Key takeaways

- Co-investments and direct investments have become a key component in building diversified private markets portfolios for investors of all types, typically alongside traditional fund investments.

- They provide targeted exposure, at lower cost, and with greater transparency and control than fund investments.

- Success depends on access to high quality deal flow, strong GP relationships, rigorous selection and being able to evaluate deals quickly.

When Silverlake made its $12.5 billion acquisition of software business Qualtrics in 2023, participants in the deal also included a range of LP co-investors.¹

Similarly, when Montagu and Astorg provided follow-on capital to drug delivery company Nemera in 2025, the firms invited LGT Capital Partners to join them in the deal.²

These are just two examples of a growing phenomenon: general partners (GPs) offering investors the opportunity to take stakes directly in companies alongside them.

Once open only to a select few private equity LPs, co-investments have become a core part of allocations for a wide range of investors. Well over half of larger investors rank co-investments as among their preferred investment routes, while nearly half of smaller investors say the same, according to a recent Aviva Investors private markets survey.³

And it’s not just institutional investors, such as pension funds and insurance companies, turning to co-investment and direct investing:⁴ around half of family offices’ private equity allocations target direct company exposures, according to a recent UBS report.⁵

Why co-investments?

Investors are taking an increasingly active approach to building and managing their private markets exposure. As a result, they are complementing traditional closed-end primary fund investments with a range of options, including secondaries and evergreen funds.

Rising interest in co-investments and direct investments is part of this trend, with investors drawn by a range of benefits, including:

Individual company selection. The Nemera deal highlights one of co-investment’s main attractions — knowing what you are investing in. Indeed, when announcing the deal, LGT Capital Partners said it had been following the company for several years. Unlike a traditional closed-end primary fund investment, where investors commit capital without knowing which businesses or assets will be in the portfolio, co-investors can be more intentional by selecting individual investments and — in some cases — negotiating terms and tailoring structures to meet their objectives.

More control over exposures. By selecting individual deals, investors can build more granularity in their portfolios, allowing them to fine-tune exposure to specific sectors or geographies if desired. They can double down on high conviction investments or diversify into new areas, a valuable feature during more volatile times. A recent Adams Street survey of institutional investors shows that co-investments rank at the top for attractiveness in 2026, above private equity secondaries, venture capital and private debt.⁶

Lower fees. Typically offered on a low or no-fee and carried interest basis, co-investments can help investors boost net returns in the portfolio. There’s no definitive data on co-investment performance, but the experience of major US public pension fund CalSTRS is instructive: research has found that its private equity co-investments have outperformed its fund investments over one, three, five, and 10-year horizons. Lower fees are part of the reason for this.⁷

Potential to add value. For some larger investors or those with specific domain expertise, co-investments can provide opportunities to influence the company’s strategy and decision-making. When EQT sealed a $14.5 billion deal to buy international schools operator Nord Anglia Education in 2024, Neuberger Berman was among several co-investors and was announced as a “strategic partner”.⁸

Potential for improved liquidity in an exit-constrained environment. Since investors provide capital for direct deals up-front and are typically invited to provide follow-on financing, co-investments often have a shorter J-curve than a primary fund.⁹ The Nemera and Nord Anglia deals illustrate this, since in both instances, the lead GPs had already been invested in the companies for several years.

Stronger GP relationships. Seeing first-hand how a GP operates and interacts with investee companies and management teams provides investors with intelligence that can feed into decisions about which funds to back in future fundraisings.

Accessing co-investments

Some LPs have the capacity to invest directly alongside GPs. However, this requires strong existing relationships with a range of GPs to ensure access to sufficient — and sufficiently high quality — deal flow to select from. It also takes resources to assess each opportunity and respond within relatively short deal timeframes.

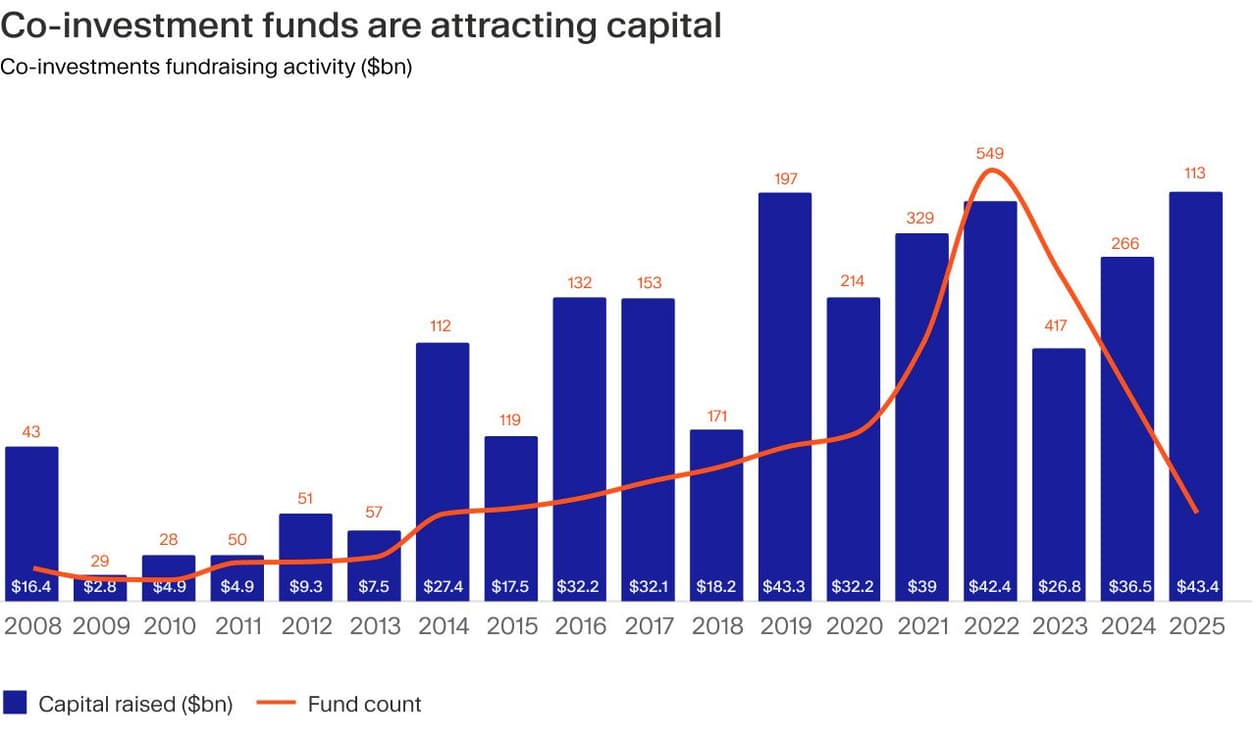

This is why we’ve seen such rapid growth in dedicated co-investment funds: in 2025, co-investment funds raised a record $43.4 billion, while AUM for these vehicles has more than doubled since 2019 to reach nearly $400 billion, according to PitchBook figures.¹⁰ By providing investors with more straightforward and diversified exposures, they are helping to broaden access and increase appetite for co-investments.

Co-investments and direct deals in investor portfolios

With 83% of respondents in the Adams Street survey planning to allocate to co-investments in the next five years, the market looks set for further growth. And the main reasons, according to a Coller Capital survey, are lower fees (with 78%) and access to specific investment opportunities (71%).¹¹

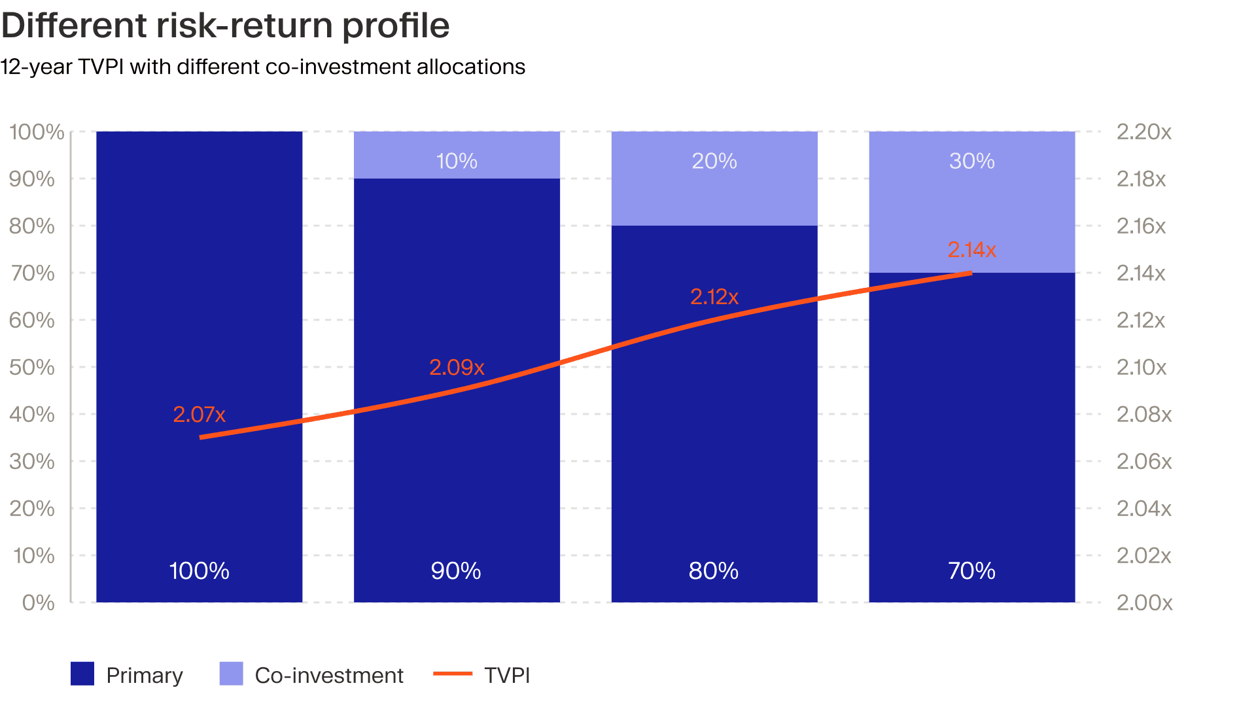

It’s therefore clear that investors are now using co-investments and direct investments as a core building block, alongside funds, when constructing diversified private markets exposure. Indeed, with a risk and return that differs from primary fund investing, co-investments can be a good addition to a private markets portfolio, as the illustrative example below shows.¹²

Yet gaining these benefits requires access to high quality deals managed by the best GPs, followed by rigorous selection. While co-investments and direct deals can provide diversification for the overall portfolio, they are more concentrated investments on a standalone basis than fund exposures. Co-investment returns can therefore meaningfully contribute to the performance of an overall private markets portfolio – in both directions. Having access to the skills and resources to choose the right deals really matters.

Therefore, for many investors, co-investment funds, including the pre-screened direct deals they can offer, are likely to be the most streamlined way of achieving diversified exposure to this rapidly growing part of the private markets investment universe.

Co-investments versus direct deals

At Moonfare, co-investments and direct deals are both types of transaction in which investors commit capital alongside a lead GP to gain direct exposure to a portfolio company. The main distinctions are that:

Co-investments are made via a dedicated fund, offering investors a straightforward route to building a diversified portfolio of co-investments without the need to assess, structure and manage each deal.

Direct investments are screened, hand-picked deals in companies that we offer to investors outside a fund structure alongside a lead GP we trust and know well. They give investors some control over the process and investment structure as well as the ability to fine-tune exposures according to their objectives.

EQT’s 2025 investment in Nord Anglia Education is an example of this: alongside Neuberger Berman, several institutional co-investors participated, including Moonfare, which also offered its investors direct access to the deal.