The private equity market is consolidating around fewer managers, with investors demanding cash returns over paper marks and extending existing relationships rather than initiating new ones.

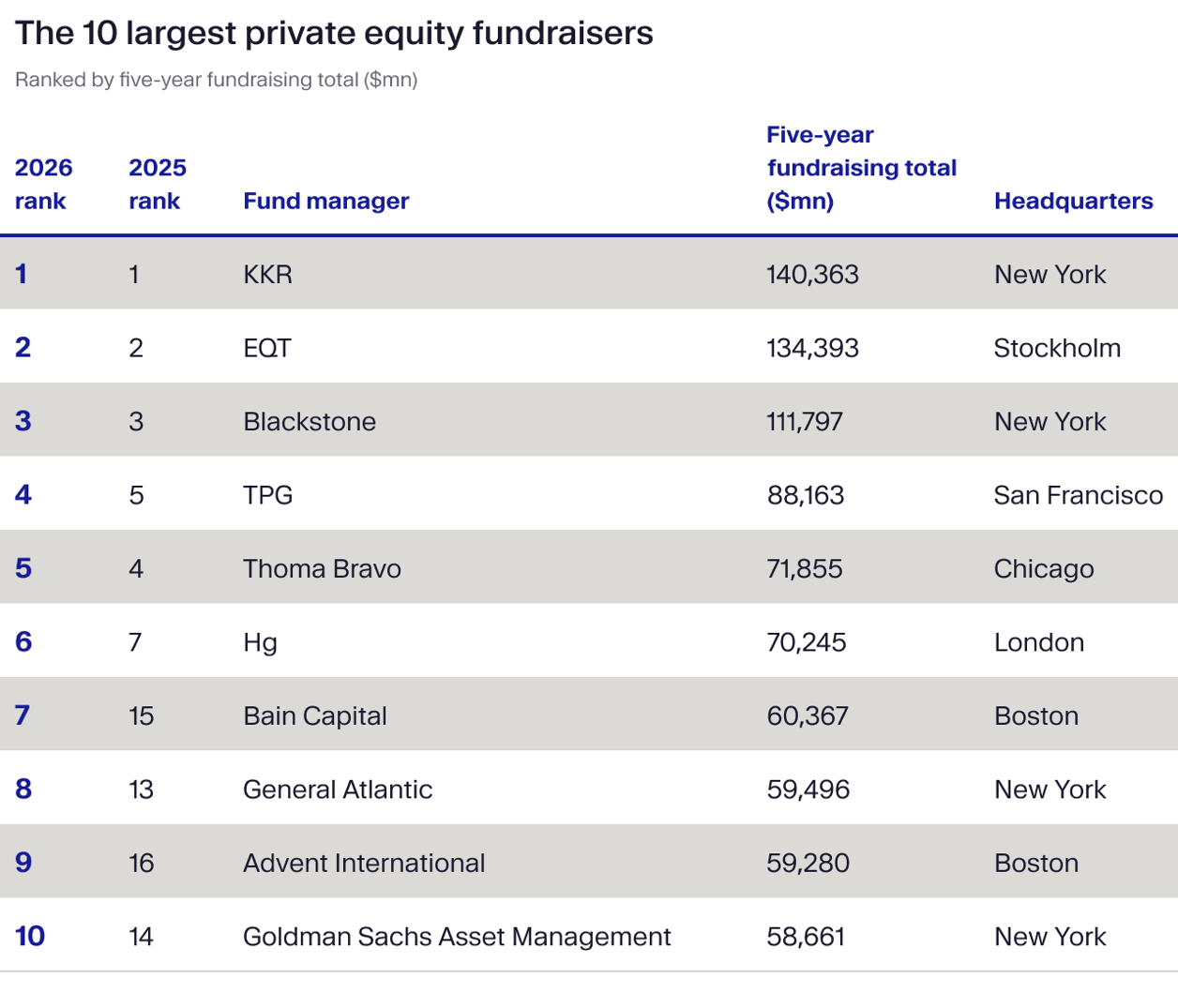

Private Equity International's latest ranking captures the scale of that divide. The top 300 fundraisers, representing around 2-3% of the global PE market by count, amassed a record $3.6 trillion over the past five years, as of end-2025, up 8% from the year earlier.¹ The minimum amount to enter the list was $2.8 billion — also an all-time high — while the top ten firms alone, including KKR, EQT and Hg, raised $855 billion, roughly a quarter of the entire tally.

This sits against a backdrop of global PE fundraising at its lowest since 2020 as only $735 billion was raised in a single-year 2025, a 20% drop from the prior five-year average.² Capital has clearly moved to fewer hands, and the gap between the top of the market and the rest has widened significantly.

The issue is cash flow, not conviction

These figures underscore that the key issue for LPs is not conviction (surveys show that most investors plan to maintain or increase their allocations³ ⁴ ⁵) but rather cash flow. A significant share of commitments from 2021 and 2022 vintages have not yet been called, and not enough has come back. Distributions as a percentage of net asset value (NAV) have held below 15% for four years running which is an industry record, per Bain’s annual report.⁶

The result is a market where willingness to allocate and ability to allocate have come apart. By end-2025, more than half of LPs surveyed by PEI reported that undrawn prior commitments were directly limiting their ability to make new ones — up 15 percentage points over twelve months. Moonfare's own investor survey (ongoing as of mid-June) reinforces this: when asked what would need to change to increase their private markets allocations, improved distributions ranks as the top answer — ahead of valuations, fees or market timing.

Until capital is recycled, many investors are not taking chances on new relationships. Around 70% of LP commitments in 2024 and 2025 went to existing GP relationships, up from 60% five years earlier, per Preqin data, analysed by Pipelineroad.⁸ This means that of every $100 of institutional PE capital committed, around $10 to $15 is realistically available for a manager without an established LP base.

What winning GPs look like

That scarcity has also clarified what LPs require from the managers they do back. The clearest change in selection criteria is the move from IRR to DPI. IRR measures annualised return while DPI measures how much cash has come back to investors. According to McKinsey's 2026 Global Private Markets Survey, DPI has become as important a performance metric as MOIC⁹ - a big jump on the priority list compared to just a few years ago.

In a period of slower exits and extended holding periods, IRR and realised returns have diverged, sometimes sharply. A GP who can consistently return capital on schedule demonstrates something IRR alone cannot: that the value creation model works end to end, from entry through exit. Managers who can't show progress toward at least 1.5x paid-in capital by year eight face a difficult fundraising conversation regardless of the unrealized value generated.

Consistency across cycles matters as much as average returns. The performance spread between top and bottom-performing buyout managers for the 2022 vintage reached more than 13 percentage points and is the widest since 2014.¹⁰ Top-quartile managers delivered around 22% IRR over the past decade against a median of around 13%¹¹ — a gap of roughly 8 to 9 percentage points that, over a fund life, compounds into a materially different outcome for investors. LPs are not looking for the manager who had one strong vintage; rather, they are backing managers who held up when conditions turned for the worse.

Organisational stability has also become an explicit criterion. LP commitments run for ten to twelve years. What an LP is underwriting is not just a fund but whether the organisation generating those returns will still be coherent at redemption with the same team and similar strategy. A February 2026 analysis published by Harvard Law found that 96% of LPs now cite succession readiness as decisive in re-up decisions.¹² In practice that means formal transition plans, distributed carry across the investment team rather than concentrated at the founding partner level and key person provisions broad enough to cover the people running deals.

Finally, co-investment access is now a baseline LP requirement, not a differentiator. Co-investments let LPs increase exposure to their highest-conviction assets at lower cost. A GP that doesn't offer them is asking LPs to accept less flexibility and less alignment than they can get elsewhere.

Private wealth is changing the demand structure

The institutional liquidity squeeze doesn't capture the growing role of private wealth. More than 80% view private market risk as equal to or below public market levels, per Hamilton Lane's 2026 Global Private Wealth Survey.¹³ Their capital depends somewhat less on the distribution cycle currently limiting what pensions and endowments can deploy.

The volumes are already significant. Blackstone attracted more than $11 billion from private wealth investors in Q4 2025 alone, up 50% year-on-year.¹⁴ KKR's latest flagship included meaningful commitments from family offices and private wealth platforms.¹⁵ Evergreen structures — one of the primary vehicles through which individual investors access institutional-quality managers — now account for around 5% of private markets NAV and are expected to grow steadily, per Hamilton Lane.¹⁶ For many private wealth investors, evergreens represent the first viable route into managers that were previously accessible only to large institutions.

Pole position for established firms

As the distribution recovery anticipated through 2026 and 2027 begins releasing capital currently trapped in LP portfolios, allocation decisions should accelerate. The managers best positioned to capture them are those who have spent the past three years generating consistent returns, have demonstrated cash distributions and are running an organisation that LPs know and trust.

For everyone else, the window doesn't widen just because more capital becomes available; the re-up dynamic means established relationships absorb the recovery first.

¹ Private Equity International, 2026 (behind paywall)

² Private Equity International, Savcenkova, Mendoza, 2026

³ WealthBriefing, 2026

⁴ Hamilton Lane, 2026

⁵ McKinsey & Company, Edlich, Llewellyn, Croke, Schneider, Teichner, 2026

⁶ Bain & Company, 2026

⁷ Private Equity International, Mendoza, 2026

⁸ Pipelineroad, 2026

⁹ McKinsey & Company, Edlich, Llewellyn, Croke, Schneider, Teichner, 2026

¹⁰ J.P. Morgan Asset Management, 2026

¹¹ Bain & Company, 2026

¹² Harvard Law School Forum on Corporate Governance, Taylor, Hammond, Byrne, 2026

¹³ Hamilton Lane, 2026

¹⁴ Yahoo Finance, 2026

¹⁵ Business Wire, 2026

¹⁶ Hamilton Lane, 2025