Key takeaways:

- Investors buy NAV-based shares, giving them immediate exposure to the portfolio, while new cash is invested gradually rather than all at once.

- A carefully constructed evergreen portfolio holds assets from multiple vintages simultaneously, reducing reliance on any single exit cycle.

- Managers may halt redemptions temporarily under exceptional circumstances to prevent later investors from inheriting a portfolio of forced sales.

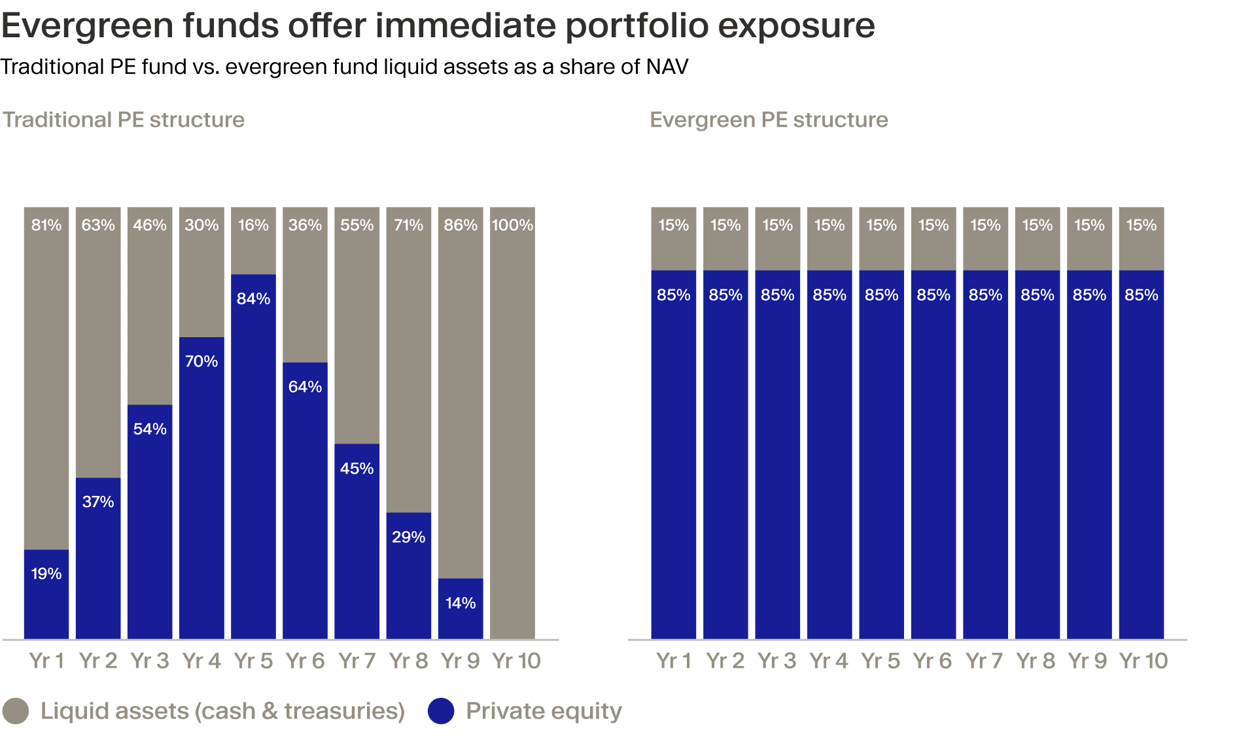

Traditional private equity funds ask investors to commit for ten years and wait for the next vintage. But not every investor can predict their liquidity needs a decade in advance.

Evergreen funds may solve this by translating private market returns into a structure that accepts capital continuously, recycles it for compounded returns and offers partial periodic liquidity for those who need it.

With evergreens becoming a private markets mainstay, the following five characteristics explain how these vehicles actually function in practice, why certain safeguards exist and what the structure means for capital deployment and returns.

Staged deployment

Evergreen funds accept capital continuously, typically monthly or quarterly, rather than restricting entry to specific, one-off fundraising windows.

Investors subscribe at the fund’s net asset value (NAV), which represents the fund’s total assets spanning both the private portfolio and cash reserves, minus any liabilities, divided by the number of shares outstanding.

When new capital arrives, it flows directly into the liquidity sleeve – the pool of cash and short-term instruments maintained to meet redemptions and fund new investments.

Subscribers receive shares priced at the current NAV, granting immediate exposure to the entire existing portfolio, including the underlying private companies.¹ While the specific cash contribution initially sits in the liquid reserve, the investor participates in the fund's full return through their share ownership from day one.

The fund manager deploys fresh capital from incoming investors into new private investments as and when opportunities arise. This pacing prevents the fund from rushing into deals simply to put money to work, while shareholders still capture returns from the established holdings.

The liquidity sleeve keeps things moving

Every evergreen fund maintains a liquidity sleeve, combining cash on hand, undrawn credit facilities, secondary market positions and shorter-duration assets to meet redemption requests without forcing premature sales of core private investments.

A well-built liquidity sleeve serves two purposes. It provides flexibility to handle withdrawals, while allowing the main portfolio to stay locked in long-term, value-creating investments. The composition of the sleeve matters enormously. Cash offers a degree of certainty as it is available regardless of market conditions. Mark-to-market assets such as liquid credit offer higher yields than cash, helping to offset the return drag of maintaining a liquidity buffer.

There is an inevitable cost to this safety. Liquidity sleeves typically generate lower returns than the fund's core private equity investments. Too much cash drags on overall performance, while too little risks may force asset sales during downturns. The art of managing these unique funds lies in maintaining this buffer — keeping enough dry powder on hand to simultaneously honour withdrawal requests and make new investments.

Even the most carefully managed sleeve can only handle short-term liquidity needs. For the structure to remain viable over years and decades, another source of cash is needed to replenish the reserves.

Realisations drive long-term liquidity

Ultimately, the long-term sustainability of these vehicles depends on exits. Evergreen funds generate distributable cash through portfolio company sales and dividend recapitalisations from underlying assets.

The inherent challenge here is timing. Redemption rights are periodic and predictable, while private market exits can be lumpy and uncertain. Managers address this mismatch through diversification: spreading investments across vintages, sectors and strategies to create a rolling realisation profile rather than a single J-curve concentration.

A carefully constructed evergreen portfolio holds assets from multiple investment years simultaneously. While one vintage may still be in its value-creation phase, another may be generating distributions. This should reduce reliance on any single exit cycle and produce a more consistent stream of cash flows over time.

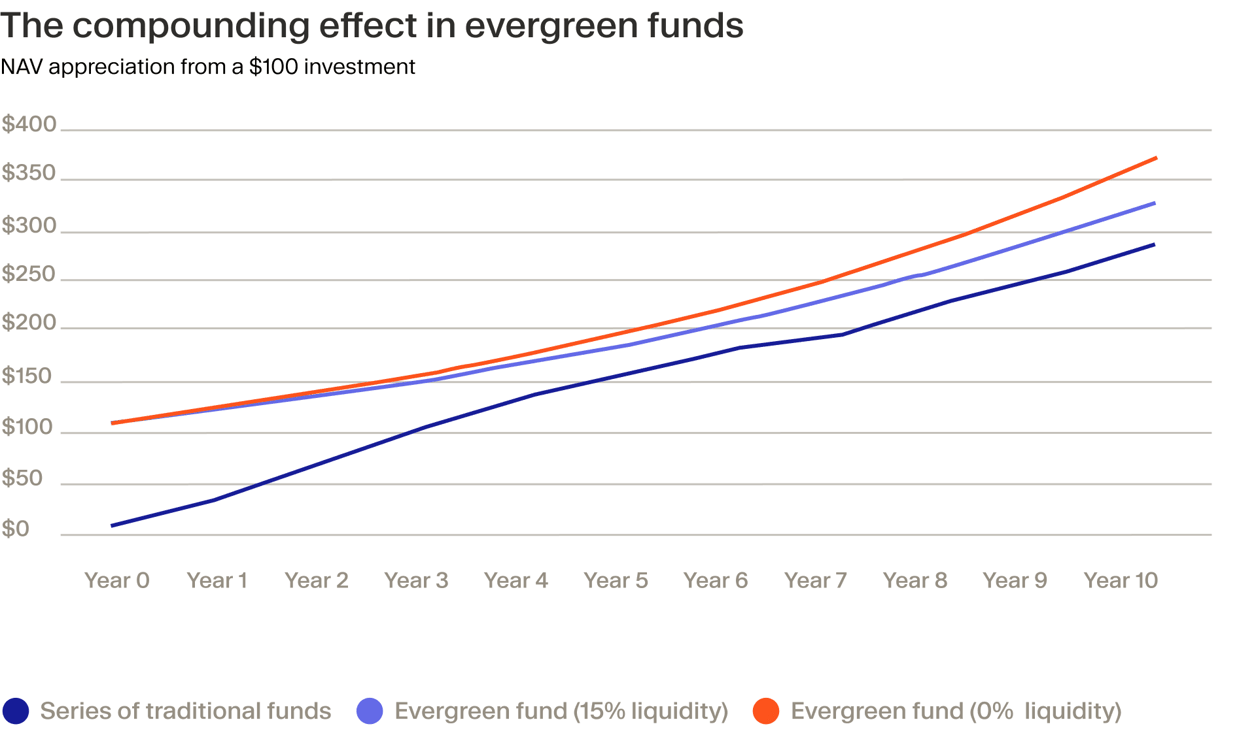

Reinvestment policy deserves particular attention here. Most evergreen structures recycle capital automatically, using distributions to fund new investments rather than returning cash to investors. This approach is intended to sustain compounding and keep capital at work, but also means investors should understand precisely how and when cash can actually be extracted.

Reinvestment supports long-term wealth accumulation, yet those needing periodic cash flow must understand that withdrawals require active redemption requests.

With realisations feeding the liquidity sleeve and the sleeve meeting ordinary withdrawals, the fund can theoretically operate smoothly. But what happens when withdrawal requests exceed the ordinary?

Redemptions are structured — and gated

Liquidity in evergreen funds is periodic rather than on-demand. Funds typically offer redemption windows quarterly, subject to advance notice periods ranging from 30-90 days.² This is essential to proper risk management.

Most vehicles impose redemption caps, limiting withdrawals to a percentage of NAV per quarter, commonly up to 5%.³ If requests exceed this limit, investors receive prorated settlements with excess amounts rolling forward to subsequent periods. Gates protect remaining investors from forced asset sales at distressed prices, preserving portfolio integrity precisely when markets become challenging.

The suspension right represents a more extreme safeguard. Fund documents typically allow managers to halt redemptions temporarily under exceptional circumstances such as market dislocation, portfolio company distress or liquidity crises.⁴

Such provisions protect long-term investors from being disadvantaged by a mass exodus, but they materially alter liquidity assumptions during systemic stress. Investors should understand that these rights exist as a practical circuit breaker that may activate when liquidity is most needed. They align incentives by preventing the destructive dynamic where early redeemers receive favourable NAV pricing while remaining investors inherit a portfolio of forced sales.

Subscriptions, redemptions and the NAV at which both occur depends on one important assumption: that the fund’s share price genuinely reflects what the portfolio is worth.

Valuation discipline is critical

Because subscriptions and redemptions occur at NAV, valuation methodology is critical when investing in evergreen funds. Investors entering or exiting must transact at prices reflecting genuine portfolio value, neither inflated to benefit outgoing investors nor depressed to advantage incoming investors.

Independent valuation processes, third-party reviews and conservative marking policies reduce the risk of entry versus exit arbitrage. Without rigorous standards, sophisticated investors might exploit stale pricing, redeeming when marks lag true deterioration or subscribing when undervaluation exists.

Governance structures typically include valuation committees independent of the investment team, reviewing methodologies quarterly. Hard assets and public market comparables provide benchmarks, but private company valuations inevitably involve some degree of subjective judgement.

What matters is consistency: applying the same conservative standards across market cycles prevents the NAV from becoming a trading opportunity rather than a true economic reflection of the portfolio.

Final thoughts

Evergreen funds provide an alternative route into private equity, one that trades the fixed ten-year horizon for continuous access. That flexibility comes with specific structural features including liquidity sleeves, NAV-based dealing and structured redemption rights. These are not flaws but intentional safeguards that prevent forced asset sales and serve to preserve value.

Understanding this trade-off is essential. Evergreen funds are best suited to investors who are willing to accept capped, quarterly liquidity for the potential to achieve compounded outperformance over the long term.