Three names define the 2026 IPO calendar. SpaceX, OpenAI and Anthropic could create more value at listing than every venture-backed IPO combined since 2000.¹ Dozens of private capital firms hold stakes across the three and stand to realise meaningful returns.²

Listings at this scale do more than return capital to their own investors. They reset risk appetite and could pull the next wave of mid-cap PE-backed deals forward. This is necessary given the scale of inventory across private markets: roughly 16,000 buyout-backed companies have now been held for four years or more, according to McKinsey,³ and it would take years to work through at the current exit pace.

Clearing it requires sales channels deep enough to absorb scale. Trade sales and secondaries have done much of the recent work, but neither can fully substitute for the public listings. The overhang only eases when IPO activity broadens across sectors, not when it concentrates in a handful of marquee names.

The early signs of a broader rebound are encouraging. Whether this momentum inspires dealmakers to pursue transactions in earnest, helping to lift distributions back toward historical levels depends on a number of conditions — and three in particular.

Aftermarket performance

Aftermarket performance translates directly to LP economics because sponsors rarely sell their full position at listing. Lock-up agreements typically restrict sales for 90 to 180 days, with sponsors selling down the remaining stake gradually over the following 18 to 36 months. The trading price during that disposal window determines what flows back to LPs.

The recent evidence on aftermarket performance is generally supportive but mixed. Moonfare’s analysis of data from Renaissance Capital, an IPO specialist,⁴ shows that PE-backed companies which went public this year trade 21% above their IPO price at the beginning of June, while those with VC sponsors are up 27% on average. This compares to 10% return for S&P 500 in the first five months of 2026.⁵

The window looks open, but it is rewarding selectively. A few recent listings illustrate what that looks like in practice. Blackstone-backed Legence went public in a major Nasdaq listing last September, debuting at a valuation over $3.2 billion;⁶ the engineering and maintenance services provider currently trades around 200% above its IPO price.

CoreWeave has had a volatile post-listing trajectory since its March 2025 debut but has lately turned upward; the AI cloud-computing company, backed by Magnetar and other investors,⁷ now trades at more than 190% premium to its IPO price.

Hinge Health, a VC-backed digital musculoskeletal care provider with Tiger Global and Coatue among its largest holders, is up 90% as of the end of May, roughly 12 months after listing.⁸

Not every recent debut has followed that arc. Cerebras Systems, a chip maker, has experienced a post-IPO pullback, with shares down roughly 25% from their opening-day close on May 14 as initial excitement has cooled and investors weigh the risks of a newly public tech stock. Still, the stock remains above its IPO price.⁹

There are clearer laggards too. Klarna's long-awaited September listing has so far been largely a dud, with its stock down around 60% from the IPO price.¹⁰ NielsenIQ, McGraw Hill and Medline have similarly failed to take off and currently trade below the price at which they were brought to public markets.

Depth beyond the top names

A market that clears SpaceX or Anthropic but not much more will struggle to move the distributions needle. The portfolio companies awaiting exit are mostly mid-cap businesses with much less household recognition, and it is their ability to access public markets that will determine whether distributions normalise.

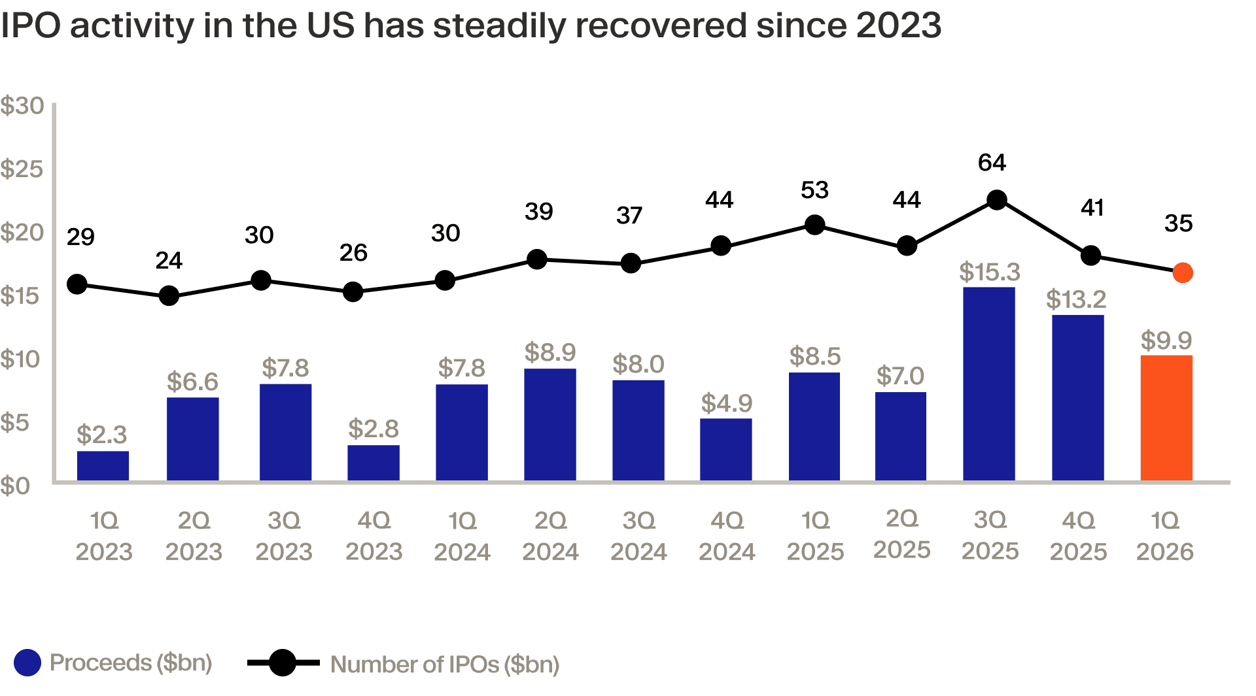

The US market is showing early signs that this depth is forming. The first five months represented the strongest start in PE and VC-backed IPOs since 2021, with a combined $25 billion raised through 36 US public listings, up from 19 in the same period last year, according to Renaissance Capital.

The pipeline is deeper still. There have been 112 new IPO filings year-to-date, a 12% increase from the same date last year. A flurry of private equity-held companies have recently registered for public offerings, including Advent's gas engine maker Innio,¹¹ Blackstone-backed mobile app advertising platform Liftoff Mobile¹² and bike-sharing app Lime which is funded by Bain Capital and Andreessen Horowitz.¹³ A much larger number are expected to file in the coming months, media reports suggest.¹⁴

In Europe, the story is more nuanced but better than a year ago. EMEA IPO proceeds reached $7.4 billion across 34 listings in Q1 2026, a 30% increase on Q1 2025, according to PwC.¹⁵ The key moment for the market came in October last year, when Hellman & Friedman-backed Verisure raised €3.2 billion in a Stockholm IPO¹⁶ at a €13.7 billion valuation which remains Europe's largest PE-backed listing on record.¹⁷ Seven of the top 10 IPOs in Europe this year were backed by private equity, according to PwC, “highlighting the ambition of investors to realise value”.¹⁸

The pipeline includes Peter Thiel-backed Bitpanda targeting a €4–5 billion Frankfurt listing,¹⁹ and a cluster of EQT-, CVC- and Permira-backed candidates positioning for the window. However, the momentum has been partly tempered by Middle East tensions, with several processes shifting their target windows to the second half of the year or 2027.

The interest rate and credit backdrop

Then there is the macro question. Many of the 2021–2022 investments were underwritten on rate and debt-cost assumptions that proved optimistic. Public market exits for these assets require either operational outperformance large enough to support the existing capital structure, or a credit environment that lets the public market absorb it. This condition is largely outside any sponsor's control and remains the swing factor.

The mechanics are worth being specific about. A typical 2021 deal in the US was struck at 13 to 14 times EBITDA²⁰ with leverage in the 5 to 7 times range,²¹ against a financing backdrop where senior debt spreads averaged roughly 425 basis points over the benchmark rate.²²

By 2023, the same capital structure cost the company several hundred basis points more in interest expense, eroding some of the free cash flow sponsors needed to deleverage ahead of exit. For public market investors, the key question is whether the balance sheet inherited from the buyout still makes sense at current rates.

The Federal Reserve's path through the second half of 2026 is therefore a key external variable for the exit pipeline. A measured easing cycle would compress spreads and bring more 2021-vintage assets into "IPO-able" range. A higher-for-longer outcome could extend the standoff through 2027.

Will mid-market follow?

Each successful listing makes it easier for the next sponsor to file, with confidential filings from PE-backed companies having picked up substantially in 2026. GPs who waited out the drought are now positioning for the window while it is open.

Whether the cycle compounds from here will depend less on the major names everyone is watching, and more on the hundreds of less famous portfolio companies that follow them.

¹ Stanford, K (2026) PitchBook

² Thomas, D, Vidal, K A, & Jazul, N I (2026) S&P Global Market Intelligence

³ McKinsey & Company (2026)

⁴ Renaissance Capital IPO Pro (2026) — paywalled, subscription required

⁵ S&P Dow Jones Indices (2026)

⁶ Reuters (2025)

⁷ CNBC (2025)

⁸ Yahoo Finance (2025)

⁹ Seeking Alpha (2026)

¹⁰ Yahoo Finance (2026) — Klarna stock quote

¹¹ Manufacturing Dive (2026)

¹² Reuters (2026)

¹³ Yahoo Finance (2026)

¹⁴ The Wall Street Journal (2026) — paywalled, subscription required

¹⁵ PwC (2026)

¹⁶ SWI swissinfo.ch (2025)

¹⁷ GAIN.PRO (2026)

¹⁸ PwC (2025)

¹⁹ Yahoo Finance (2026)

²⁰ PitchBook (2026)

²¹ PitchBook (2022)

²² PitchBook (2024)