Key takeaways:

- Finance professionals are receiving some of the largest bonuses in years, with payout pools at record levels.

- Institutions separate irregular inflows into distinct buckets before investing, protecting liquidity while preserving long-term compounding.

- By allocating long-term capital to private markets instead of cash, individuals can access the same time-driven return engine institutions rely on.

Bonus season is upon us. After a strong year for M&A and trading, banking professionals are once again looking at meaningful compensation packages and will need to decide what to do with those proceeds.

But one question most will fail to ask is — what would an endowment or pension fund do with a sudden windfall?

The answer offers a guide that can transform episodic bonuses into lasting wealth.

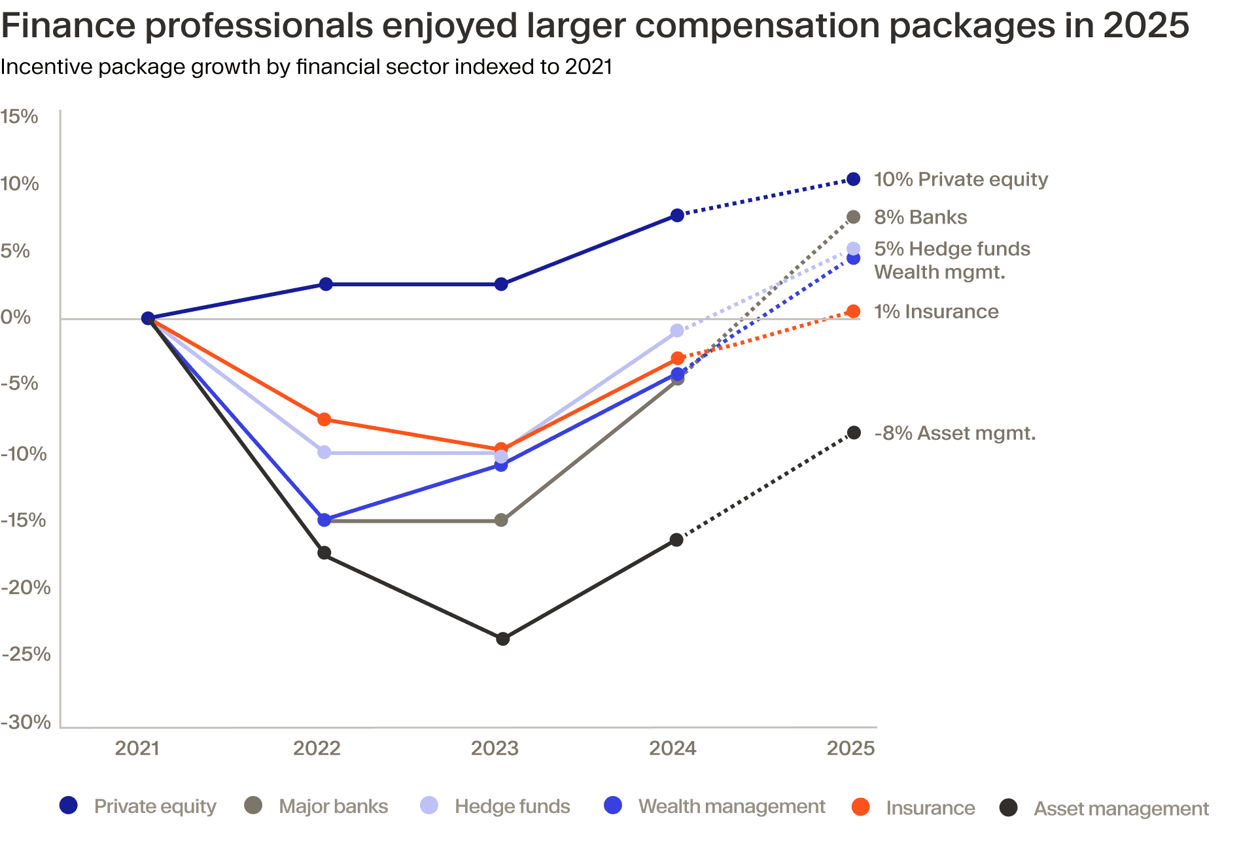

A bumper year

Wall Street bonuses are expected to rise for the second consecutive year, driven by surging deal volume and market volatility.

Fixed income sales and trading professionals could see increases up to 15%, while equity traders may enjoy gains of 15% to 25%, according to compensation consultancy Johnson Associates.¹ M&A advisory bonuses are projected to climb 10% to 15% which is the strongest showing since 2021.

Private equity presents a more nuanced picture. While larger firms may see bonus increases of 5%, mid- and small-cap firms are expected to remain flat. The standout performers? Secondaries professionals, who may enjoy bonuses upward of 10%, pushing up the average as firms increasingly turn to fund extensions and other liquidity solutions.

The scale is significant. In 2025, Wall Street's total bonus pool hit a record $47.5 billion,² with the average bonus reaching $244,700, up 31.5% from the prior year.

Across the Atlantic, London City workers anticipate a particularly lucrative season as new rules allow senior staff faster access to deferred compensation.³ In Germany, roughly two-thirds of banking employees expect to receive bonuses,⁴ (source in German) with Deutsche Bank raising its bonus pool to €2.5 billion, a 25% increase and the highest level in a decade.⁵

The gravy train may not last for long though. Increasing macroeconomic uncertainty, fuelled by sovereign bond market volatility and US stock markets stalling in recent months, may dampen future payouts, potentially making this year's bonus bonanza more lucrative than next year's.

Bonus behaviour

When windfalls arrive, behaviour tends to split between caution and consumption. UK research reveals that 70% of people prefer to save a surprise bonus rather than spend it, with 27% opting for bank accounts and 16% choosing long-term savings vehicles. Only 9% would invest in stocks or similar products, while 5% would treat themselves.⁶

Among financial professionals, the patterns are slightly different from Joe Public’s, but are surprisingly short-term. Forum discussions reveal a familiar cycle: tax-efficient accounts, property down payments, luxury purchases such as watches and engagement rings, and lifestyle spending on travel or personal events. Less typical but noteworthy uses include funding an MBA or seeding a side business.⁷ ⁸

Whether a banker or barista, most treat one-time bonuses as either immediate spending power or near-term savings, rarely as strategic capital.

The institutional approach

Pension funds, endowments and sovereign wealth funds don't receive bonuses. But they do manage irregular capital inflows and they've developed sophisticated frameworks for deploying them.

One of the core strategies is separating capital by function, not by amount. Institutions typically divide new capital into three distinct buckets before making any allocation decisions:

Spending capital: Money earmarked for near-term needs over the next 12–24 months. This sits in current accounts, high-interest savings, or short-term deposits. It's cash set aside for taxes, known expenses or planned purchases. The goal is liquidity and certainty, not return.

Liquidity capital: This preserves flexibility and prevents forced selling elsewhere in the portfolio. Institutions maintain emergency reserves in cash-like instruments, short-duration bond funds and highly liquid public assets. For individuals, this means having accessible buffers that prevent disrupting long-term investments during unexpected events.

Growth capital: This is capital that isn't needed in the near term and can remain invested through market cycles. It's the engine of wealth creation and it's where institutions differentiate themselves. For growth capital, institutions favour long-duration strategies where returns are driven by time in the market, not timing the market. This includes public equities held with multi-year horizons, but increasingly, it means private markets: private equity, private credit, secondaries and real assets.

The rationale is straightforward. Public markets offer liquidity but at the cost of volatility⁹ ¹⁰ and shorter-term performance pressures. Private markets demand patience, typically 7-10 years, but may compensate with reduced volatility, differentiated return streams and access to value creation that public markets cannot replicate.¹¹

Translating the framework

For bonus recipients, the institutional approach offers a clear decision tree. First, identify your spending capital. Set aside what you need for taxes, immediate obligations and near-term lifestyle decisions. Be realistic — this isn't the place for aspirational frugality.

Second, establish your liquidity capital. Maintain 3-6 months of expenses in accessible form. If you're planning major purchases within 2-3 years, include those amounts here.

Third, and this is where the transformation happens, allocate the remainder as growth capital. This is the institutional advantage. While peers park bonuses in savings accounts earning minimal returns, those taking an institutional approach can deploy into long-duration assets that can potentially compound through cycles.

However, this bucket must be treated as truly long term. The institutional framework is only effective if the separation of capital is respected.

The long game

Bonus season is a natural inflection point. The default path leads to incremental consumption or low-yield savings. The institutional path treats irregular cashflows strategically, separating spending needs from growth opportunities and matching time horizons to appropriate vehicles.

In an era of increasing market access for individual investors, the real differentiator isn't information or even capital, it's discipline. The ability to segment, delay gratification and let time do its work. A bonus is more than just compensation for last year's efforts. Deployed with an institutional mindset, it can be the foundation for the next decade's wealth.

Important notice: This content is for informational purposes only. Moonfare does not provide investment advice. You should not construe any information or other material provided as legal, tax, investment, financial, or other advice. If you are unsure about anything, you should seek financial advice from an authorised advisor. Past performance is not a reliable guide to future returns. Don’t invest unless you’re prepared to lose all the money you invest. Private equity is a high-risk investment and you are unlikely to be protected if something goes wrong. Subject to eligibility. Please see https://www.moonfare.com/disclaimers.