Key takeaways:

- Diversification: Allocation to an evergreen fund is almost immediately spread across different investment types, strategies and vintages.

- Portfolio management: Scaling and liquidity flexibility of evergreens can provide investors with granular control over exposure.

- Compounding: Gains are continuously reinvested, potentially amplifying long-term returns.

Evergreen funds have gone from niche to mainstream faster than most expected. As adoption grows, investors are refining how these investments fit into portfolios.

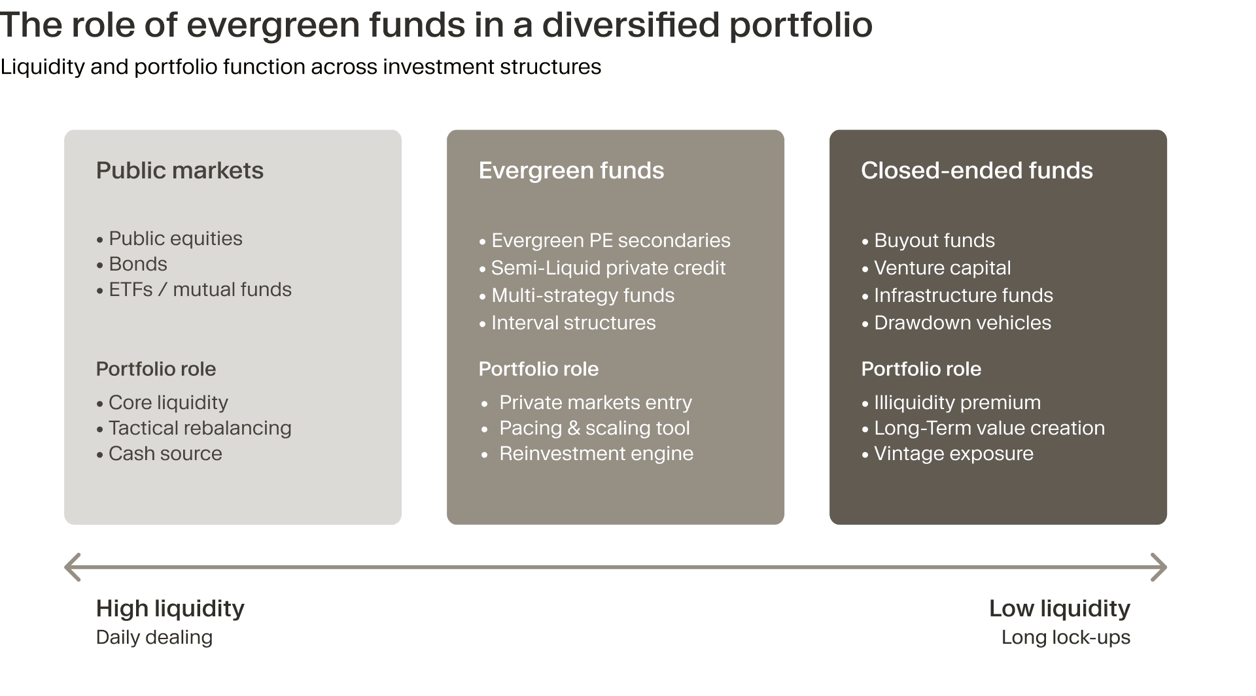

We believe closed-ended funds remain the primary vehicle for capturing illiquidity premia and maintaining core allocations to high-conviction managers. Evergreen funds play a structural role alongside them by improving diversification and addressing pacing, rebalancing and liquidity management.

Importantly, evergreen funds may serve distinct purposes depending on where an investor sits on the private market experience spectrum. For some, they are a starting point; for others, a portfolio refinement tool.

Entry point

For first-time investors, evergreen funds lower common barriers to entry. The 10-year fund term typical of traditional PE funds can feel daunting, particularly for those used to the daily liquidity of public markets. Evergreen structures lower this psychological barrier by offering quarterly or periodic exit windows.

Immediate diversification is another advantage. With their continuous deployment models, evergreens naturally distribute exposure across market cycles, strategies and vintage years. This may reduce concentration in any single market environment.

While traditional funds may take three to five years to fully invest committed capital, leaving investors with uncertain cash flow forecasting and the notorious J-curve of early negative cash flows, evergreens put capital to work from the first subscription date.

This means that less cash is sitting idle waiting for unpredictable capital calls, compressing the path to potential positive performance.

A path to private markets

Certain strategies are particularly well-suited to evergreen structures. Private credit's recurring income profile aligns naturally with liquidity windows, potentially allowing managers to meet redemptions without having to hold too much cash univested.

Secondaries strategies further optimise the evergreen model — mature, cash-generating portfolios reduce cash drag versus primary allocations and may accelerate compounding potential. Both provide immediate diversification while smoothing the cash-flow challenges that traditional structures create.

This flexibility allows evergreen funds to play a foundational role within a broader private markets allocation. Investors may choose to hold a baseline level of diversified PE exposure through an evergreen fund while making periodic investments into niche sector-, region- or company stage-specific drawdown funds. In this way, they can combine broad market access with targeted, high-conviction bets.

Pacing tool and allocation bridge

For sophisticated investors already managing complex, multi-asset portfolios, evergreens offer granular control over exposure. The ability to scale positions up or down, coupled with the option to use these vehicles as liquidity management tools within a broader allocation, provides tactical flexibility that traditional closed-ended vehicles typically don't have.

Proceeds from a drawdown fund distribution can be quickly reinvested into an evergreen opportunity, maintaining a target PE allocation without the cash drag of waiting for the next closed-ended commitment.

Compounding benefits

These evergreen mechanics also influence how capital is reinvested and compounded within private markets portfolios.

Rather than managing the cash flow cascades typical of traditional fund structures, investors can compound returns within the evergreen vehicle itself.

This feature addresses one of the more cumbersome aspects of private market portfolio management: the need to redeploy capital efficiently as underlying investments exit. Because of this, evergreen funds create a true compounding mechanism whereby gains are continuously reinvested, amplifying long-term returns.

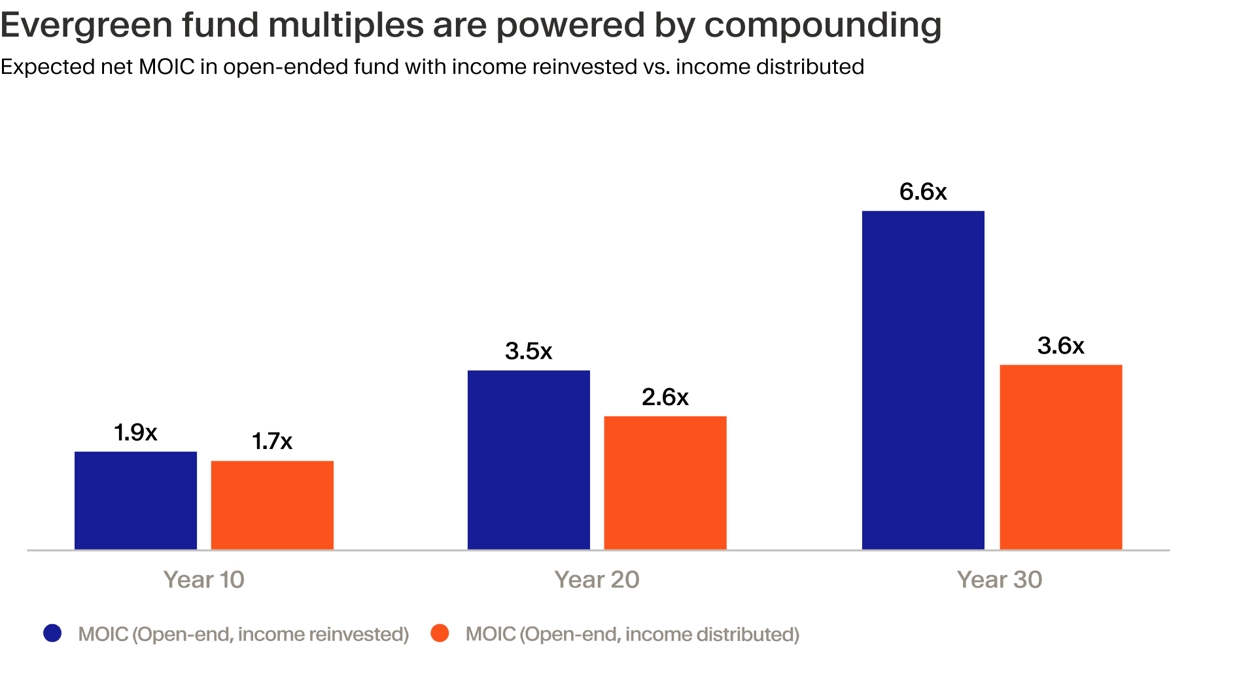

Compounding benefits should not be underestimated. Research demonstrates that consistent reinvestment in private markets over time can significantly improve long-term portfolio outcomes.

JP Morgan Asset Management has found that this effect widens the return gap significantly over longer horizons. Assuming a 6.5% total annual return, reinvested income produces a 6.6x MOIC by year 30 versus 3.6x for distributed income.

Comparing performance

Closed-ended funds report Internal Rate of Return (IRR), which factors in the timing of capital calls and distributions. Because these funds deploy capital gradually, IRR captures the J-curve effect with early fees and unrealised investments typically weighing on returns before exits begin to materialise.

Evergreen (and open-ended funds more broadly) report Time-Weighted Return (TWR), which measures compound portfolio growth assuming continuous full investment. This fits evergreen structures where capital is immediately deployed and income is reinvested.

The metrics answer different questions. For cross-fund comparisons, Money on Invested Capital (MOIC), which is the ending value divided by total capital invested and often simply called a cash multiple, provides a common benchmark independent of cash-flow timing.

Allocation strategy

There's no universal answer to how much should be allocated to evergreen funds. It all depends entirely on an investor’s specific goals, constraints and how far along they are in their private markets journey. Portfolios are not static, they are built, scaled and refined over time.

Early on, evergreen funds may play a somewhat larger role, providing immediate diversification while helping investors pace commitments to closed-ended funds gradually. As programmes mature, closed-ended funds typically take the lead for core return generation, while evergreen funds settle into a rhythm of maintaining steady capital deployment and liquidity optionality.

Maintaining allocation discipline over time

The true power of evergreen lies as much in what they enable investors to do as in what they enable investors to avoid: disrupting long-term allocation strategies due to short-term liquidity concerns. By allowing gradual scaling, rebalancing flexibility and disciplined reinvestment, these funds may help investors maintain target allocations rather than merely setting them.

Evergreens can also reduce the psychological friction that often undermines private market investing. They remove decision fatigue by automating reinvestment and eliminating the need to repeatedly select new funds. They lower timing anxiety by spreading entry points across vintages rather than concentrating in a single year.

Most importantly, they encourage staying invested, countering the tendency to retreat during volatility or sit on the sidelines waiting for optimal entry points that never arrive. This consistent participation, rather than misguided attempts to time vintage years, is what generates the most reliable long-term results.

What evergreen funds do not change

Flexibility, however, should not be confused with liquidity certainty. Evergreen semi-liquid funds are still private market investments and their periodic liquidity provisions come with important caveats that investors must understand.

Liquidity is typically offered quarterly or semi-annually, not daily. It is also subject to limits. Funds usually cap the percentage of assets that can be redeemed in any given period to protect remaining investors from forced asset sales.

Additionally, the success of any evergreen fund remains fundamentally dependent on the quality of its underlying assets. A poorly performing portfolio does not become attractive simply because it offers quarterly liquidity windows. Proper due diligence on investment strategy, manager track record and asset quality remains as critical as ever.