Our key takeaways:

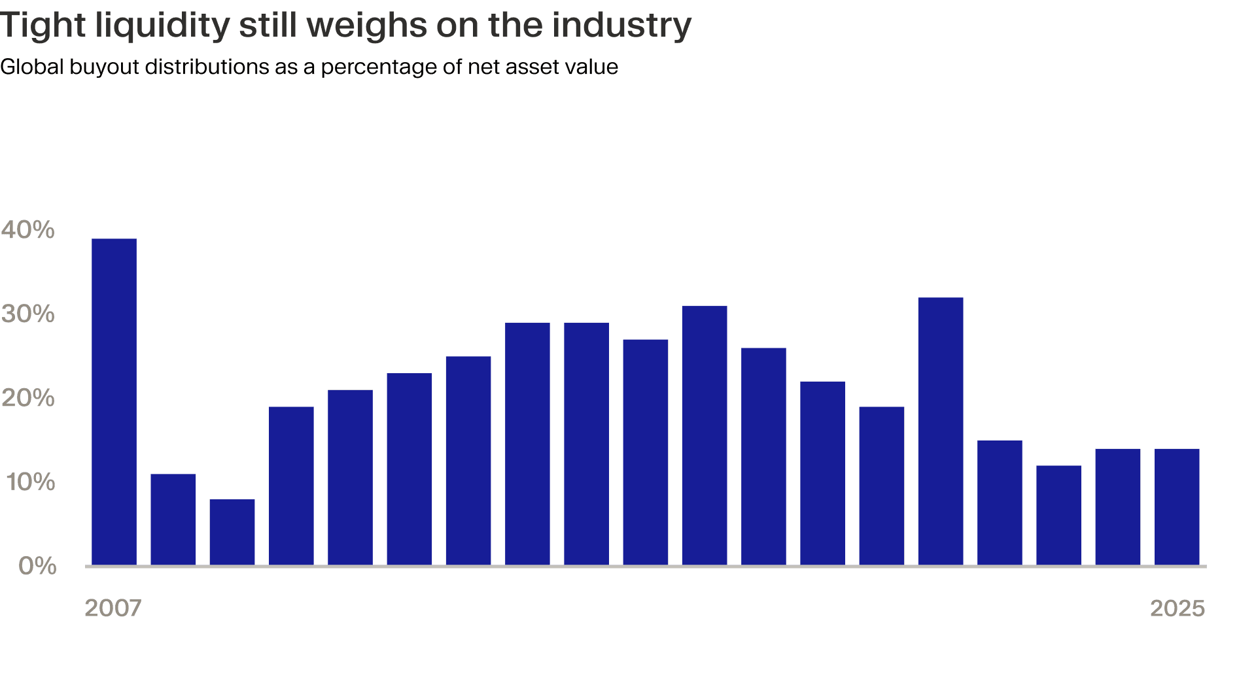

- With buyout distributions stuck at 14% of NAV, GPs that deliver cash returns back to LPs have a decisive fundraising edge.

- Most value creation (71%) now comes from revenue and EBITDA growth, not multiple expansion.

- The gap between top- and bottom-quartile buyout funds has stretched to nearly 14 percentage points, concentrating returns among fewer, more disciplined managers.

The private equity industry has spent the better part of four years waiting for conditions to normalise. Deal activity moderated. Exits were delayed. Distributions ran below historical averages.

And yet, through it all, capital continued to flow. No less than $1.8 trillion has been raised since 2022, according to Bain,¹ affirming that sophisticated investors have maintained conviction in the asset class through the cycle.

That patience may be rewarded. The exit environment is showing signs of improvement and deployment is rising. But the industry emerging from this period looks fundamentally different from the one that entered it. Financial engineering has given way to operational transformation. Broad-based strategies have ceded ground to focused expertise. And the gap between top-quartile performers and the rest has widened to levels not seen in a decade.

Bain & Company's 2026 Global Private Equity Report offers a clear-eyed assessment of this new reality. Here are five takeaways that we believe investors should pay the closest attention to.

1. Liquidity recovery is proving gradual

Net cash flow turned marginally positive in 2025, but when measured as distributions relative to NAV, the figure flatlined at 14% – a level last seen during the global financial crisis.

As we noted in our 2025 review, this dynamic is taking a toll on investor liquidity. With over $3 trillion of unrealised value sitting in global buyout portfolios, working through this backlog will take time. For GPs, the implications are clear: those delivering cash returns on schedule hold a distinct advantage in raising their next funds, while those falling behind face likely to struggle.

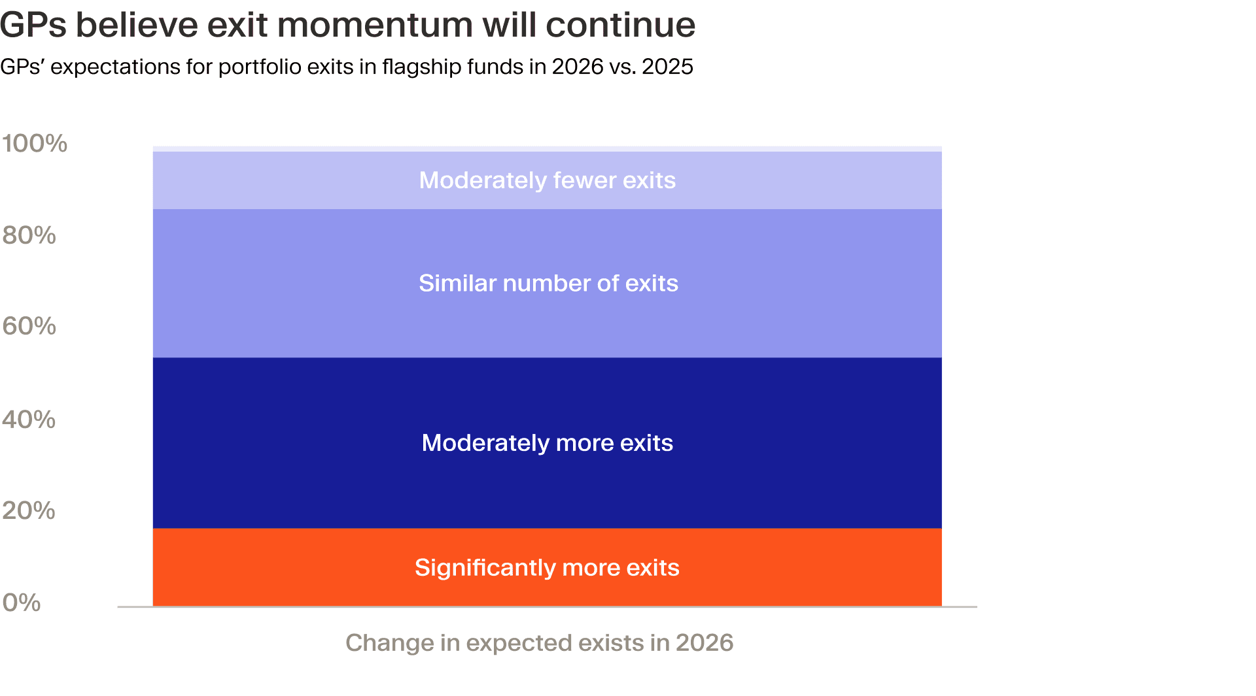

2. Exit activity is heating up

Encouragingly, early signs suggest that this liquidity pressure may begin to ease.

Interest rates are gradually declining, deal pipelines are well stocked and the record-breaking Medline IPO, the largest PE-backed listing to date, signals that public markets are reopening. Corporate M&A activity, which supported exit values throughout 2025, continues apace against a backdrop of elevated equity markets and economic resilience that has defied many expectations.

GPs are responding accordingly. According to the latest StepStone/Bain survey, confidence is building that exit momentum will strengthen this year, with 55% of respondents expecting more transactions while only 14% anticipate a decline.

PitchBook data highlighted in Moonfare’s own 2026 outlook supports this: by the end of Q3 2025, global exit value had already exceeded full-year totals from each of the previous three years. If current trends hold, the capital recycling mechanism that drives private equity may finally regain traction – though as Bain notes, sponsors still face considerable work in reducing hold periods and improving distribution profiles.

3. Elite managers maintain their edge

Despite fundraising headwinds, buyout funds have raised $1.8 trillion since 2022 – clear confirmation that institutional capital continues to flow toward the asset class.

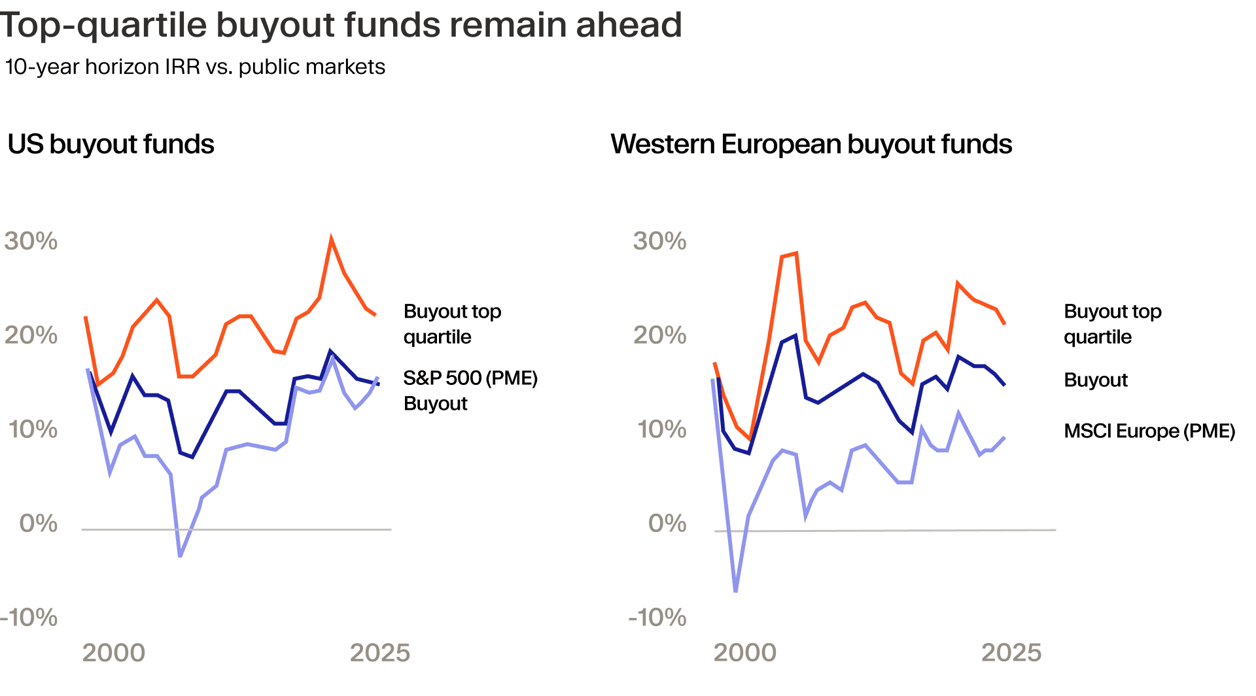

While public market returns have recently eliminated the historical performance premium over 10-year horizons, sophisticated investors recognise these gains as exceptional rather than structural. The majority of this outperformance came from a handful of Big Tech stocks, which have lagged the equal-weighted S&P 500 since November.²

More importantly, private equity investing is not buying an index and offers substantial outperformance through careful manager selection. The numbers are compelling, Bain’s analysis shows. Top-tier buyout funds consistently beat public markets across all measured time horizons.

Yet this outperformance is concentrating among fewer names. As we noted in our outlook, the return gap between top- and bottom-quartile managers has widened to nearly 14 percentage points for the 2021 vintage – the largest spread in a decade. In this environment, identifying the best managers is essential.

4. The era of financial engineering is over

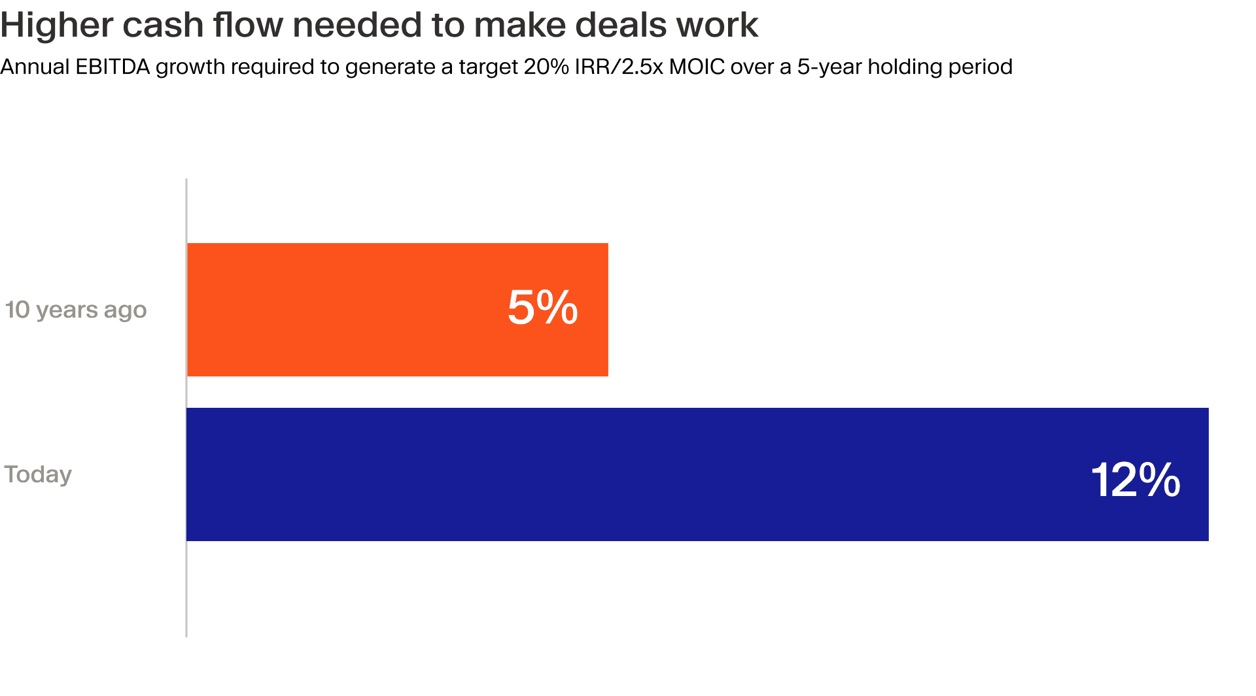

The arithmetic of buyouts has transformed beyond recognition. A decade ago, a typical transaction employed leverage of 50% at interest rates of 6-7%, with sponsors benefiting from steadily expanding valuation multiples. Under those forgiving conditions, modest annual earnings growth of 5% could generate attractive returns over a standard holding period.³

Today's environment is totally different. Financing costs have climbed to 8-9%, leverage has compressed to 30-40% and purchase multiples remain elevated without the support of further expansion.

According to Bain, deals that once required single-digit earnings growth now demand double-digit improvements to achieve equivalent returns, which is a fundamental reset in value creation requirements.

As we flagged in our 2026 outlook, operational improvement has displaced financial engineering as the primary driver of returns. Recent data shows revenue growth accounted for 71% of value created in 2024 exits, up from 64% in 2023 and far exceeding any previous five-year period.

The industry is returning to first principles: building stronger companies through hands-on operational involvement, but with deeper expertise and more sophisticated tools than in previous cycles.

5. In 2026, generalists will get squeezed

In a market saturated with capital, undifferentiated generalists are struggling to attract commitments. Generic claims of value creation are no longer enough to persuade investors.

Limited partners demand specificity: a coherent strategy articulated clearly, supported by evidence of portfolio company transformation, consistent returns and reliable cash distributions.

“As the industry matures and becomes increasingly more competitive, LPs are ever more focused on who within the asset class can deliver,” argues Bain.

Winning firms rigorously evaluate their own track records to identify genuine competitive advantages, sharpening focus around what they do distinctively well. They start building relationships with targets years before a sale is even rumoured, developing insights no one else has. When the auction finally comes around, they can move faster and bid with more conviction because they already understand what the business could become.

The most sophisticated managers treat due diligence as an opportunity to map out exactly how they would transform the asset. They identify the specific operational improvements, revenue initiatives and technology upgrades that will drive meaningful, lasting earnings growth.

This lets them underwrite a genuine upside case rather than a conservative base case, giving them the confidence to be aggressive on price while still protecting returns. And because they know exactly what levers to pull, they start creating value from the moment the deal closes.

Looking ahead

The industry is entering a new phase where discipline, operational excellence and careful manager selection matter more than at any point in the past decade. The recovery of 2025 benefited some participants far more than others and as the cycle progresses, we expect this divergence to intensify.

For investors, the priority is clear: Back managers possessing coherent, repeatable strategies and the demonstrated capability to drive value creation in what is an increasingly demanding environment.