Most investors in public markets will be aware of the efficient market hypothesis, the dictum that all publicly available information should be reflected in market prices. It seems that in a topsy turvy world, markets are less efficient, or perhaps giddier, especially so given the impact that artificial intelligence (AI) is having on stocks.

One example that comes to mind is the ‘DeepSeek’ sell-off in technology stocks that occurred in late January 2025.¹ The realisation by investors that a cheaper, open-source approach to large language model building is possible rattled investors in companies positioned as AI winners.

In late December 2024, I had seen test results, showing how DeepSeek AI could achieve similar results to more expensive platforms, potentially triggering a sell-off in AI-centric stocks modes — thanks to Azeem Azhar’s blog who had mentioned it as far back as December 2023. Readers may be interested in Azeem's and my podcast conversation on this topic and the broader AI landscape.

‘The 2028 Global Intelligence Crisis’

So, this is the context in which we viewed the recent research paper from Citrini Research entitled ‘The 2028 Global Intelligence Crisis’,² published on 22nd February, that triggered a sell-off in technology stocks, and in the stocks of companies that are vulnerable to disruption by AI.³

The Citrini paper is a well thought out scenario-driven note, that outlines how at a time point in the future, AI tools undercut the production of software, and in short time the white-collar workforce. This causes a corresponding drop in discretionary consumer spending, and thus devastating the economy.

The Citrini paper is a provocative read, but there are plenty of other equally alarming scenario driven notes on AI and the economy in circulation.

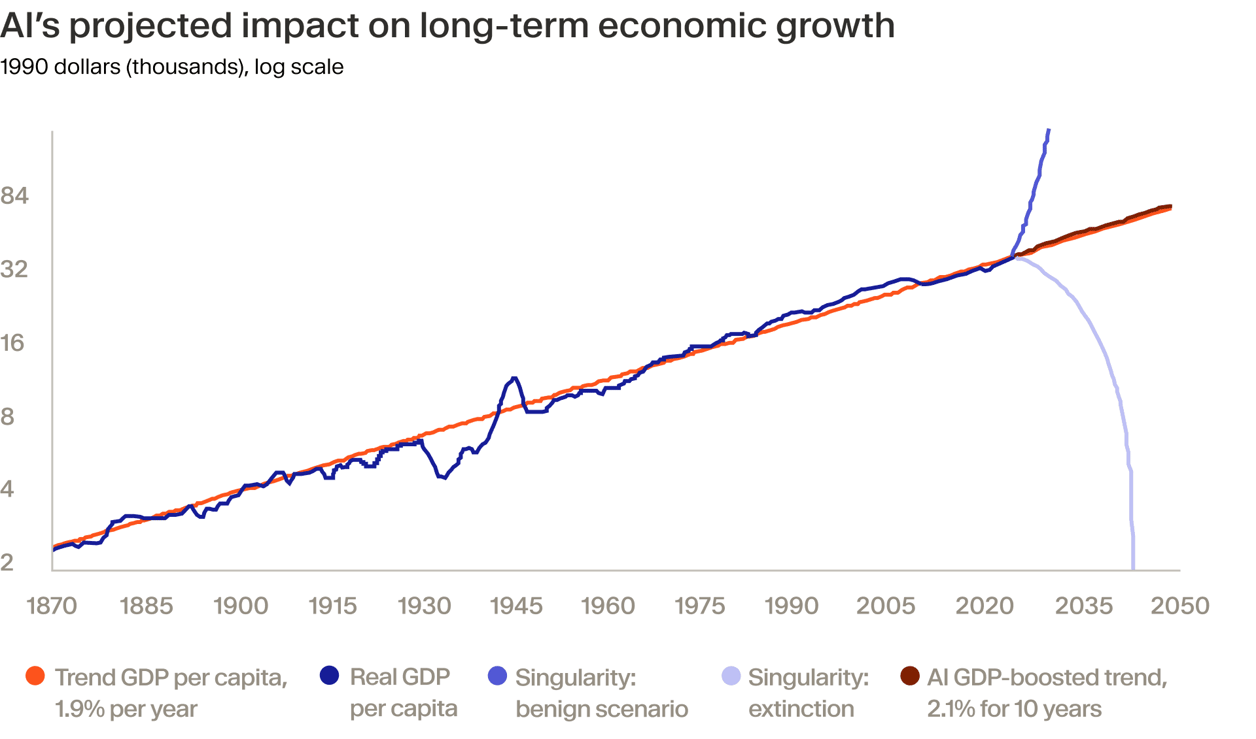

My favourite is from the Dallas Federal Reserve research team who have produced one of the most gripping charts I have seen.⁴ Like Citrini, it relates to the potential for AI to impact long-term economic growth.

Normally, economists deploy three types of forecasts: a mainline projection that tracks historic growth rates, an optimistic version that is just a bit higher and a corresponding pessimistic one. In this paper, however, the optimistic scenario is vertically upwards and the pessimistic one is vertically downwards, highlighting the potential of AI to revolutionise the economy or to destroy humanity.

Another example are the geopolitical thrillers authored by Admiral Jim Stavridis and Eliot Cohen, such as ‘2034’ that outline the great power military battles of the future.

However, neither the Stavridis books, nor the Dallas Federal Reserve research team have triggered market reactions. In this light, the response to the Citrini note has much more to do with jittery investors than the analytical power of the note.

Winner-and-loser effect

In our view, the reaction to the Citrini note signals that public markets have now moved beyond the first phase of the AI capex boom/bubble. This phase centred around the build-out of the large language platforms, of whom Anthropic and OpenAI are the dominant players, and who are busy assembling ecosystems around themselves.

This second phase of the AI boom is more focused on the ways in which AI will impact individual sectors like healthcare, the military and finance for example, and within these will create a pronounced ‘winner-and-loser’ effect.

Focus on productivity

There are several factors that bear a focus. The first is the speed of AI, not only in terms of the commercial take-up, but the ability of models to learn, think and act, sometimes in ways that are not bound by human morality. The apparent use of AI by the US military in Venezuela and Iran is a case where the technology needs to be tightly bound in its uses.

At the same time, we hear of multiple reports where AI has enhanced the early diagnosis of ailments (notably different forms of cancer), and the application of this to emerging economies could have a transformative impact on public health.

Another trend to focus on is productivity. A range of papers attribute a very wide bandwidth of productivity benefits to AI. To my reading, the most comprehensive one comes from the UK’s independent economic body, the Office for Budget Responsibility (OBR) who have stated that the productivity benefits from AI are yet uncertain but, depending on different scenarios, could range up to 1.5% in annual productivity growth over the next ten years.

It is worth noting that some of the most optimistic forecasts of AI driven productivity gains come from firms like McKinsey⁵ and Goldman Sachs, who make a large amount of their revenues from the AI industry, while some academic economists like Daron Acemoglu have taken a more conservative view. Still, none of these are as terrifying as the Citrini outlook.

Suggested read: Market commentary: AI as an asset class

Replaced by machines?

However, as the social and industrial effects of AI become more pronounced, there is growing evidence that AI can save people time by replacing tasks that were perhaps standard, repetitive or cumbersome, according to a paper from the St Louis Fed.⁶

What is not yet clear is how workers deploy the time they manage to save, and whether they learn less, which could mean they are eventually replaced by machines. Our sense is that through history, there are very few if any technologies that have wiped out jobs at a mass scale, rather they displace workers into new roles, notably so where education and training keep up pace with technology.

We believe that AI is simply entering a new phase, where take-up is accelerating, and where the disruptive effects are becoming more pronounced. Most businesses cannot afford not to use it.

As a final remark, if they are still fixated on the ways in which AI can collapse our civilisation, readers might want to amuse themselves with one of the first works of fiction to tackle the ability of machines to think and act independently, Robert Harris’ ‘The Fear Index’.