Key takeaways:

- Top-quartile VC funds tend to stay top-quartile. They outperform across successive vintages — largely a function of preferential access to deal flow.

- AI may be making this gap even wider. The space demands huge amounts of capital, with winner-takes-most outcomes.

- As more of the best AI deals flow to a small group of top firms, access to proven managers could become the deciding factor in who actually gets exposure to AI’s upside.

In venture capital, the success of a manager's earlier funds is a strong indicator of future performance. This phenomenon, known simply as performance persistence, has proven remarkably durable in VC compared with other asset classes, where it has generally weakened or disappeared as markets matured.

This distinction matters because artificial intelligence is impacting investment trends in ways that may further entrench these dynamics.

As AI attracts more and more capital, and produces winner-takes-most outcomes, the forces that drive VC persistence are growing stronger rather than fading. Early access to exceptional founders, preferential deal allocation and the ability to protect ownership through large follow-on rounds are becoming more decisive in an AI-driven market.

For limited partners, the task is to identify where persistence genuinely endures and assess how AI is changing the equations.

Running the numbers

The question of whether past performance predicts future results has haunted investment committees for decades. In venture capital, the answer appears to be yes, though with important nuances that have evolved as the industry has matured.

A comprehensive 2023 study¹ analysed over 2,000 funds spanning three decades using research-quality cash-flow data from Burgiss. The methodology addressed several limitations of earlier research. It examined fund sequences within specific strategies and distinguished between final performance data and interim information available to LPs at the time of fundraising decisions.

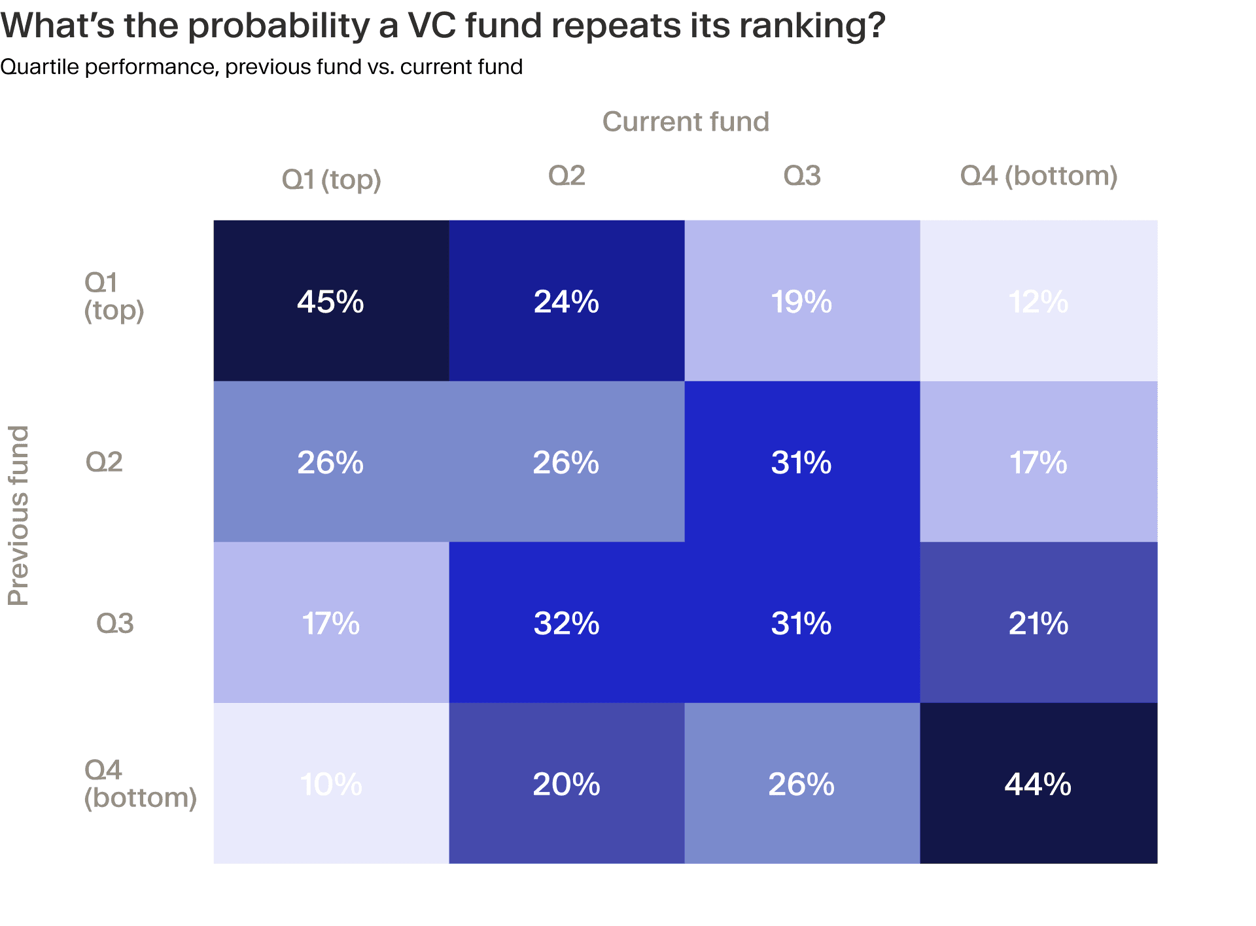

The results confirm that VC demonstrates marked persistence. Funds with a previous fund in the top quartile were in the top quartile 45.1% of the time and above median 68.7% of the time, far exceeding the 25% and 50% rates one would expect from random distribution.

Bottom-to-top quartile transitions occurred less than 13% of the time. This pattern held across both pre-2001 and post-2000 sub-periods, though with some compression in return differences over time.

The matrix table below shows this probability of a VC fund repeating its ranking.

GPs typically raise their next fund while the current one is still active, therefore LPs must decide without the benefit of final performance figures. Critically, persistence remained significant even when using only interim performance data available at the time of fundraising.

Top-quartile funds based on interim data produced an average Public Market Equivalent of 1.81 in their next fund, compared to 1.01 for bottom-quartile funds.

The fact that the pattern holds even with incomplete early data means the signal is detectable when it actually matters for investment decisions. LPs can identify likely outperformers in real time.

Preferential access is key

A separate study looking at individual deals found something similar. For every extra IPO a VC firm achieved in its first ten investments, its chances of producing another IPO later increased by up to 8%. In short, early wins tend to lead to more wins.²

The authors noted that persistence appears to operate primarily through access rather than selection skill.

Successful VC firms do not persist in their ability to pick the right industries or timing. Rather, early success leads to preferential access to later rounds and larger syndicates. This pattern seems most consistent with the idea that initial success improves access to deal flow, which raises the quality of subsequent investments and perpetuates performance.

Why manager selection is everything

The persistence phenomenon would be merely interesting if VC returns were normally distributed. That is far from the case. Return dispersion in venture capital is much wider than in public markets or buyouts, creating substantial economic consequences for LP allocation decisions.

A McKinsey analysis for 2011–20 vintage funds shows an interquartile spread of 16 percentage points of net IRR. This is wider than for buyout strategies (13.6 percentage points), where performance is more tightly clustered around the median IRR.³

Research from Commonfund underscores this point. Top-quartile venture capital managers generated returns over public markets in all but one vintage year from 2000 to 2020, with an average net annualised outperformance of 6.1%.⁴ Median managers, by contrast, failed to beat public markets in 11 of 21 years.

In venture capital, manager selection is everything.

The great AI pivot

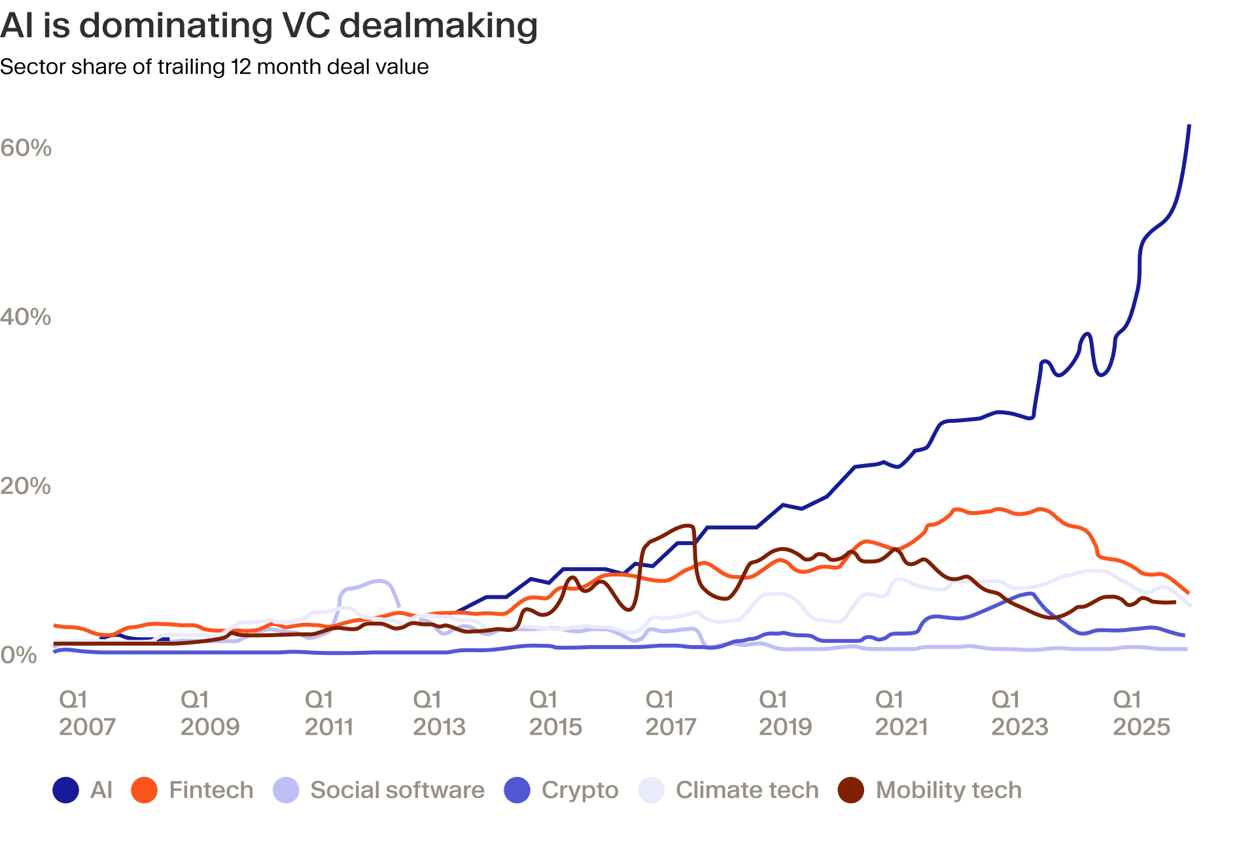

If persistence describes the steady-state of venture capital, AI represents a structural break that is amplifying these dynamics. AI investing now dominates venture capital to an unprecedented degree.

PitchBook data shows that AI startups in the US captured 63% of total VC deal value in Q3 2025, compared with 40.3% a year prior and peaks of 17.1% for fintech and 15.1% for mobility in previous hype cycles.⁵

This capital is concentrating into fewer, larger deals. Among the top 10 VC-backed companies by valuation, three of the top five are AI companies – OpenAI, Anthropic, and xAI – with a combined valuation exceeding $1.1 trillion.⁶

The concentration extends beyond deal size to geography and firm market share. The US captured 79% of global AI funding in 2025, up from 57% in 2024.⁷ At the firm level, just 12 managers captured around half of all VC dollars in the first half of 2025.⁸ And the list goes on.

The AI effect

We believe that AI has the potential to strengthen rather than disrupt the mechanisms behind this persistence.

Several structural features of AI investing favour established franchises. Early access to breakout founders is paramount, and in oversubscribed seed or Series A rounds allocation is far from random. Anecdotal evidence suggests that founders, particularly those with technical pedigrees, choose investors based on brand, platform support and proven scaling expertise.

The serial entrepreneur effect compounds this dynamic. Research has shown that entrepreneurs with prior success have a 30% success rate in their next venture, compared with 21% for first-time entrepreneurs.⁹ As these successful founders gravitate toward top-tier VCs, it creates a self-reinforcing cycle of quality deal flow.

Experience and infrastructure create another edge. Managers who have invested through previous technological shifts bring institutional memory - they’ve seen platform transitions before and understand how to evaluate them.

Just as importantly, established VC franchises have built platforms that are hard for newer managers to replicate. Their edge goes beyond capital. It includes deep ties with hyperscalers, strong syndicates to support growth and exits and access to specialist talent networks.

Capital concentration

Capital concentration in breakout rounds represents perhaps the most important mechanism at play. AI investing requires unprecedented capital deployment discipline. Follow-on rounds are massive, meaning ownership dilution can be devastating for early investors who cannot maintain their pro-rata.

Top-tier firms possess structural advantages here. They defend ownership more aggressively, often investing beyond their pro-rata to maintain their position. They have the capital base to support winners across multiple $1 billion-plus rounds. They win allocation in competitive later rounds by leveraging their networks.

The persistence mechanism therefore operates not only through initial selection, but through capital deployment across rounds.

Access is everything

Persistence data must be interpreted thoughtfully. It is not proof of pure skill – performance over cycles is partly driven by access and reputation feedback loops. It is also prone to survivorship bias because some underperformers disappear.

Despite these caveats, backing proven franchises during transformative cycles matters more than in stable periods. The dynamics of AI investing such as massive capital requirements and the critical importance of follow-on rights amplify the advantages of established managers rather than eroding them.

This carries major implications for investors. Access to a small group of top-tier VCs can define in what capacity LPs are able to participate in arguably the most transformative technology of our generation. The persistence of returns in venture capital has held through multiple technology cycles. AI appears poised to extend this enduring trend.