF) in April sharply revised its US growth outlook up from 2.1% to 2.7%, citing the strength of the consumer and the labour market.⁶ Europe meanwhile is on a divergent path. The IMF expects eurozone growth to come in at 0.8% by year-end, which is still an improvement on last year’s 0.4% expansion.⁷ The region is contending with a confluence of long-term challenges including its energy dependency, ageing demographics, reliance on trade, lower levels of technological adoption and fiscal constraints. Weak consumer sentiment in both Germany and France are weighing on near-term growth, but any forthcoming easing from the ECB could provide some relief and help to stimulate household consumption. There’s some consternation around the Chinese economy as well. The Asian superpower has been drawing a lot of attention over the past year due to its hobbled real estate sector, which accounts for around 20% of its economy.⁸ The IMF expects China’s GDP to decelerate this year, with the country on course to log a 4.6% growth, a fall from 5.2% in 2023.⁹ Despite contrasting growth projections across major economies, there is every chance a broad soft landing is well within reach. While this will mean a more prolonged schedule for rate cuts, it’s a case of being careful what you wish for. The greater the need for deeper cuts, the greater the chances of recession, which would dent investor confidence. The prospect of gradual easing is the optimal outcome for private markets as it will provide more borrower-friendly financing conditions that are more conducive to dealmaking, and within a growth macro environment.

The risks of geopolitical tensions

A potential scupper to this promising trajectory are rising geopolitical tensions in the Middle East — in addition to ones already existing in East Europe. The ongoing conflict threatens to disrupt global oil supply chains, as about 20% of the world's oil supply passes through the Strait of Hormuz near Iran.¹⁰ Higher oil prices would translate to increased costs for fuel, energy, transportation and countless goods, putting upward pressure on inflation.

This precarious situation jeopardises central banks' careful efforts to tame inflation through interest rate hikes. If the conflict escalates further and sends oil prices higher, it could force central banks to maintain tighter rates for longer than anticipated early this year. This is arguably the biggest threat to the progress that has been made on inflation so far.

Green shoots

All of this paints a mixed and precarious picture. Inflation has not been equivocally tamped down just yet. However, markets appear to be frontrunning more accommodative macro conditions. Global M&A was up by 15% year-over-year in Q1 to $722 billion, even though deal counts fell.¹¹ This means that larger-ticket transactions are closing, which is being made possible by a return of leverage finance markets. US and European institutional loan and high-yield bond market issuance totalled $460 billion in the first quarter of 2024, representing a 230% year-on-year gain.¹² Admittedly, the vast majority of this has been directed at refinancing rather than supporting private equity funds’ LBO activity, but it’s a promising sign nonetheless that shows investors’ risk appetites are growing and there is a greater willingness to finance transactions as private equity deal flows recover. One voice that expects more private market activity going forward is AustralianSuper’s chief investment officer, Mark Delaney. Australia’s largest pension fund is actively scaling up its global direct investment capabilities in private equity under Delaney’s stewardship, with one of its most recent acquisitions involving a €1.5 billion minority stake in Luxembourg-headquartered data centre business Vantage EMEA.¹³ He told Bloomberg in April that he anticipates dealmaking will increase from here, adding: “We’ve seen the lows in private equity prices. Prices haven’t gotten as cheap as in previous downturns.”¹⁴

Outlook

The term “cautious optimism” may be a cliché, but it’s a fitting one at this juncture. The recent uptick in M&A value and easing of credit conditions in Q1 indicate a more positive outlook than was shared by dealmakers a year ago. Broadly speaking, things appear to be on the up, though market participants will be closely watching the price of oil given its potential to postpone looser financing conditions that would energise exits. Should exit activity begin to recover from here on out, it would provide the wind that has been missing from private equity’s sails, returning liquidity to investors and catalysing fundraising and deployment.

So far, that has been lagging. In Q1 in the US, for example, exit value fell 19% quarter-over-quarter to levels consistent with the past two years. Tellingly, the share of sponsor-to-sponsor exit value in the country hit an all-time low of 30.4%, indicating how interest rates are disproportionately hamstringing PE funds compared with corporate buyers.¹⁵ However, other exit channels appear to be thawing. In March, EQT Partners successfully floated Galderma on the SIX Swiss Exchange, the IPO giving the cosmetics business a valuation of more than €15 billion.¹⁶ The stock rallied nearly 20% on its debut and at the time of writing is trading at an all-time high.¹⁷ And in one of the largest sponsor-to-sponsor deals in Europe so far this year, Permira partially exited its position in Alter Domus to Cinven, the transaction valuing the fund administrator at €4.9 billion.¹⁸

If we are closer to the end of the monetary tightening cycle than the beginning, which many believe, expect exits to tick up as 2024 progresses.

¹ https://www.federalreserve.gov/newsevents/pressreleases/monetary20240501a.htm ² https://www.reuters.com/markets/us/goldman-sachs-raises-2024-gdp-growth-forecast-23-2024-01-15 ³ https://www.cnbc.com/2024/05/01/fed-meeting-today-live-updates-on-may-fed-rate-decision.html ⁴ https://ec.europa.eu/eurostat/web/products-euro-indicators/w/2-17042024-ap ⁵ https://www.reuters.com/world/imf-sees-slow-steady-2024-global-growth-china-inflation-pose-risks-2024-04-16 ⁶ https://www.imf.org/en/News/Articles/2024/02/02/cf-chinas-real-estate-sector-managing-the-medium-term-slowdown ⁷ https://www.euronews.com/business/2024/04/16/imf-outlook-eurozone-growth-set-to-rebound-but-inflation-at-risk-amid-middle-east-turmoil ⁸ https://ionanalytics.com/insights/debtwire/levfin-highlights-1q24-riding-the-refinancing-wave/ ⁹ https://www.reuters.com/markets/us/us-consumer-prices-rise-more-than-expected-march-2024-04-10/ ¹⁰ https://www.eia.gov/todayinenergy/detail.php?id=61002 ¹¹ https://ionanalytics.com/insights/mergermarket/ma-highlights-1q24-cautious-optimism/ ¹² https://www.reuters.com/markets/us/us-consumer-prices-rise-more-than-expected-march-2024-04-10/ ¹³ https://www.legal500.com/developments/press-releases/homburger-advised-australiansuper-pty-ltd-on-its-eur-1-5-bn-investment-in-vantage-data-centers-europe/ ¹⁴ https://www.bnnbloomberg.ca/australiansuper-plans-to-double-private-equity-assets-in-four-years-1.2057665 ¹⁵ https://pitchbook.com/news/articles/pe-exit-slowdown-2024 ¹⁶ https://www.reuters.com/business/retail-consumer/skin-care-company-galdermas-shares-soar-stock-market-debut-2024-03-22/ ¹⁷ https://uk.investing.com/equities/galderma ¹⁸ https://www.ft.com/content/cc3cb2e1-be2e-4252-8df1-5809a9ea8359